Earlier this month, Fitch downgraded the United States’ long-term credit rating from AAA to AA+. This was not just because of the large and growing federal deficit but also “a steady deterioration in standards of governance.” Regular fights over the debt limit are evidence enough of that.

There are lessons here for Canada.

Before getting to those, though, it’s important to appreciate the troubling scale of U.S. fiscal challenges.

Fitch expects the government deficit there to reach 6.3 percent of GDP this year. For context, that would be more than $180 billion for Canada’s federal government—4.5 times what we anticipate for this year.

Such public borrowing—especially during a period of strong economic performance—is not sustainable. And long-term projections paint an even bleaker picture.

The latest estimates from the U.S. Congressional Budget Office (CBO) project federal debt to reach 181 percent of GDP by the early 2050s—the highest ever, by far. In Canadian terms, that would be well over $5 trillion today.

Something must give. And soon.

Recent research suggests immediate and permanent spending cuts or tax increases equal to 3.1 percent of the U.S. economy are needed to stabilize the U.S. federal debt. That’s massive. In Canada, that would be like tripling the GST. And the longer adjustments are delayed, the harder it will be to fix the budget.

Why does this all matter? Rising debt obviously means more interest payments, which crowds out other priorities. But massive public borrowing affects more than just government finances.

Most significantly, it can weaken the economy by reducing private investment. The CBO estimates that each dollar borrowed cuts private investment by 33 cents, slowing growth and productivity. Higher interest rates are also a strain on individuals, who face higher mortgage rates and other borrowing costs.

Canada is in a better position but should learn from the U.S. experience.

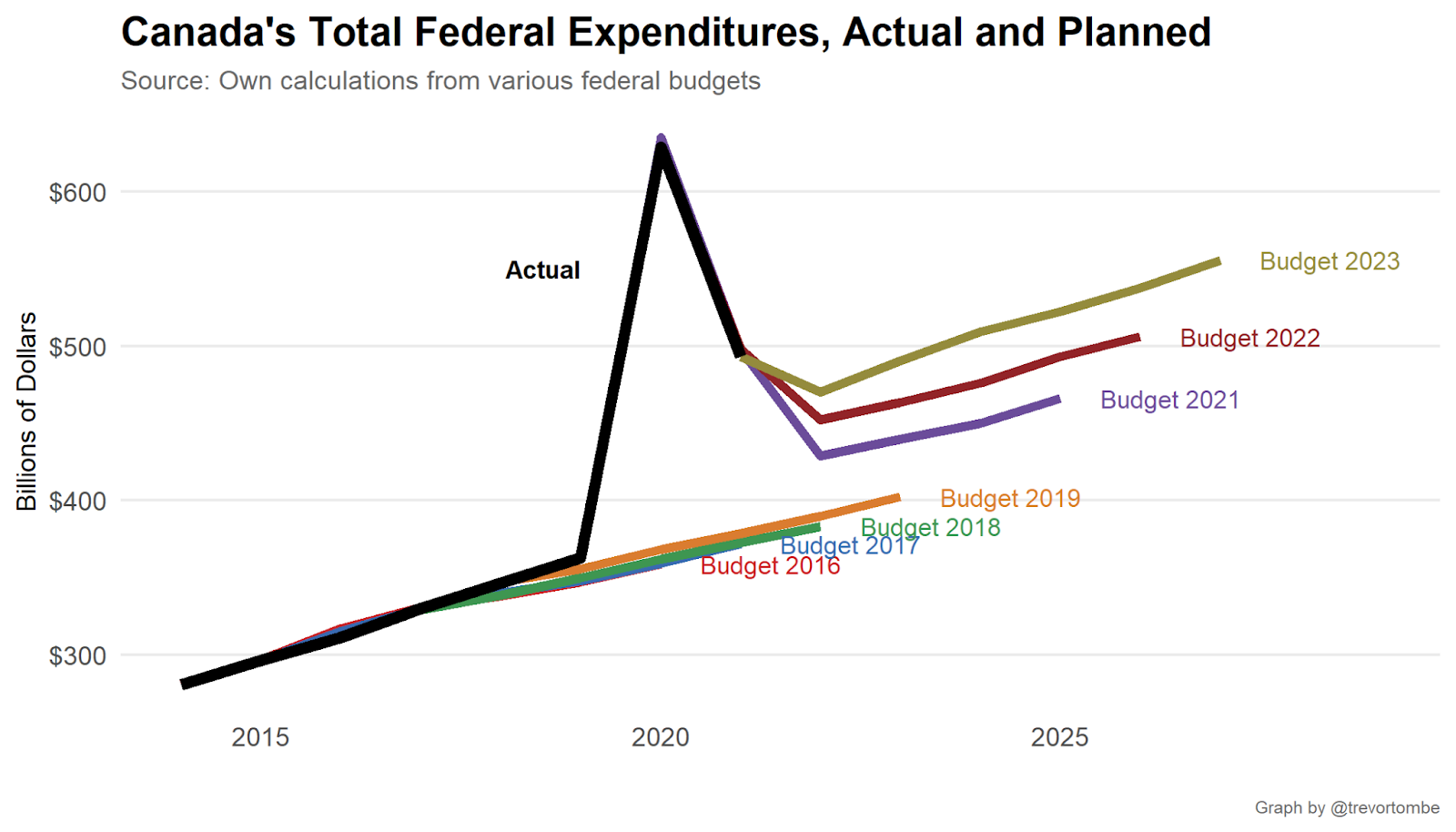

First, while our budget process is cleaner than the American’s (if a budget bill fails, Canadians go to the polls to break the logjam), we could do better. Governments should make financial decisions and stick with them beyond one year.

In recent years, the federal government has consistently increased spending above its own previous plans.

Had total federal program spending this year remained at the level originally planned as recently as Budget 2019, for example, then our more than $40 billion deficit would be a nearly $40 billion surplus.

This isn’t just due to COVID-19. Spending in 2019, for example, was nearly $9 billion higher than originally planned. This has been a consistent pattern that predates the pandemic, though it has grown larger since.

This doesn’t mean that the government can’t spend more. But a prudent and sustainable way to do that is by levying taxes to cover the costs and seeking public support to do so.

Regularly running deficits during times of strong economic performance and full employment is generally unwise. Such periods are the opportune moments for governments to run surpluses and build reserves for future uncertainties.

By accumulating these surpluses, governments can strengthen their balance sheet and prepare for the next inevitable downturn.

Since the end of COVID, Canada’s federal government has done too little of that. This year, debt will be almost 44 percent of GDP—down from its 48 percent peak but still far above the 31 percent before COVID hit.

There are also lessons for provinces. Much of the growth in projected U.S. federal spending is directed toward major health care programs. In Canada, health care is primarily the responsibility of provinces, and our aging population is stretching their finances.

Yet provinces, regardless of political affiliation, consistently fail to plan for this long-term reality. Instead of crafting sustainable policies, they often resort to passing the burden onto the federal government by demanding ever-greater transfers. This act of kicking fiscal cans down the road mirrors the U.S. approach, and it’s fraught with risks.

A sustainable fiscal path requires a firm commitment to responsible long-term policies and clear communication about the choices being made.

Neither is easy. But both are needed to avoid U.S. mistakes.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School…

Recommended for You

‘Another round of trying to pull capital from Canada’: The Roundtable on Trump’s latest tariff salvo

‘We knew something was coming’: Joseph Steinberg on how Trump is ramping up his latest tariff threats against Canada

Rudyard Griffiths and Sean Speer: Canada’s high-stakes standoff with Trump

Canada is losing ground on investment. Here’s where