DeepDives is a bi-weekly essay series exploring key issues related to the economy. The goal of the series is to provide Hub readers with original analysis of the economic trends and ideas that are shaping this high-stakes moment for Canadian productivity, prosperity, and economic well-being. The series features the writing of leading academics, area experts, and policy practitioners. The DeepDives series is made possible thanks to the ongoing support of the Centre for Civic Engagement.

This month, the United States Congress passed President Donald Trump’s One Big Beautiful Bill, which, among other things, extended and made permanent the income tax rate reductions and revised tax brackets first brought in through the 2017 Tax Cuts and Jobs Act, namely a 2.6 percentage point cut to the top bracket. This should raise alarm bells for policymakers north of the border, as Canada will continue to have uncompetitive personal income tax rates compared to our American counterparts and fall even farther behind in the race to attract entrepreneurs, professionals, investors, and top talent.

Jurisdictions around the world compete to attract and retain top talent, including entrepreneurs, engineers, and doctors, who contribute significantly to their economies. According to research, taxes have the greatest impact on the mobility of high-skilled individuals. For example, relatively high personal income tax (PIT) rates in one jurisdiction may incentivize workers to reduce their tax burden by relocating to a lower-tax jurisdiction. This creates competition between jurisdictions, with the jurisdictions with the lowest taxes typically more successful at attracting and retaining professionals, business owners, and entrepreneurs.

According to a study in the American Economic Review, the number of “star” scientists in a state increases by 0.4 percent annually if the after-tax income in that state increases by 1 percent due to a reduction in PIT rates. Put differently, high-income scientists are acutely sensitive to personal income taxes and make decisions about where to work in part based on the level of taxation in a given jurisdiction.

Similarly, economists Agrawal and Feremny found that workers in finance, real estate, and healthcare are more sensitive to taxes, thus more likely to migrate than other professionals.

Research from the National Bureau of Economic Research similarly found that “superstar” inventors are significantly influenced by top tax rates when deciding where to locate. Another study on international mobility examined the exodus of Canadian professionals to the U.S. It determined that high-skilled Canadians respond strongly to tax rates. According to the report, a “1 percent increase in the existing tax gap (measured by the ratio of total tax revenue to GDP) can push 2 percent more Canadians toward the United States.”

The effect also shows up in international professional sports. Economist Henrik Kleven and his colleagues examined data on European soccer players and found that countries with low taxes attract more “high-ability players” who have high rates of compensation. Among NHL fans and hockey pundits, there has been recent discussion about the Florida Panthers having an advantage in attracting the most talented hockey players because they do not pay state-level income taxes. Big names such as Sam Bennett, Aaron Ekblad and Brad Marchand recently re-upped with the Panthers on bargain contracts, in part due to relatively low tax rates. Meanwhile, big-name Mitch Marner left the Toronto Maple Leafs this summer for greener pastures and substantially lower taxes (with sunny weather) in Nevada by signing a lucrative eight-year contract with the Vegas Golden Knights.

Five of the last six Stanley Cup-winning teams have come from U.S. states that do not impose state-level income taxes (the Colorado Avalanche being the exception). And again, although taxes are not the sole factor in any player’s career decisions, they are undoubtedly a key reason why these teams successfully manage the salary cap and build the best possible roster.

Why does this matter for Canada?

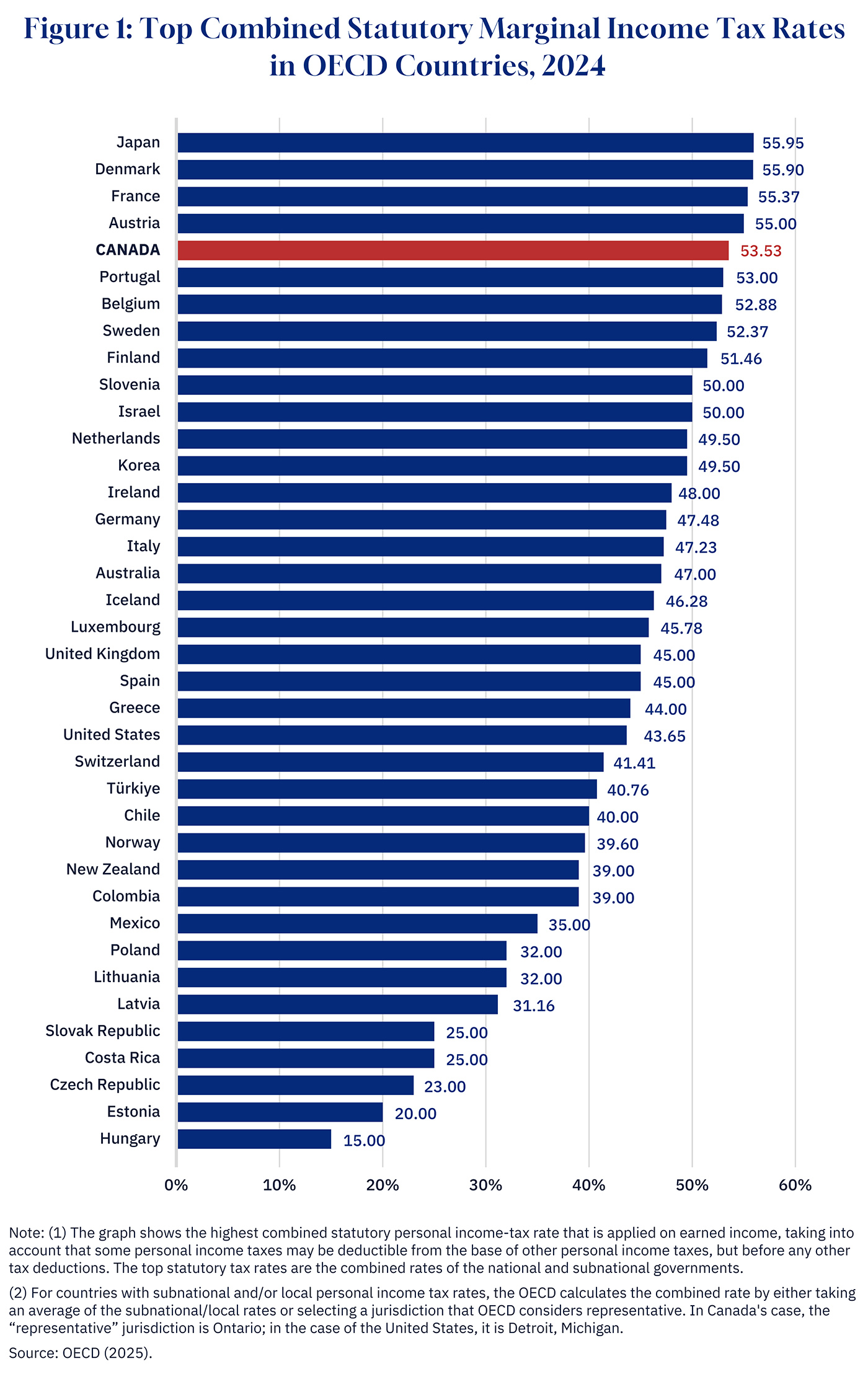

Canada’s personal income tax (PIT) rates are uncompetitive compared to those of other advanced countries. Among the 38 countries within the Organization for Economic Cooperation and Development (OECD), Canada’s personal income tax system is ranked the seventh-least competitive.

In 2024, Canada’s top combined (federal and provincial) PIT rate was the fifth-highest among the 38 high-income countries, as illustrated in Figure 1 below. Our combined PIT rate is higher than Australia (17th), the United Kingdom (20th) and the U.S. (23rd).

Graphic Credit: Janice Nelson

Over the last decade, tax hikes at the federal and provincial levels have increased top PIT rates in every province. For example, the Trudeau government in 2015 raised the top federal PIT rate from 29 percent to 33 percent. Provinces such as Alberta, British Columbia, and Newfoundland and Labrador followed suit.

The Carney government has shown little interest in changing course. While the prime minister cancelled Trudeau’s planned capital gains tax hike, he has done little else to attract or retain top talent. Instead, his government changed the bottom federal PIT rate from 15 percent to 14 percent on income below $57,375 CA. While this move may slightly improve Canada’s competitiveness for lower- and lower-middle-income workers, it does almost nothing to make the country more attractive to doctors, scientists, engineers, and entrepreneurs (and, yes, athletes).

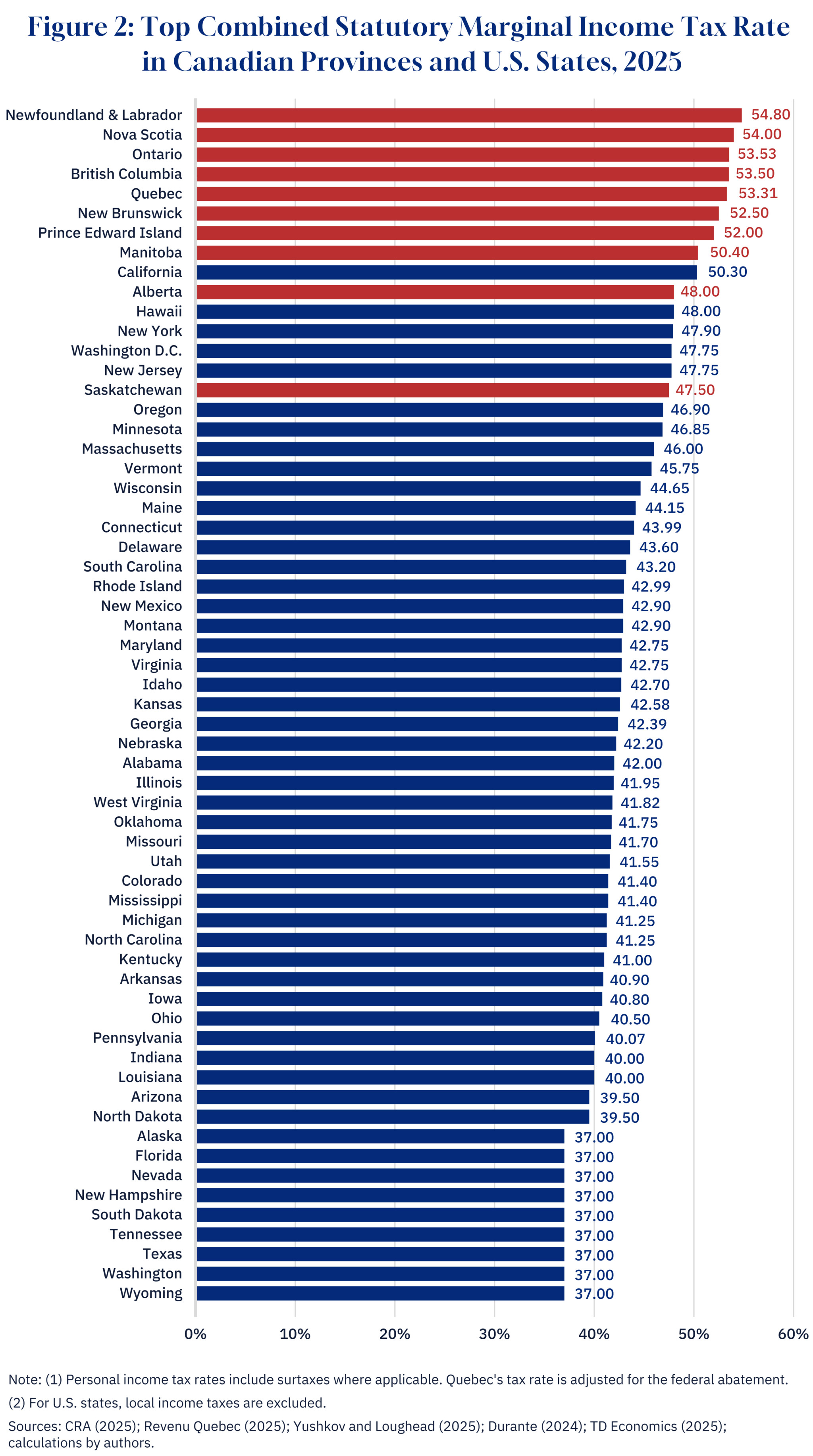

While Trump’s Big Beautiful Bill helped solidify the U.S. advantage, it exacerbated Canada’s competitiveness problem. If we compare PIT rates in the 10 Canadian provinces to the 50 U.S. states and the District of Columbia, the scale of our problem becomes apparent (see Figure 2).

Specifically, when ranking the top combined (federal and provincial/state) PIT rates in 2025, Canadian provinces hold nine of the top 10 highest rates among the 61 American and Canadian jurisdictions. Saskatchewan (at 15th highest) is the only province to escape the 10 top 10.

Graphic Credit: Janice Nelson

Newfoundland and Labrador has the highest top PIT rate (54.80 percent) among Canadian and U.S. jurisdictions, followed by Nova Scotia (54), Ontario (53.53), Quebec (53.31 percent) and New Brunswick (52.50). Compare this to top PIT rates as low as 37 percent in Texas, Florida, Nevada, Washington and Tennessee, which impose no state-level personal income taxes.

In addition to the rate differences, there are also differences in income thresholds. For instance, in Ontario, the top combined PIT rate (53.53 percent) kicks in at $253,414 CA compared to $1,384,538 CA in California, a notoriously high-tax state.

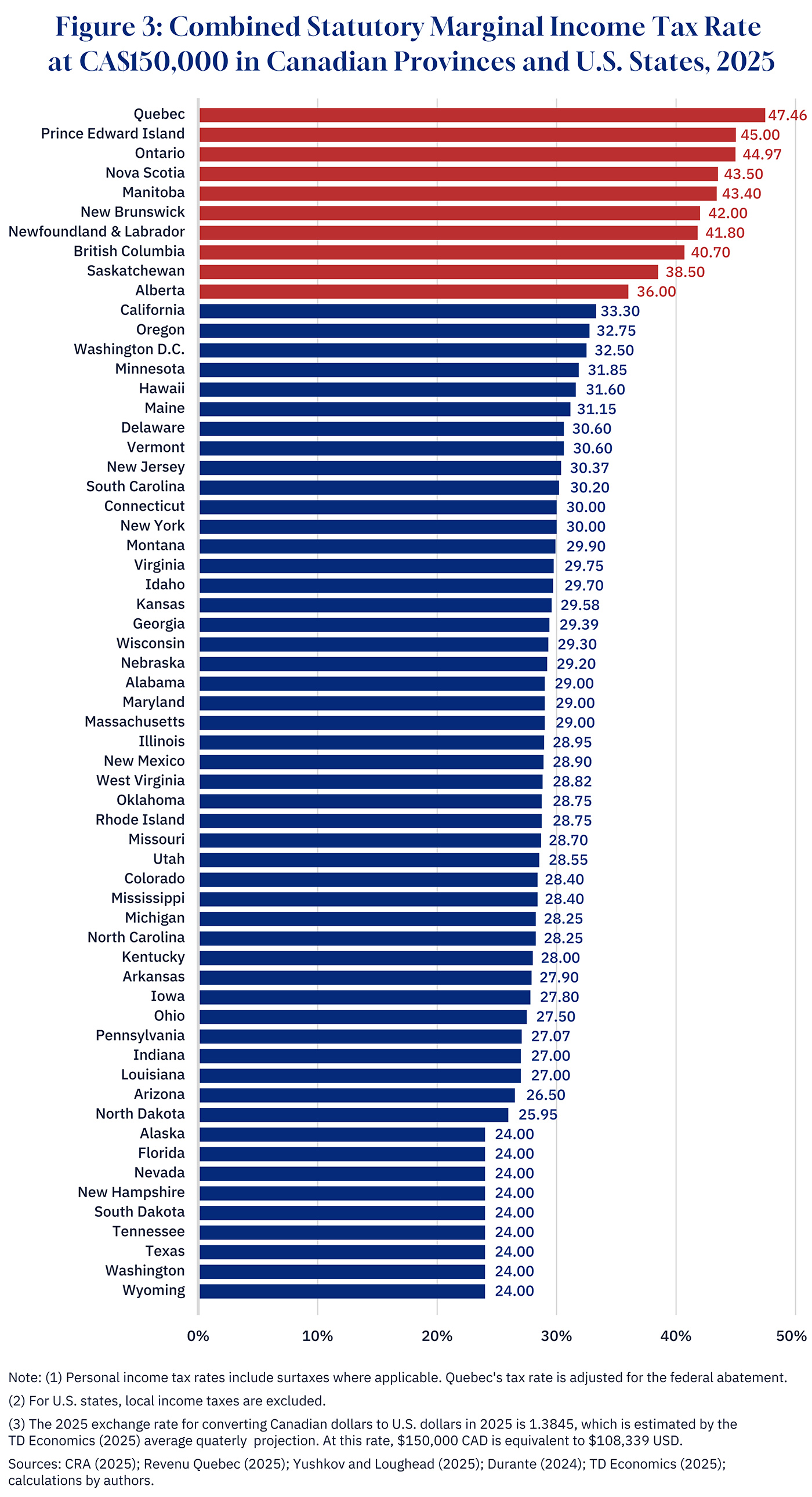

In addition to top earners, Canada’s PIT rates are also uncompetitive at other income levels. At $150,000 CA, Canadians in all 10 provinces face higher PIT rates than Americans in every U.S. state (see Figure 3), with the highest rates in Quebec (47.46 percent), Prince Edward Island (45) and Ontario (44.97). While Albertans enjoy the lowest rate (36) in Canada, it’s still higher than in California (33.30 and at $150,000 CA, nine U.S. states have combined (federal and state) income tax rates at 24.0 percent.

Graphic Credit: Janice Nelson

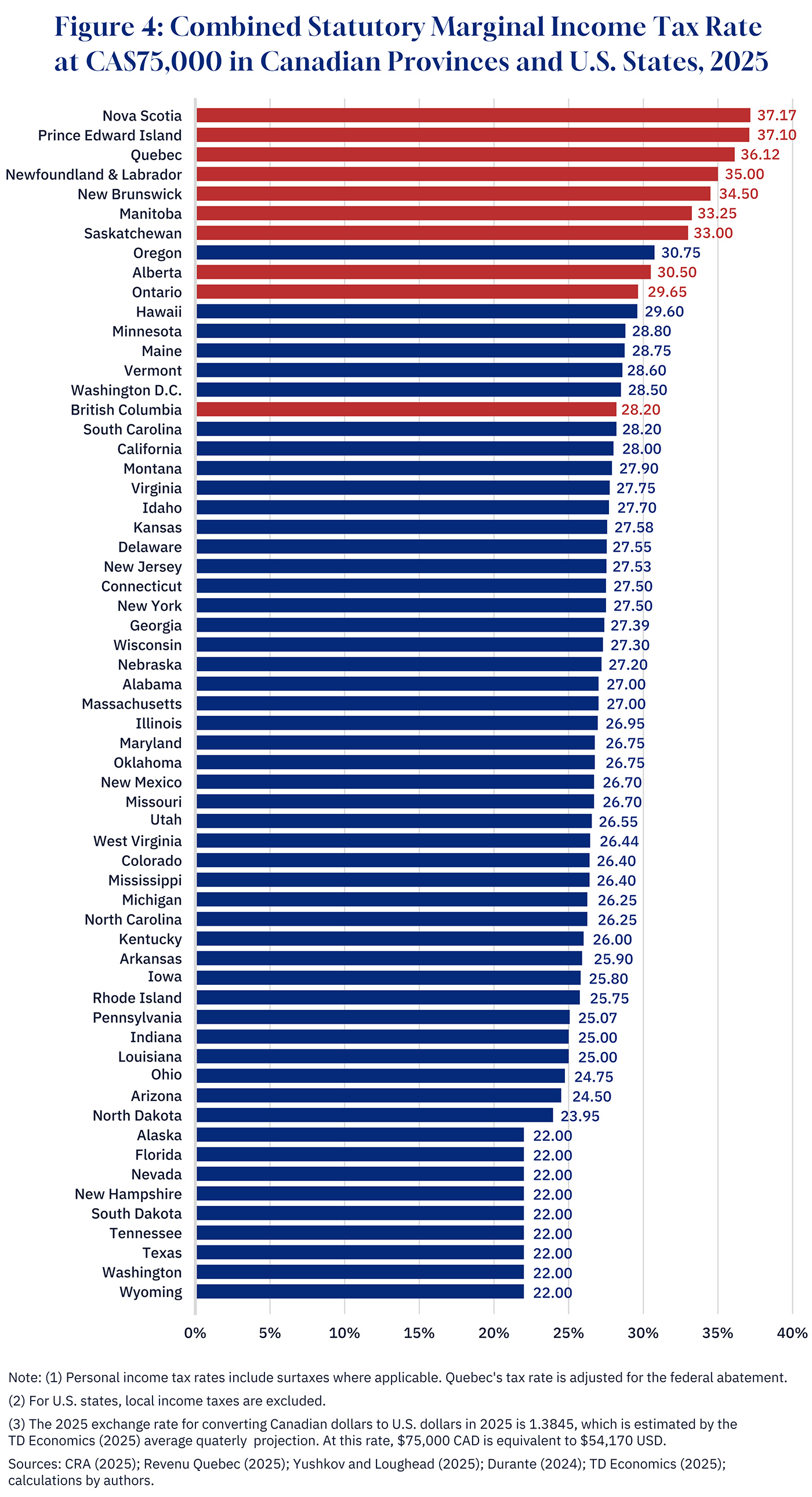

If we move down the income ladder to $75,000 CA (see Figure 4 below), Canadian provinces hold nine of the top 10 highest PIT rates, starting with Nova Scotia (37.17 percent), P.E.I. (37.10) and Quebec (36.12). Americans living in geographically similar states, such as New Hampshire (22 percent), Vermont (28.60), and Maine (28.75), all face significantly lower PIT rates than their Canadian counterparts in the Atlantic region. Oregon (30.75 is the only U.S. jurisdiction in the top 10, and B.C. (28.20 is the only Canadian province outside of the top 10.

Graphic Credit: Janice Nelson

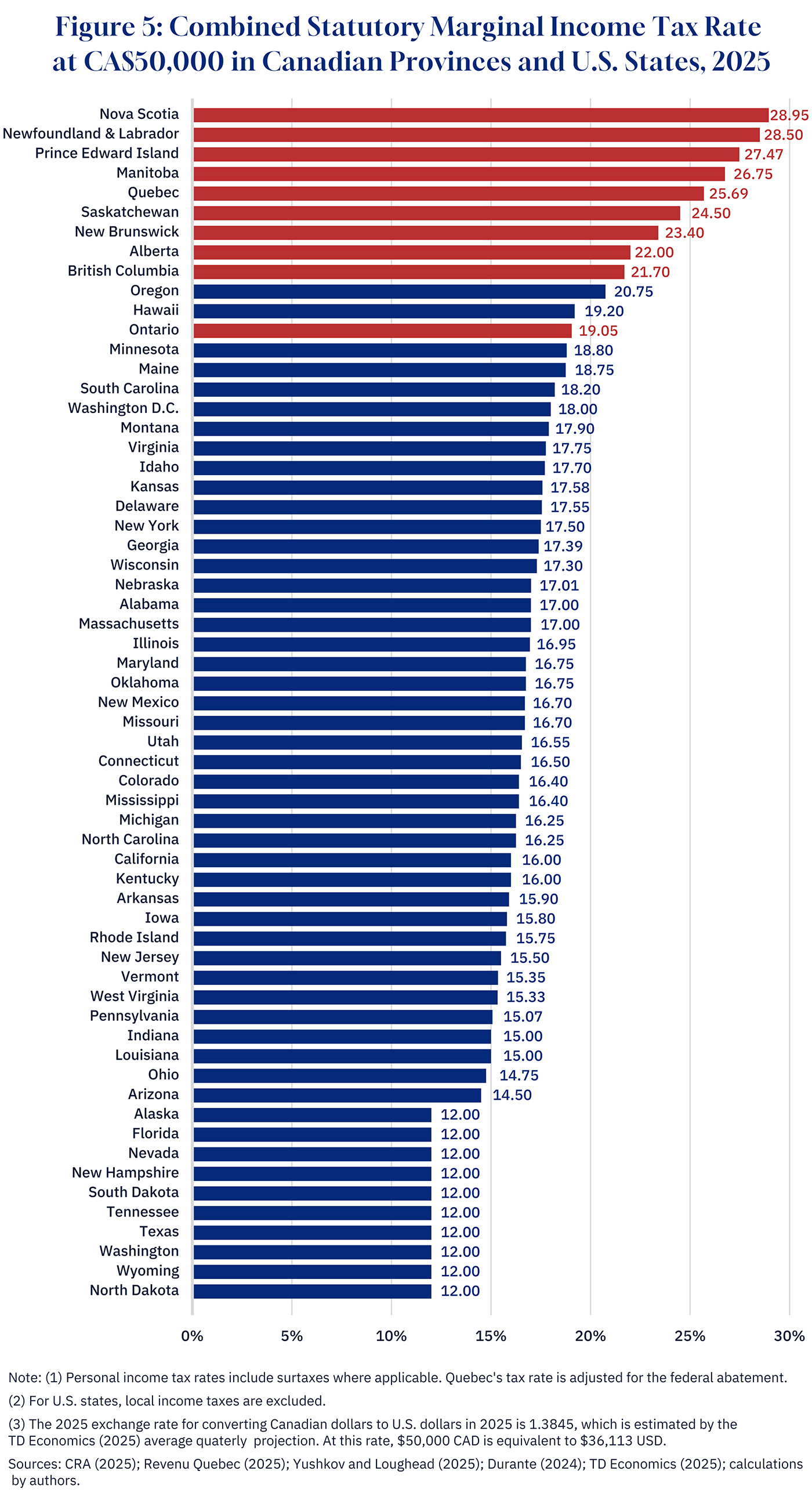

Finally, PIT rates in Canada are also uncompetitive at $50,000 CA (see Figure 5 below). Again, Canadian provinces hold nine of the top 10 highest rates, while the remaining province sits at 12th in the rankings. Nova Scotia (28.95 percent) once again has the highest rate, followed by Newfoundland and Labrador (28.50), P.E.I. (27.47) and Manitoba (26.75). Ontarians face the lowest rate in Canada at this income level, but still pay a higher rate than Americans in 48 states plus the District of Columbia. In Nevada, New Hampshire, Florida, and Texas, workers pay a 12 percent tax rate on the first $50,000 CA of their income.

Graphic Credit: Janice Nelson

Across all income levels examined, a couple of trends emerge. First, residents in energy-producing provinces, such as Alberta, Saskatchewan, and Newfoundland and Labrador, consistently pay PIT rates that exceed those in comparable energy-driven states, including Texas, Oklahoma, Alaska, Wyoming, North Dakota, West Virginia, and New Mexico, with which they directly compete for investment and talent. For example, Alberta’s top combined PIT rate is 11 percentage points higher than in Texas, Wyoming and Alaska. Newfoundland and Labrador fares even worse, with top PIT rates 17.40 percent higher than in those U.S. jurisdictions.

Another obvious trend is that Canadian jurisdictions have higher income tax rates, at both the lower and top ends of the income spectrum, than virtually all U.S. states. In other words, the provinces with the lowest rates are generally less competitive than states with the highest tax burdens in the U.S. That’s a big problem for a Canadian economy already struggling to increase productivity, innovation and living standards. These comparably high tax rates reduce the incentives to save, invest, and start a business—all key drivers of prosperity—while deterring top talent from relocating to Canada.

The problem worsens when we look beyond taxes towards the multitude of regulatory barriers businesses must sift through, which scares away investors and entrepreneurs. According to the Canadian Federation of Independent Business, Canadian businesses spent an estimated $51.5 billion CA, and an average of 735 hours, on regulatory compliance in 2024. Imagine what business owners and entrepreneurs could do with their time and money spent on innovation instead. Add in relatively high housing prices and cold winter weather in many parts of the country, and it’s difficult to see why professionals, business owners and entrepreneurs would consider relocating to a Canadian city today.

Make no mistake, Canada has immense potential. We have an abundance of natural resources, a highly educated workforce, and many young people clamouring for a better future. But we cannot realize that potential if our policymakers are not bold and daring enough to change course.

Creating an environment to foster higher living standards for Canadians means we must meaningfully reduce taxes to make us substantially more competitive with our American neighbours and other industrialized countries around the globe. Tinkering around the edges of our tax system with a small tax reduction here or there will simply not get it done. To attract and retain top talent, Ottawa and the provinces must give high-skilled people a robust reason to make Canada their home. Why not start with making Canada the most competitive tax system in the world?