Canada’s economy may be struggling, but at least our national pension plan is secure.

Now worth $732 billion, the fund is projected to be “financially sustainable for at least the next 75 years,” and that may be an understatement. Compare that to U.S. Social Security, where the trust used to fill the gap between contributions and payments is expected to run dry in less than a decade. Across the border, the debate is between three bad options: cutting benefits, increasing taxes, or hiking the earnings cap.

Canadians can feel pretty good: proud of the CPP’s investment track record and relieved we’re not facing the same funding headaches as in the U.S. But some argue the plan is overfunded and that money shouldn’t be locked away. Instead, it should all be returned to Canadians through higher payouts, lower contributions, or even redirected to other priorities.

The reason the fund has ballooned is simple: unlike in the U.S., contributions exceed payouts. Those extra dollars are invested—in stocks, bonds, and other assets—earning an annual return of around 8 percent over the past decade. That’s doubled the size of the fund in just 10 years, and, by 2031, it’s expected to top $1 trillion.

The reason some don’t see this as a good thing is that strong returns don’t mean more money for Canadians. Benefits are based on things like how much you contributed and for how long, not by how well the fund performs. For most Canadians, the return they’ll see is less than 3 percent. Which means more than $22,000 per Canadian is sitting in the CPP just to be absolutely, positively sure the fund remains solvent.

Graphic credit: Janice Nelson.

But while there may be room to slightly reduce contribution rates and/or increase payouts, taking this too far would be risky.

For one, drawing down the CPP fund comes with a risk of the fund’s future sustainability— which was what prompted reform in the late 1990s, including higher contributions and the introduction of a reserve fund. Right now, contributions are set at 9.9 percent, just a hair above the 9.56 percent the chief actuary says is needed to keep the plan on track. If the fund were smaller, it would be less able to protect Canadians against weaker investment returns, a recession, or the demographic pressures expected.

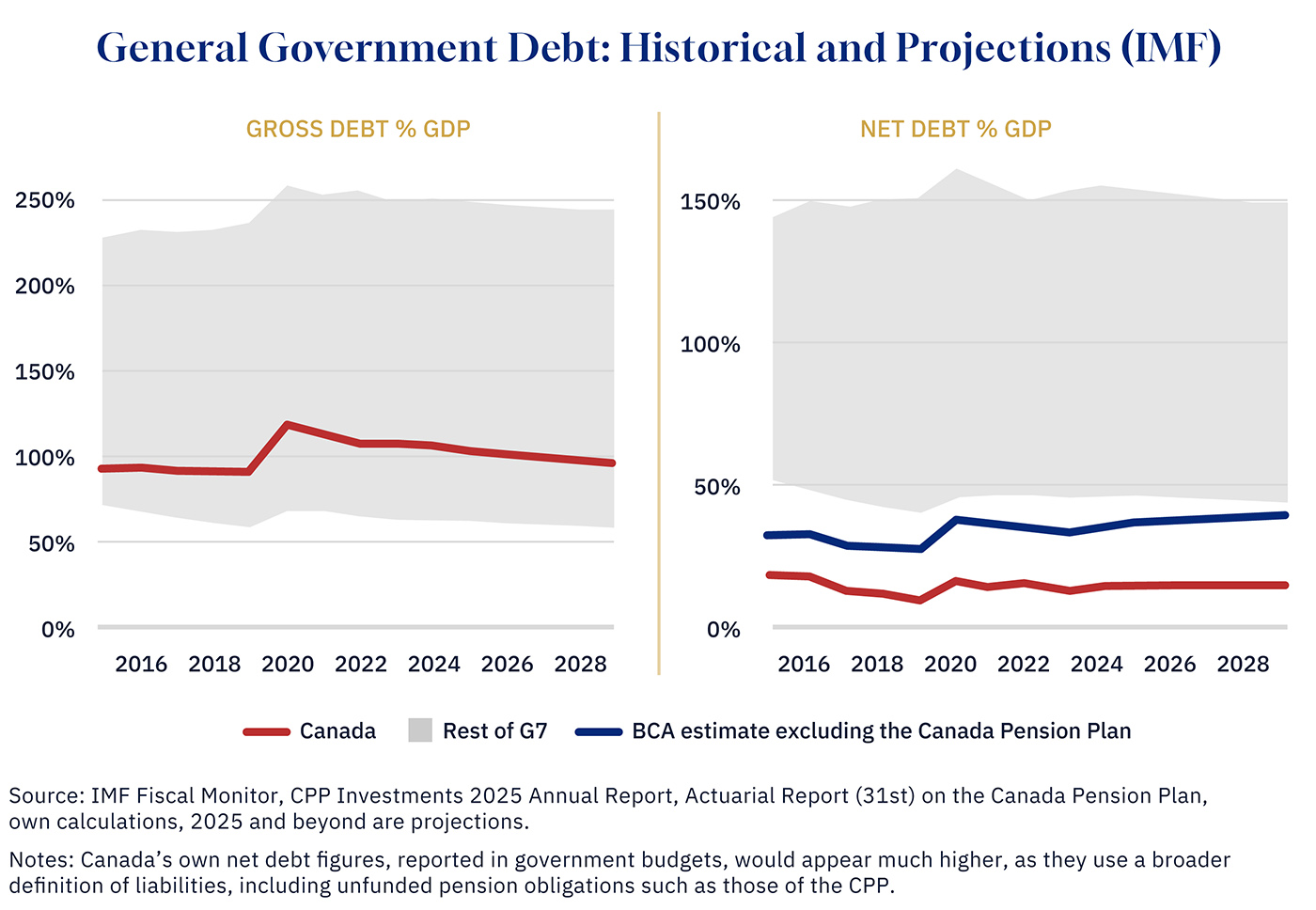

And second, it would significantly worsen Canada’s debt position. Total government debt in Canada is high compared to many other countries, but our net debt picture actually looks pretty good because our gross debt is partially offset by large financial assets like the CPP—assets, which, in theory, could be used to repay lenders.

That picture would shift dramatically if Canada were to deplete the CPP as some have proposed. In fact, our net debt would more than double. While that would still compare favourably with other G7 countries, such a sharp deterioration could raise investors’ concerns about Canada’s ability to manage its debt.

To be clear, the CPP’s purpose isn’t to prop up the country’s balance sheet. But that is nonetheless a benefit of such a large and well-funded plan. Keeping a strong financial buffer is necessary to protect both the CPP and the country’s fiscal health.

A version of this post was originally published by the Business Council of Alberta. To learn more, read the article here.

Alicia Planincic is the Director of Policy & Economics at the Business Council of Alberta. She regularly provides insight and analysis on…