The rising cost of living is, by far, Canadians’ most pressing concern.

But this challenge goes beyond rising prices. Changes in our income available to spend on food, shelter, clothing, energy, and so on, is also critical to understand. It’s also here where experiences are vastly different. For some, (mainly the elderly) things are improving, a lot; while for others (mainly the young), it’s quite the opposite.

Everyone strains under rising prices. A young person doesn’t pay a different price at the pump than an older person does. While of course we buy different things, which exposes us to different price changes, this doesn’t add up to much todayI estimate young families see a similar average consumer price increase as older ones. They differ by only a few tenths of a percentage point..

But interest rates present a very different, and highly unequal, story.

When rates rise, those with interest-earning investments tend to benefit while those with debts, of course, do not. This is obvious. It might also be obvious that the young have more debt than the old. What is not widely understood, however, is the sheer magnitude of the gains and losses resulting from recent rate changes and the systematic (and ongoing) redistribution from young to old that they have caused.

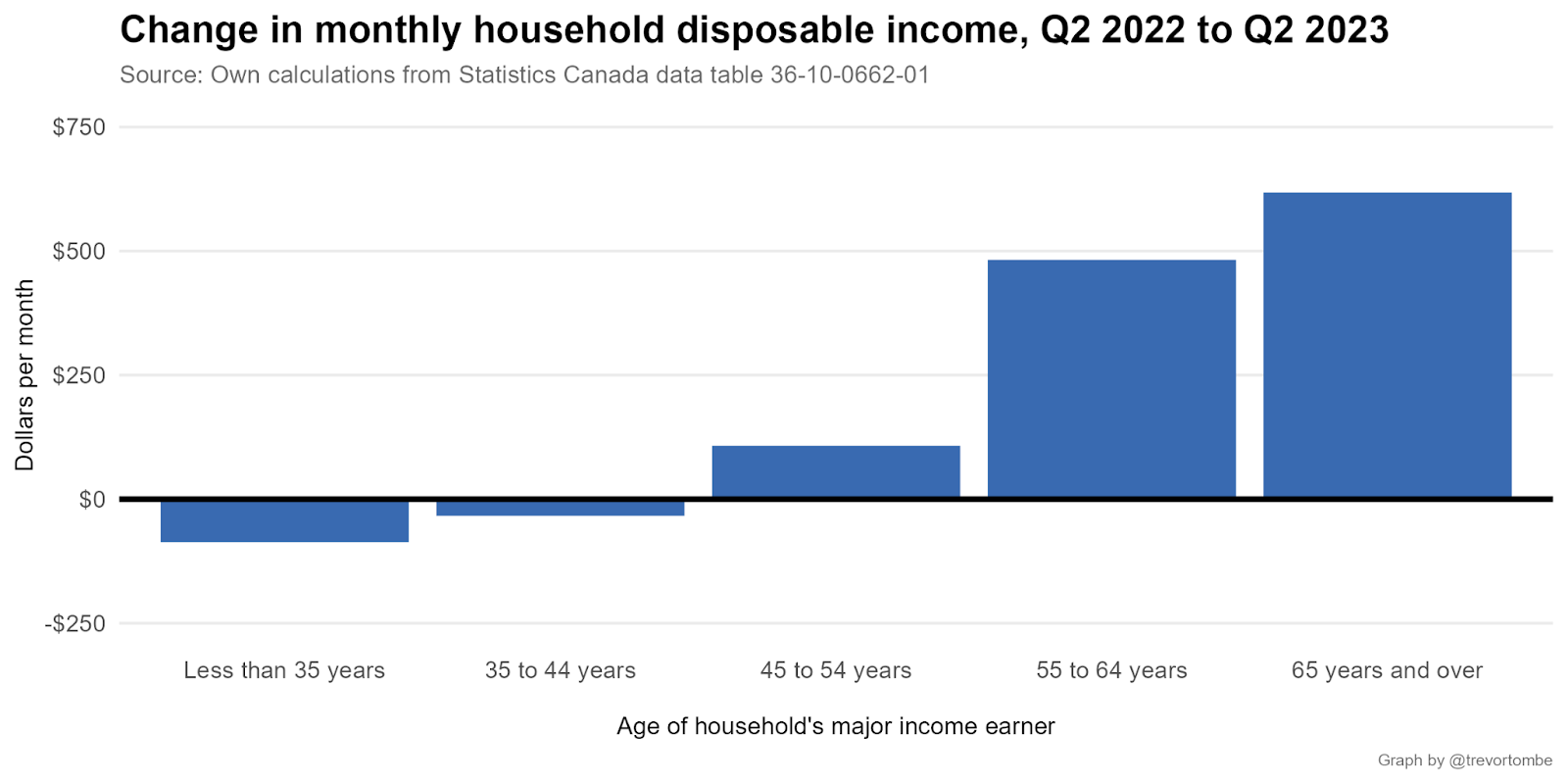

To see this, consider household disposable incomes. Using the latest data released by Statistics Canada earlier this month, I plot changes over the past year below. It shows a stark difference between older households, who saw their disposable incomes rise sharply by over $600 per month, and younger ones, who have seen their disposable incomes drop.

Importantly, this particular measure not only subtracts taxes from a person’s total income but also subtracts interest payments on their debts. This provides a clearer picture of a household’s ability to consume or save out of whatever is left over.

This is particularly important today. Higher interest rates are a major reason why old people are doing better and young people are doing worse.

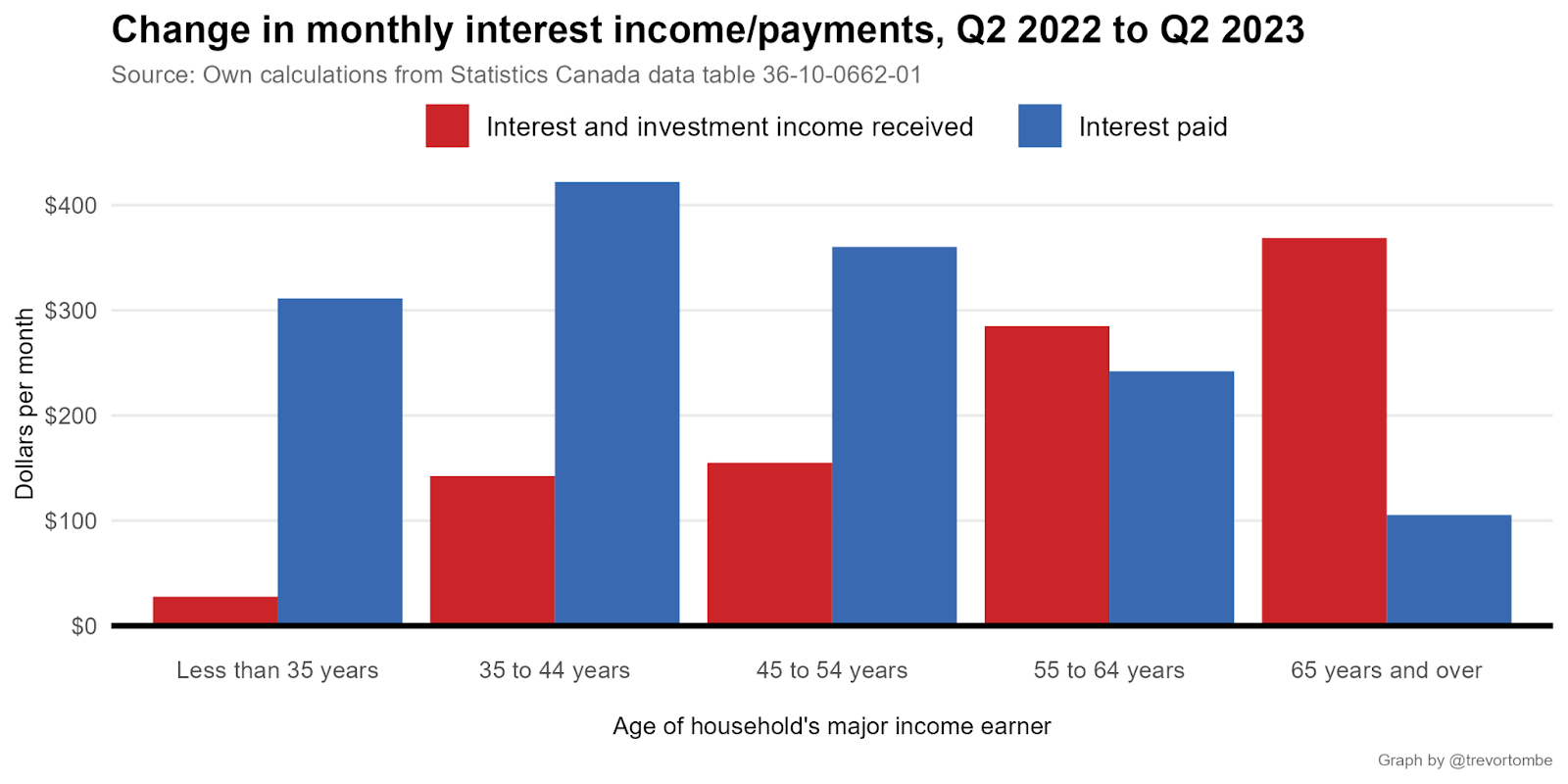

Below I plot changes in interest earned (from savings) and interest paid (on debts). Since the second quarter of last year, interest payments by the average household rose by $263 per month. For younger households, the increase was significantly greater, as much as over $400 per month for those in their late-30s and early-40s. This contrasts sharply to the only $100 per month increase among those 65 and over.

There is an even larger difference in interest income. For the youngest households, interest-earning investments are negligible, so rising interest rates have had little effect. For the oldest households, however, the income boost was nearly $370 per month.

In total, the youngest households paid nearly $1 billion more per month in interest. And net of higher interest earnings, those under 45 collectively paid over $1.6 billion more. Those over 65, meanwhile, received $1.6 billion per month more.

This is a massive shift. It is roughly comparable to a four percent tax on the disposable incomes of those under 35 and a nearly seven percent subsidy to those over 65.

Even with rising consumer prices, elderly households come out ahead.

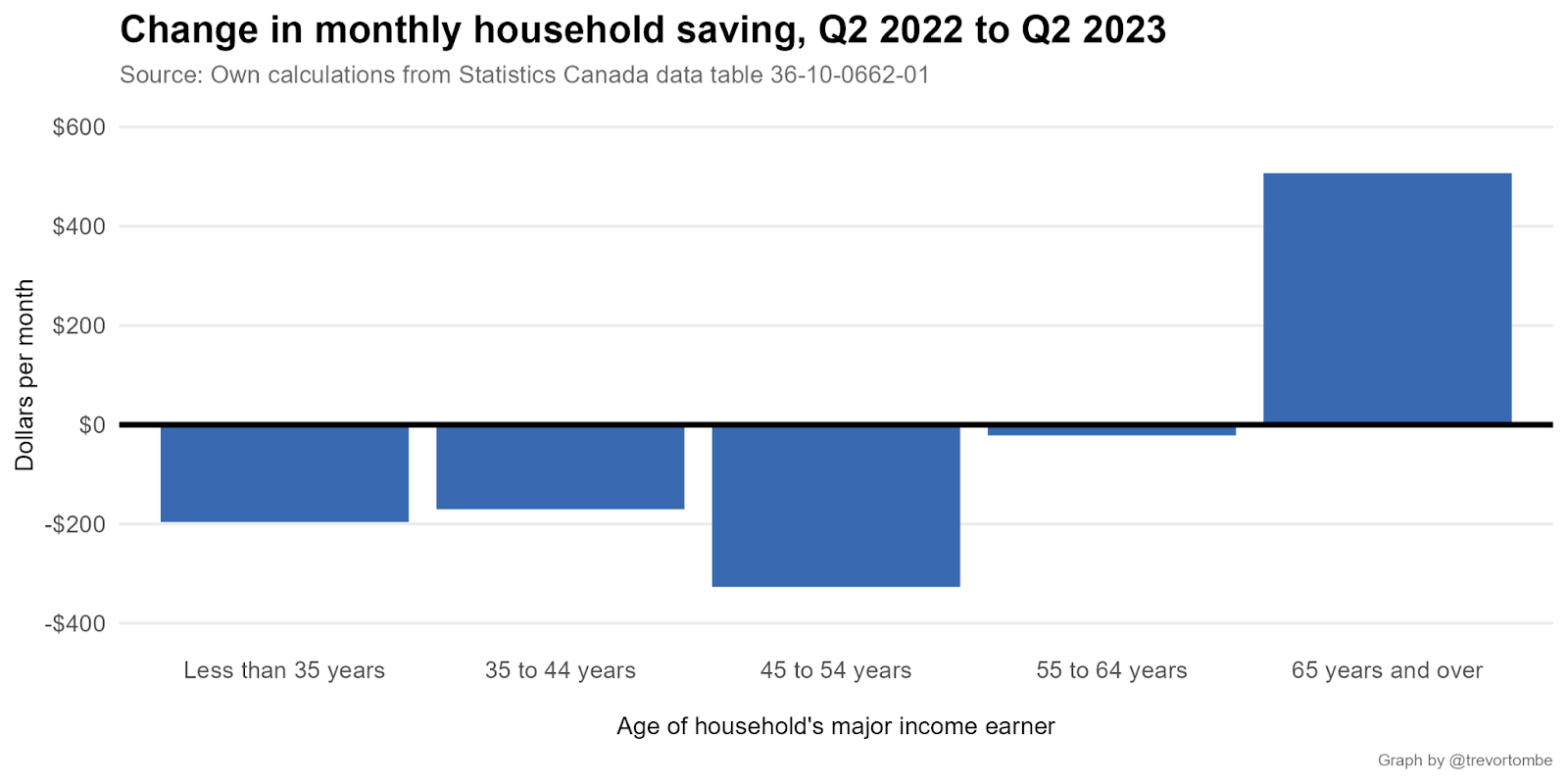

For all but the oldest households, as I show below, savings are falling as households try to make ends meet. The young are saving $200 per month less than they did a year ago while those age 45 to 54 are saving $327 per month less. Those age 65 and over, meanwhile, savings are up over $500 per month compared to last year. For them, rising prices increase monthly expenses, sure, but by less (on average) than their incomes are rising.

To be absolutely clear, this isn’t a criticism of the Bank of Canada. We rightly mandate it to keep inflation at two percent per year. That’s a heavy lift (and mistakes, of course, happen) but they have precious few tools at their disposable. Today, they are right to increase rates in an effort to slow consumer and business spending.

This also isn’t a criticism of older Canadians, who worked hard to accumulate savings that they are now benefiting from. That’s fair enough.

Instead, I mean to shine a light on a new economic development that some governments are only making worse and, perhaps, not even aware of. At the very least, governments should reconsider the increasingly generous supports they provide to older Canadians. Alberta, for example, provided $100 per month to seniors for several months to compensate for rising prices, despite their monthly disposable incomes rising much more than spending.

The federal government has also enacted policies to benefit seniors, with increases to various income support programs from GIS to OAS. Going forward, for this and many other reasons, we could consider raising OAS eligibility again from 65 to 67. (This was previously done, though later cancelled for short-term political reasons.)

This is all easier said than done. Elderly individuals vote in greater numbers, so the political challenge is clear.

But as economic pressures mount, and especially if interest rates remain higher for longer, increasingly difficult fiscal decisions will be required. We should take care to ensure that when those decisions are taken, young people are not unfairly saddled with the heaviest burdens while other Canadians are spared.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School…

Recommended for You

Laura David: Red pill, blue pill: Google has made its opening salvo in the AI-news war. What’s Canadian media’s next move?

The Notebook by Theo Argitis: Mark Carney’s first major tests

The Weekly Wrap: Trudeau left Canada in terrible fiscal shape—and now Carney’s on clean-up duty

Ben Woodfinden: Lament for an ‘elbows up’ nation