The Carney government’s recent announcement to rename and enhance the GST credit—at a cost of $11.7 billion—is symptomatic of a broader Canadian problem. While framed as affordability relief, the harder truth is that it represents yet another instance of a leveraged nation borrowing to fund current consumption.

A federal government running a nearly $80 billion deficit is effectively spending money it doesn’t have to patch immediate pressure points. This isn’t a critique of helping families manage costs; it’s an observation about where Canada now stands. We have become one of the world’s most indebted nations.

When households, corporations, and governments are simultaneously highly leveraged, our ability to respond to crises shrinks dramatically. Whether the next shock arrives as a trade war, a recession, or something unanticipated, we’ll face it with far less room to maneuver than we imagine.

The uncomfortable truth about Canadian debt

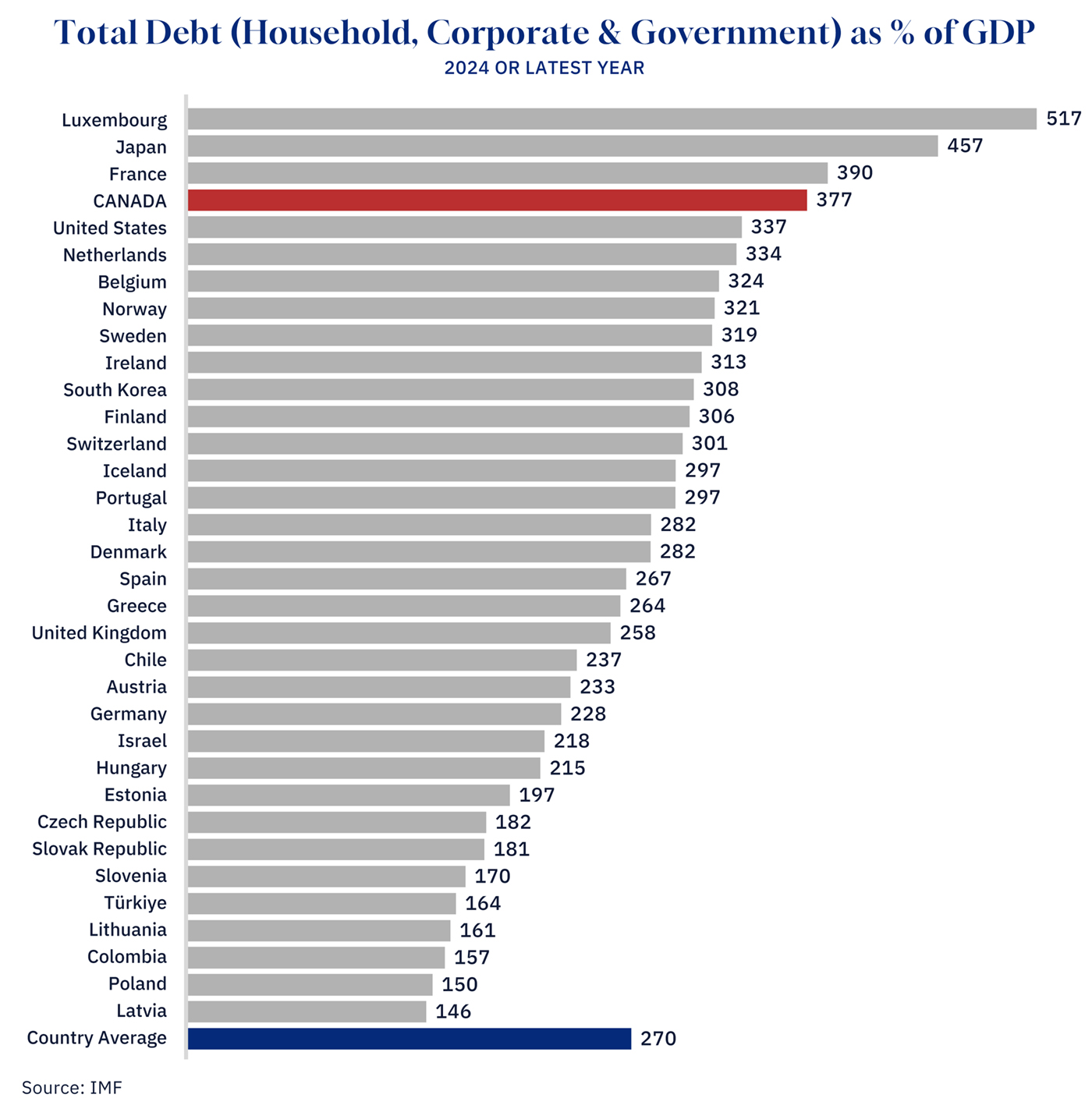

Canada ranks fourth in total indebtedness among 34 OECD countries, according to data from the International Monetary Fund. Our aggregate household, corporate, and government debt has reached 377 percent of GDP, a burden surpassed by only Luxembourg, Japan, and France.

What makes Canada’s situation particularly concerning is that this debt is spread systematically across all sectors (households, corporations, and governments) alike.

Graphic Credit: Janice Nelson.

Households: Living beyond our means

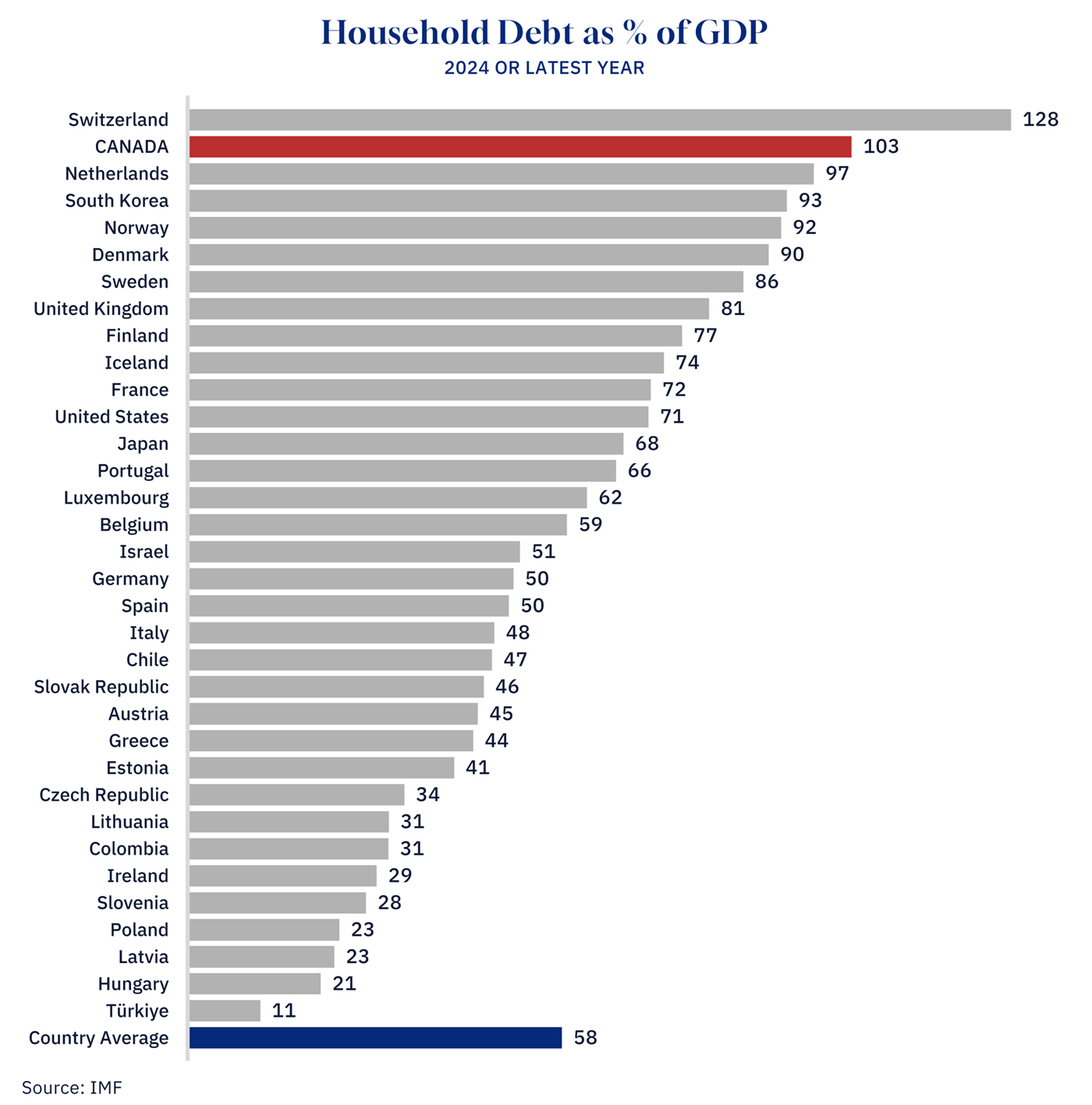

Canadian households carry debt equal to 103 percent of GDP, the second-highest among the 34 OECD countries examined, after only Switzerland.

To put this in perspective, the average household debt burden across these nations is just 58 percent of GDP. While much household debt is mortgage debt backed by assets, we’ve still borrowed nearly twice as much, relative to our economy, as the typical advanced nation.

Even the United States, often criticized for consumer profligacy, carries household debt of only 71 percent of GDP. The United Kingdom, at 81 percent, is the only other G7 economy in our stratosphere. Our household debt exceeds that of financial crisis-scarred Greece by more than double.

Graphic Credit: Janice Nelson.

Corporations: Overleveraged and exposed

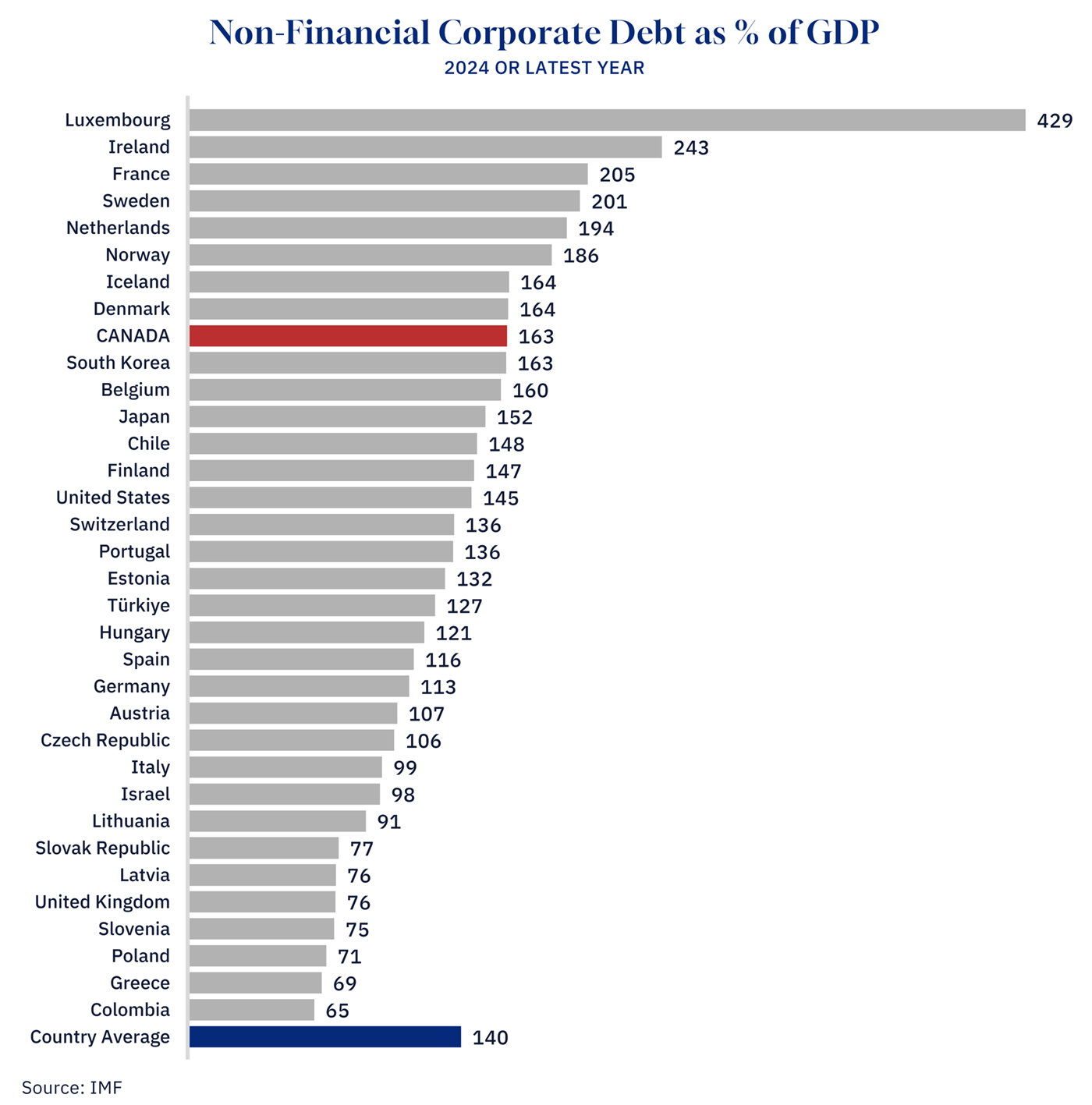

Canada’s non-financial corporations carry debt equal to 163 percent of GDP, placing us in the top tier globally. Only a handful of countries—led by Luxembourg and Ireland—have more heavily indebted corporate sectors. Luxembourg and Ireland are special cases, functioning as financial hubs where multinationals structure cross-border financing through local entities, inflating their debt ratios.

Canada’s corporate debt level exceeds that of the United States (145 percent) and far surpasses Germany (113 percent), despite their significantly larger industrial bases. For a resource-dependent economy like Canada’s, this corporate leverage creates acute vulnerability to commodity price swings and global demand shifts.

Graphic Credit: Janice Nelson.

Government: Squandered fiscal advantage

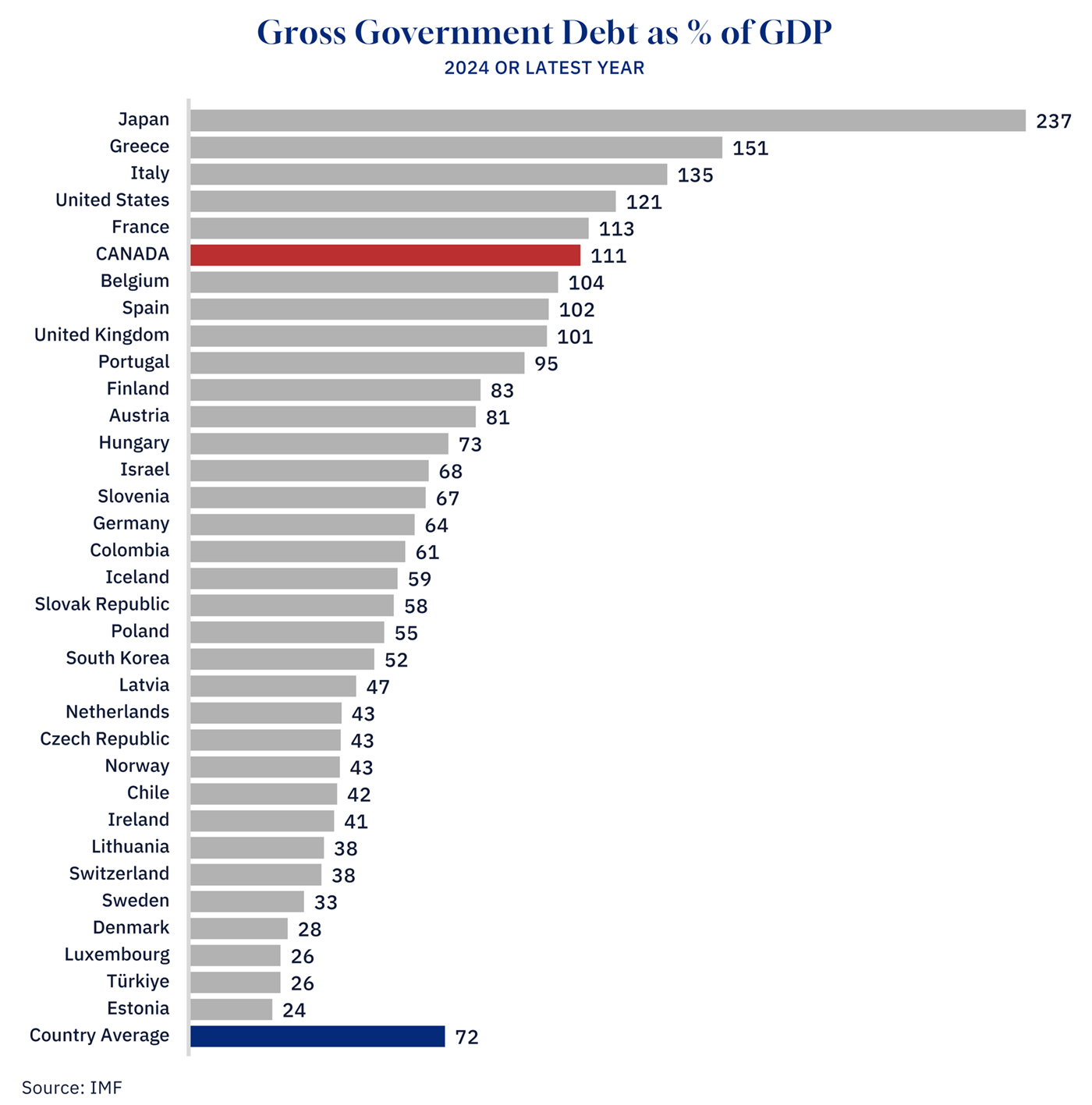

Canadian governments—federal, provincial, and local combined—carry gross debt equal to 111 percent of GDP. Among major advanced economies, only demographically challenged Japan, the United States, France, and crisis-plagued southern European nations like Greece and Italy exceed our government debt burden. We carry more government debt than the United Kingdom (101 percent) and far more than Germany (64 percent). Our level also exceeds the 34-country average of 72 percent.

This represents a dramatic shift. Before the 2008 financial crisis, Canada’s gross government debt stood at just 67 percent of GDP—a fraction of the level today. We’ve squandered much of the fiscal advantage we once held.

Graphic Credit: Janice Nelson.

Why this matters

The instinctive response to debt statistics is often a shrug; if everyone can still make payments, what’s the problem? This misses three critical dynamics that should concern anyone interested in Canada’s economic future.

Fragility trap

High debt levels change how economies respond to shocks. When households, businesses, and governments are all highly leveraged, the entire system becomes fragile in ways that individual balance sheets don’t capture.

Consider what happens when interest rates rise unexpectedly, commodity prices fall, or a recession arrives. Households cut spending to service debt. Businesses postpone investment and hiring. Governments face a tough choice: increase spending to support the economy while their debt servicing costs rise, or impose austerity when citizens need help most.

This isn’t theoretical. During the 2022-2023 interest rate hiking cycle, Canadian mortgage holders faced payment shocks, businesses delayed expansion plans, and government deficits widened. We were fortunate that this cycle didn’t coincide with a recession. Next time, we may not be so lucky.

Misallocation of capital

Canada’s debt levels reveal deeper structural issues about how we allocate capital. When households borrow primarily to bid up the price of existing housing stock, they inflate asset prices without adding productive capacity. When corporations leverage up to acquire existing businesses rather than build new ones, we shuffle ownership without creating value. When governments borrow to fund operating expenses, we consume our future.

The data suggests Canada has been doing exactly this. Our high household debt correlates with housing prices that have dramatically outpaced income growth. Our corporate debt hasn’t translated into the business investment and productivity growth we desperately need. Our recent government debt has largely funded direct program spending growth.

This matters because misallocated capital compounds over time. Every dollar borrowed to inflate housing prices is a dollar not invested in businesses that could drive productivity growth. Every business that levers up for acquisition rather than innovation is a missed opportunity for genuine value creation. Every government dollar spent on current consumption rather than future-oriented investment narrows our options going forward.

Erosion of policy freedom

Canada’s debt burden will constrain our policy options and how we can respond to future challenges. What happens when the next recession or external shock arrives?

Policymakers face difficult trade-offs. A cooling housing market reduces asset values. Tariffs raise costs. Either scenario could trigger defaults and financial instability when leverage is this high. Our debt burden has effectively narrowed the range of feasible approaches.

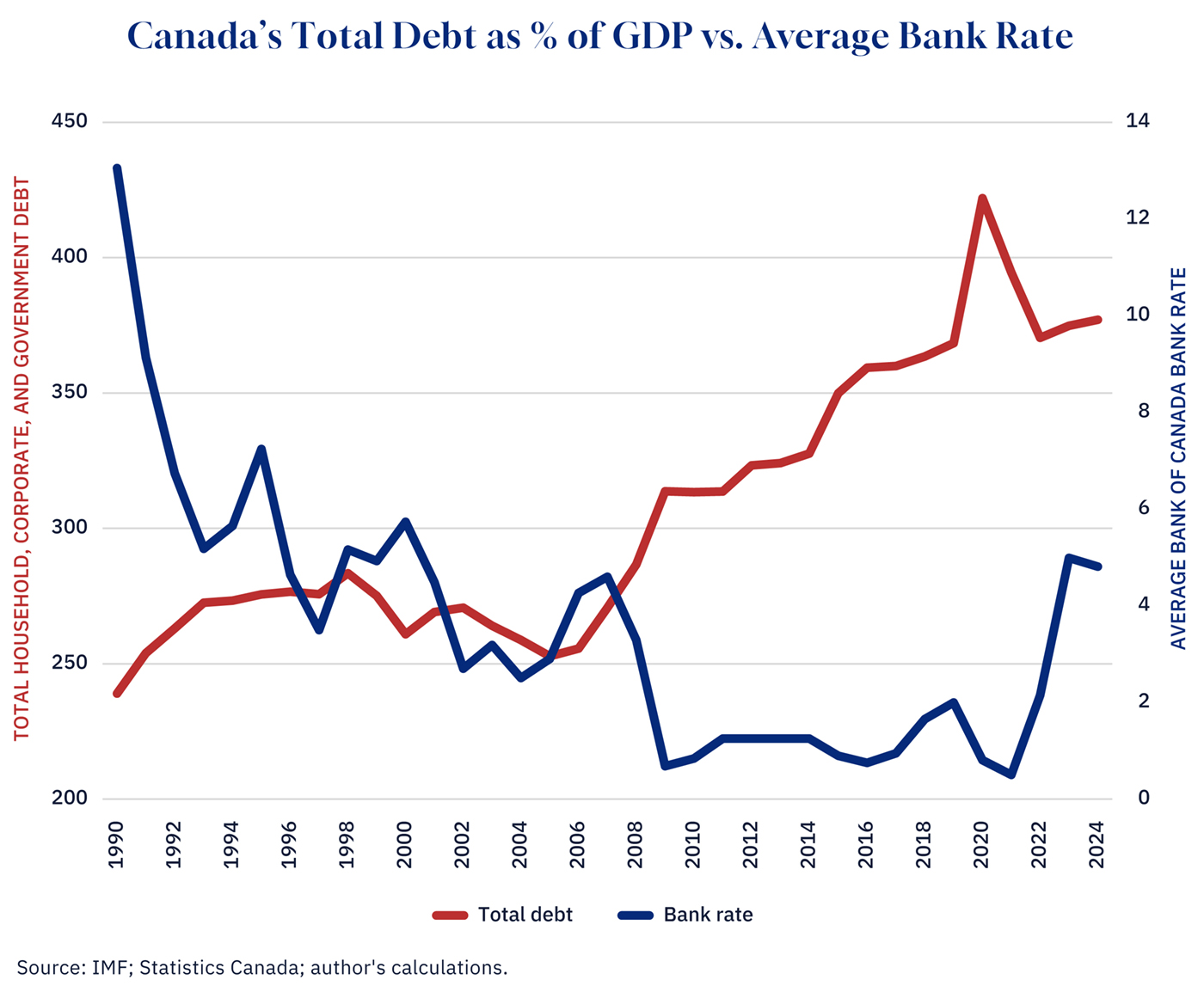

Is the debt run-up a response to low interest rates?

The short answer: yes. Canada’s debt accumulation partly reflects a rational response to falling interest rates. The data seems to support this (noting that correlation is not causation). Total debt as a percentage of GDP shows a strong negative correlation (-0.61) with the Bank of Canada’s average bank rate from 1990 to 2024.The bank rate was used instead of the target/policy rate because a historical time series was readily available from Statistics Canada going back to 1990. The target/policy rate is available for entire years starting in 1993. The bank rate tracks the target/policy rate closely. Total debt took off starting in 2007 as the rate dropped to near zero during the global financial crisis and again during the pandemic. When borrowing becomes cheaper, households, businesses, and governments naturally take on more debt.

Graphic Credit: Janice Nelson.

This rational response creates its own problems. The average bank rate surged from 0.5 percent in 2021 to 5 percent by 2023. Debt accumulated at the lower rate becomes far more burdensome at the higher rate. If Canada’s debt levels primarily reflect cheap credit rather than expanded productive capacity, we’ve built a system dependent on perpetually low rates. That’s a precarious foundation.

What about assets?

That’s a fair question. After all, debt is only one side of the balance sheet. Canadian households hold substantial financial assets, including home equity, retirement savings, and investment portfolios. Corporations own productive capital, intellectual property, and cash reserves. Governments hold physical infrastructure, Crown corporations, and natural resource rights. Focusing solely on debt without considering assets might paint an incomplete picture.

This is true, but this misses what makes debt dangerous. Assets and liabilities aren’t symmetric in a crisis. You can’t pay your mortgage with your house; you need cash flow or liquid assets. When shocks hit, asset values fall while debt remains fixed. Housing wealth evaporates precisely when households need liquidity most, corporate assets lose value when revenues dry up, government assets become harder to monetize when markets freeze. Net wealth positions matter for long-term solvency, but gross debt levels determine fragility, and fragility is what constrains our options when we need them most.

View reader comments (7)

Recognizing reality

Canada’s debt position represents a binding constraint on our economic future that we’ve been reluctant to acknowledge.

For households, this means understanding that housing wealth built on leverage is fundamentally different from wealth created through saving and productive investment. For businesses, it means asking whether debt-financed growth is genuine growth or merely financial engineering. For governments, it means protecting fiscal capacity to respond to future crises—and recognizing that each new affordability measure funded through borrowing further narrows the space available when genuine emergencies arrive.

The GST credit enhancement is case in point: it will help Canadians struggling with costs, but relief and resilience aren’t the same thing. One addresses today’s pressures through consumption; the other requires building productive capacity for tomorrow. Collectively, as a country, we’ve seemingly been making choices that prioritize short-term consumption and asset price appreciation over long-term resilience and productive capacity.

The good news: recognizing a problem is the first step toward addressing it. Canada isn’t Greece facing imminent debt crisis, nor are we Japan, burdened by one of the world’s oldest populations. We still have options. But the window for exercising those options is narrowing with every billion we borrow for consumption rather than investment.

Canada faces a spiraling debt problem, ranking fourth in total indebtedness among OECD countries, with aggregate debt at 377 percent of GDP. This debt is spread across households (103 percent of GDP), corporations (163 percent of GDP), and government (111 percent of GDP). This high leverage makes Canada fragile, prone to misallocating capital towards consumption and asset appreciation rather than productive investment, and erodes policy freedom. While partly a response to low interest rates, the reliance on cheap credit creates a precarious foundation, limiting future crisis response capabilities.

Is Canada's high debt level a direct result of low interest rates, or are there other contributing factors?

How does Canada's high aggregate debt impact its ability to respond to future economic crises?

What does the article mean by 'misallocation of capital' and how does it relate to Canada's debt?

Comments (7)

This mess in which we find ourselves reveals less about debt than the lack of real GDP growth. For the past decade and more Canada’s inflation adjusted annual growth rate has been ostensibly zero and interest rates were lowered to historic levels thereby incentivizing borrowing and penalizing savings. This is an extremely dangerous combination. Couple that with a federal government led by individuals completely bereft of the knowledge of or inclination to stimulate private sector growth and job creation and the numerator of the debt to GDP equation outpaces the denominator (simple math probably no longer taught). Our problem is debt growth for sure but the bigger problem is a country run by a government ignorant of and hostile toward the private sector needed to generate real GDP growth.