Prime Minister Carney has been talking a lot about the need for “nation-building projects” to boost economic growth, diversify Canada’s economy, and ramp up exports to global markets. This language represents a refreshing, albeit long overdue, shift in federal policy direction.

The problem is that, in recent decades, Canada’s economic value hasn’t come from exporting more goods into new markets or from expanding the range, complexity, or value of what it creates. Nor has it come from big leaps in tech, science, or innovation. Instead, the Canadian economy has mainly been powered by real estate.

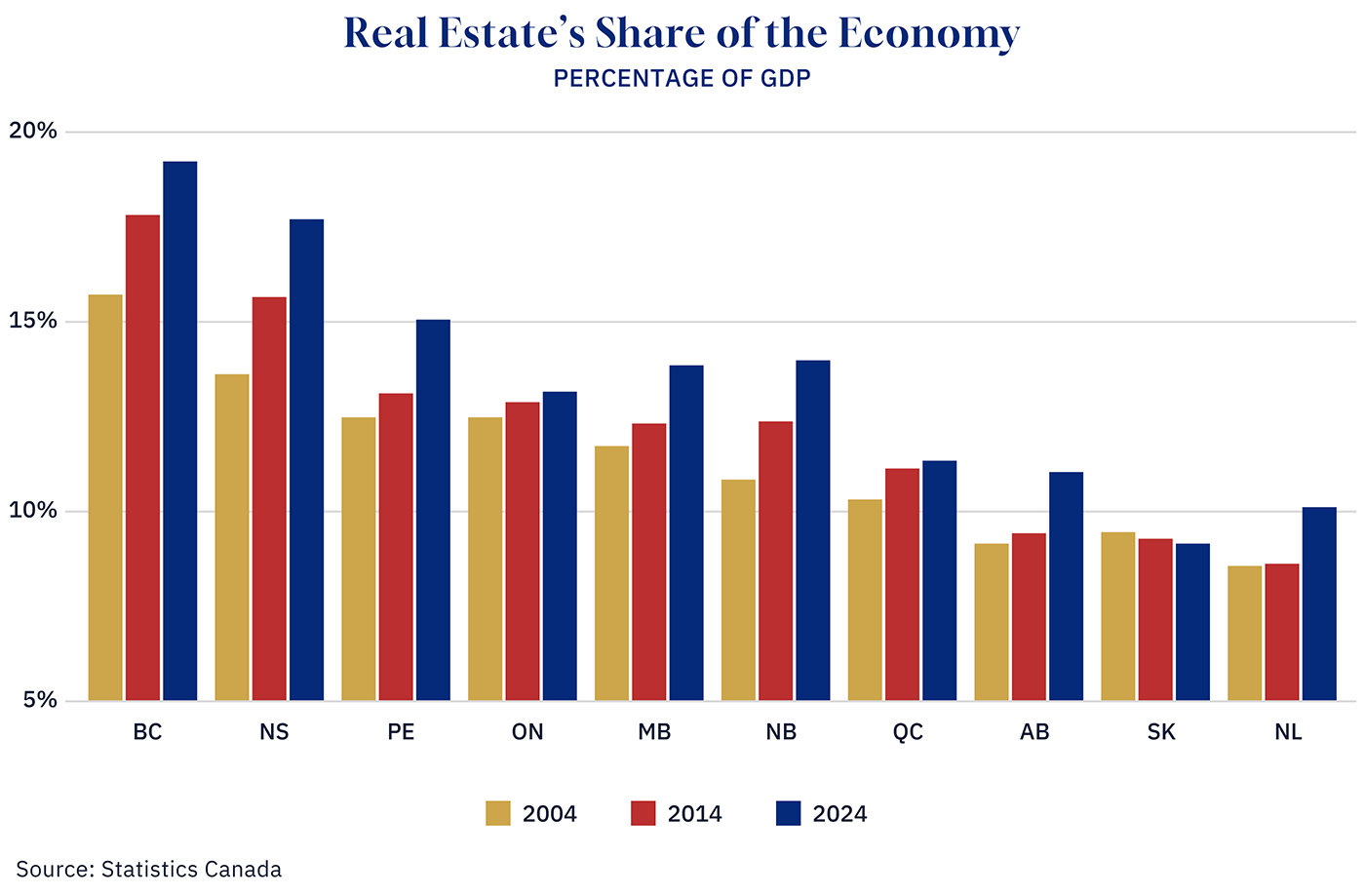

As of 2024, the real estate industry was the largest industry in six of 10 provinces and the second largest in the remaining four, behind only manufacturing in Quebec and oil and gas in Alberta, Saskatchewan, and Newfoundland and Labrador. And the importance of real estate to the overall economy continues to grow.

On average, individual provinces generate about 13 percent of their economic value from real estate. This includes income from rent—or, for homeowners, the equivalent value of living in their home—as well as services provided by property managers and realtors.

Graphic credit: Janice Nelson.

Though the sector is sizeable in all provinces, it’s especially big in B.C. Nearly 20 percent of B.C.’s economic value now comes from this sector, up from 16 percent a couple of decades ago. While not as high, the Atlantic provinces and Alberta have also seen a notable increase in the sector’s importance over recent decades—and, in Alberta’s case, especially in recent years.

To be sure, Canada is far from being dominated by the sector. One measure of industry diversification—something known as the Herfindahl–Hirschman index—suggests no province is overly concentrated in any sector, including real estate. Additionally, the sector’s contribution to GDP is not far out of step with other rich countries. After all, real estate provides an essential service for Canadians.

What’s worrying is that the sector’s importance continues to grow while others wane, shifting employment and resources away from sectors that tend to be more productive, pay better wages, and have more potential to drive long-term growth. When real estate leads an economy, it’s not usually a sign of rising incomes or economic strength. More often, it’s linked to booms, busts, and financial risk. Another challenge is that just because the real estate sector is growing doesn’t necessarily mean the economy is creating more value—it could just mean people are paying more in rent. The tools economists use to account for inflation don’t always pick up on all the quirks of the housing market.

All this to say: a renewed focus on those other sectors would be a welcome shift. Hopefully, what drives the Canadian economy will look a little different in another decade.

A version of this post was originally published by the Business Council of Alberta at businesscouncilab.com.

Alicia Planincic is the Director of Policy & Economics at the Business Council of Alberta. She regularly provides insight and analysis on…