There’s a difficult fiscal negotiation underway between Canada’s various governments. And there may not be much room for maneuver.

“We’re very aware of the uncertainty in the global economy right now,” federal Finance Minister Chrystia Freeland said last week following a meeting with her provincial counterparts.

“At the federal level, this is a time of real fiscal constraint.”

She’s right. And that matters for all Canadians.

Provinces and territories want additional federal dollars for health care, and premiers are meeting with the prime minister today to demand exactly that.”

But as the finance minister correctly noted, there are limits to what the federal government can do, especially with rising interest rates and slowing economic growth.

To see this, imagine grouping federal program spending this year into just three buckets:

- Transfers to elderly individuals and families with children: $94 billion

- Major transfers to provinces and territories: $88 billion

- Everything else: $256 billion

It turns out, planned growth in federal spending is constrained to just the first and second buckets.

Elderly benefits are set to grow 7 percent per year between now and 2027. Child benefits grow by nearly 4 percent per year. And major transfers to provinces and territories grow at 5 percent.

And of the major transfers, funding for health systems is the largest: roughly $45 billion per year, which will increase to nearly $59 billion by 2027—that’s an average annual growth rate of over 5.3 percent.

Outside of these two buckets, total federal spending is currently slated to fall. And that’s in nominal terms. Adjusted for inflation and population growth, this bucket of federal spending will be nearly 17 percent lower in 2027 than it was in 2022. That’s significant.

Of course, that’s just the latest plan. And as others like Andrew Coyne regularly point out, the federal government consistently overshoots its own spending plans.

If this third bucket of federal spending instead grows at 2 percent per year, which will barely keep pace with future inflation, then total federal program spending would grow by an average of 3.5 percent per year over the next five years. And if the third bucket of spending grows at 3 percent, then total federal spending would grow at over 4 percent.

These growth rates are large—and potentially unsustainable.

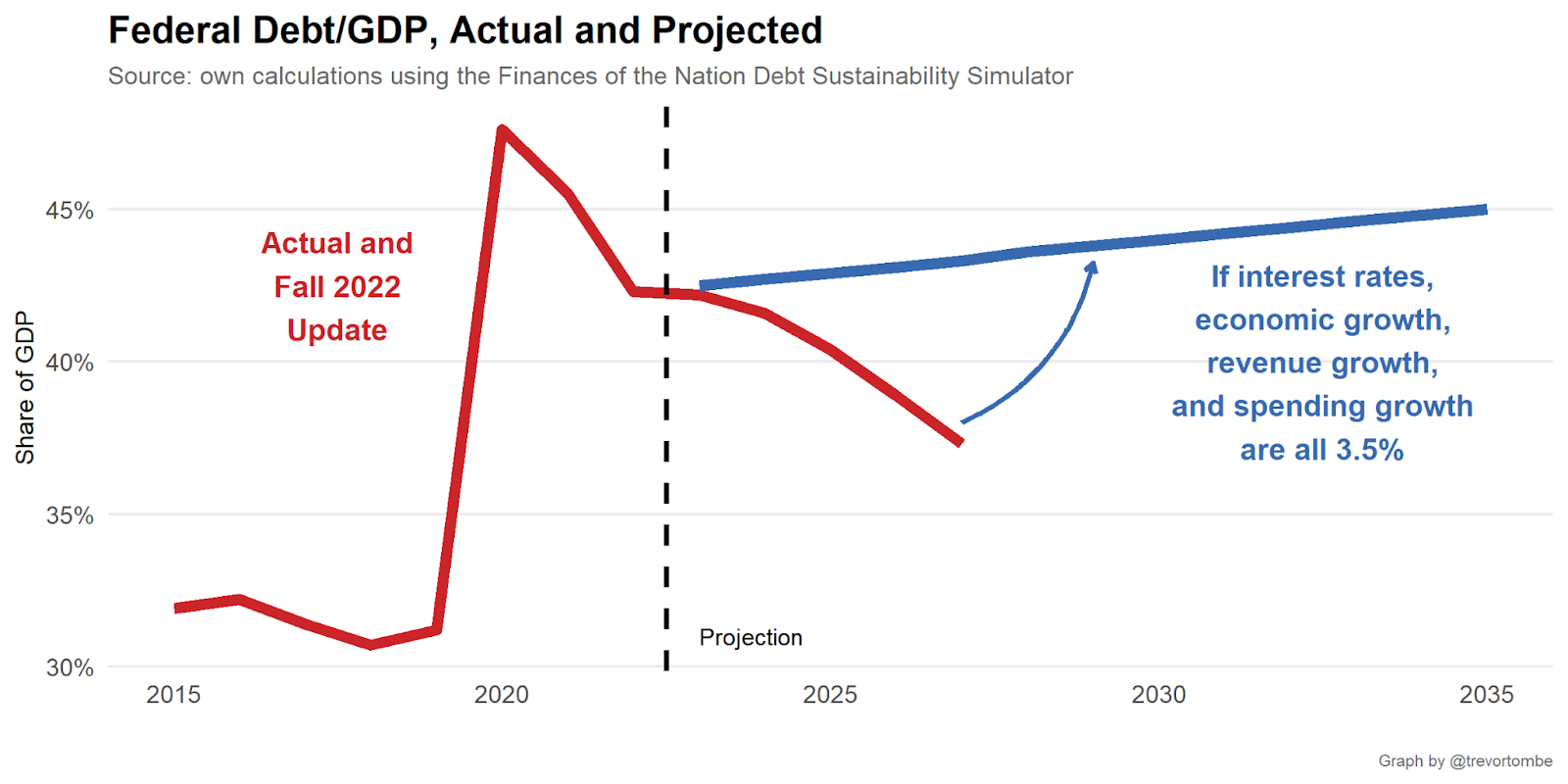

To illustrate, I estimate that if interest rates, program spending growth, total revenue growth, and Canada’s economy all grow at 3.5 percent per year,Economic growth here refers to nominal growth. This rate would be roughly 1.5 percent real GDP growth, which may be optimistic in the short term. then federal debt will increase to over 43 percent of GDP—higher than its current value of around 42 percent and much higher than the planned 37 percent.All calculations in this article are based on the Finances of the Nation Debt Sustainability Simulator. This was recently extended to allow alternative federal budget assumptions from 2022/23 onwards. Errors are my own.

Beyond 2027, federal finances become increasingly unsustainable at these rates as public debt continues to grow faster than the economy. I estimate a tax increase equivalent to increasing the GST from 5 percent to 6 percent would be required to stabilize things.

Canada’s finances are on a knife’s edge, leaving little room for provinces.

If health transfers grow just two percentage points faster than planned as a result of any deal—far less than provinces are asking for, but roughly aligned with what the Conservative Party proposed in the 2021 election—then total federal program spending growth increases by between 0.2 and 0.3 percentage points per year.

That may not sound like much, but it adds up quickly.

If interest rates, economic growth, revenue growth, and initial program spending growth are all 3.5 percent, then a boost in health transfers of this amount increases federal debt to 44 percent of GDP by 2027 and over 50 percent by the mid-2030s.

Add in a decline in global economic growth, and the consequent reduction in Canadian growth and federal revenues, and the picture becomes even more difficult.

At 3 percent growth, for example, federal debt would be 46 percent of GDP by 2027—higher than any point since 2020/21 when the pandemic disruptions and government support measures were at their highest.

To be sustainable without increasing taxes, spending must fall. But if we’re not going to touch benefits to the elderly or to families with children (which no party seems interested in doing), then increased transfers to provinces must significantly crowd out all other spending.

And to achieve the government’s debt reduction plan of 37 percent of GDP by 2027 then all other federal spending would need to fall by 25 percent (roughly 5 percent per year).

That’s a bleak scenario. But even if economic growth doesn’t slow so much, and if interest rates ease, federal spending constraints remain tight. With 3 percent borrowing rates and economic growth of 3.7 percent, for example, the third bucket of spending still needs to shrink by over 10 percent by 2027 to achieve the government’s debt target if health transfers are modestly increased.A freeze in all other spending would result in a 40 debt-to-GDP ratio in 2027 in this scenario.

Not all is fiscal doom and gloom. Over the long haul, federal finances remain fundamentally sound. But in the short term, there are only tough choices.

Pandemic pressures combined with population aging have brought many provincial health systems to the edge. But there is only so much the federal government can do to help.

Provinces will have to make most of the tough choices themselves.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School…

Recommended for You

Canada’s oilsands are poised to fill global supply gap says industry analyst, as U.S. shale production peaks

‘A big gamble’: Can Canada’s new U.S. trade rep handle high-stakes negotiations with Trump?

What Canada needs to get right in its AI strategy: DeepDive

Canada has a youth extremism problem it can’t continue to ignore