DeepDives is a bi-weekly essay series exploring key issues related to the economy. The goal is to provide Hub readers with original analysis of the economic trends and ideas that are shaping this high-stakes moment for Canadian productivity, prosperity, and economic well-being. It features the writing of leading academics, area experts, and policy practitioners. The DeepDives series is made possible thanks to the ongoing support of the Centre for Civic Engagement.

Pierre Poilievre’s recent Toronto speech revealed a surprising area of common ground with Prime Minister Mark Carney on responding to Donald Trump’s tariffs and geopolitical uncertainty: Canada must focus on what it can control.

The same day Poilievre delivered his speech, Dominic LeBlanc, the federal Liberal minister responsible for freeing internal trade, was across town making a similar point, where he bemoaned “the bureaucratic system that gets heavier and heavier” and stands in the way of economic growth.

Regulatory reform is one area of domestic control where both parties acknowledge there’s a problem. Canada’s regulatory burden hurts productivity, deters investment, inflates prices, and protects incumbents—and it does all of this independently of anything Trump does. We have built a “red tape state” that compounds costs and drives capital away.

This burden has accumulated over decades, across governments of all stripes, and now touches nearly every corner of the economy. The scale of the problem is best illustrated by the Carney government’s own actions. In a remarkable break from its predecessor, it has reversed several Trudeau-era regulatory policies, scrapping mandates, repealing environmental rules, and cancelling levies. When a Liberal government governs on deregulation, the diagnosis writes itself.

Red tape reform is an underused antidote to Canada’s sputtering economy. It’s a low-cost, high-impact policy tool. This DeepDive examines how Canada built a red tape state that inhibits its own growth and what it would take to change it.

Not all regulations are equal

Some regulation serves legitimate purposes like protecting consumers from fraud, setting environmental standards that the market wouldn’t voluntarily adopt, ensuring food and drug safety, and maintaining financial system stability. The problem isn’t this regulation; it’s the accumulation of unnecessary, duplicative, and disproportionate rules. It’s the regulations that impose costs exceeding any plausible benefit, that exist primarily to protect incumbents from competition, or that have outlived whatever purpose they once served, causing immense compliance burdens and economic dislocation. These are the “silent killers” of competitiveness.

That distinction matters because critics often blur the two, claiming that any effort to streamline rules will undermine public safety. Experience in reformed jurisdictions—British Columbia, the U.K., Australia, and New Zealand—shows otherwise. When governments pare back unnecessary requirements and focus on what truly matters, both businesses and the public benefit. And regulators can devote more attention to the rules that genuinely protect people.

Another important distinction: a count of regulatory requirements can be a useful proxy, but it can mislead when the burden is disproportionate to the number. Regulations are not equal in their reach or their cost. A single rule requiring that front-of-package nutrition symbols appear on food products imposes one-time compliance costs on a defined group of manufacturers—costs that multiply every time the requirement is revised, exempted, or reversed. A rule determining who may enter the wireless telecommunications market shapes the monthly bills of millions of Canadians indefinitely. Both count as one regulation. The policy consequences are incomparable.

This is why volume tallies, while important, need to be read alongside whether regulations carry outsized economic weight, and are those the ones drawing the most scrutiny? The regulations that levy the largest costs—supply management tariffs that inflate every grocery bill, foreign ownership restrictions that keep wireless prices high, zoning rules and permitting regimes that prevent supply and inflate development costs and home prices—are far more durable. The beneficiaries tend to be concentrated and organized, while the costs are dispersed across millions of households.

The accumulation of rules

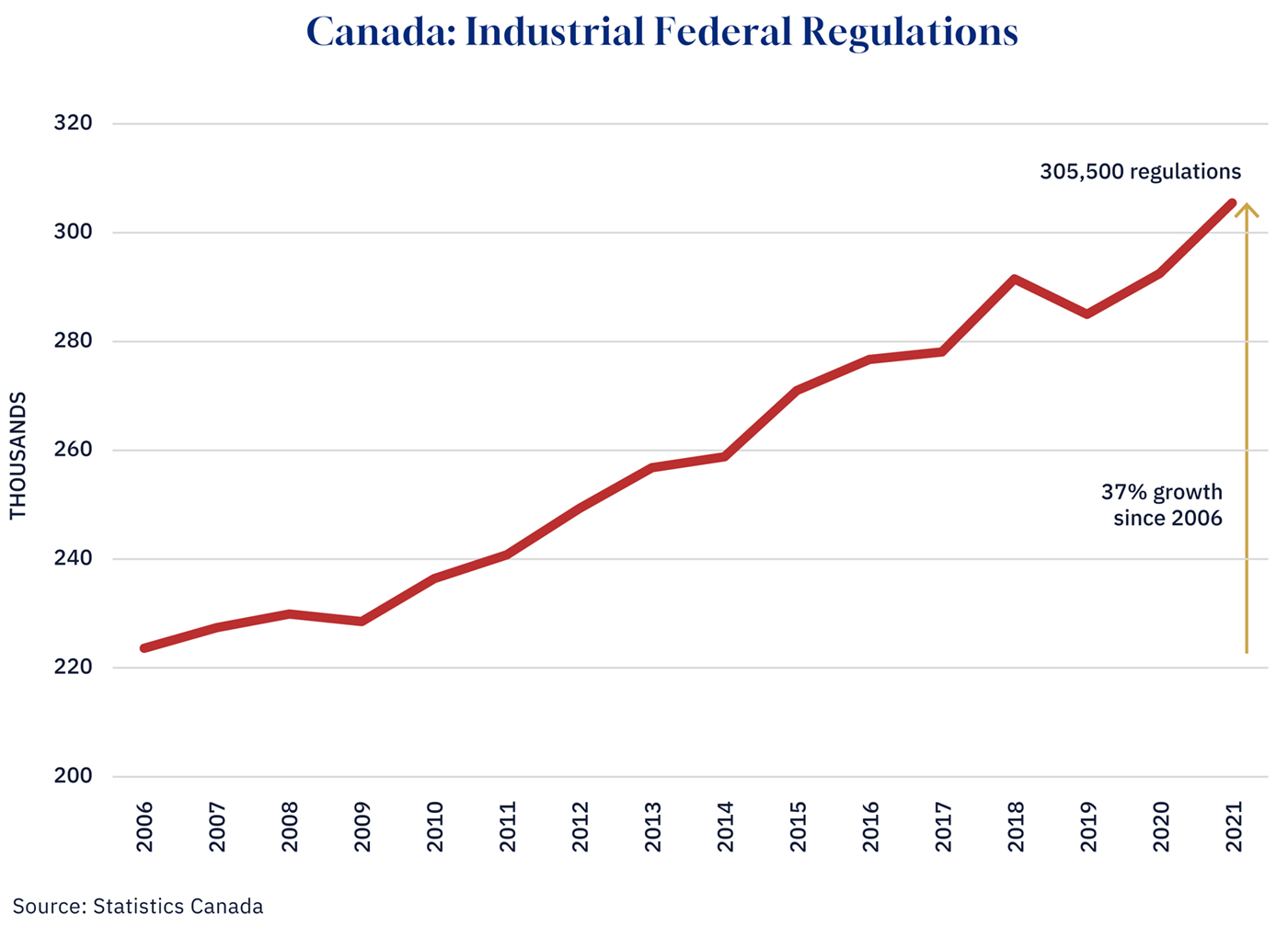

The sheer volume of regulation has nonetheless become a problem. Statistics Canada documented a 37 percent rise in federal regulatory restrictions between 2006 and 2021. This surge was directly associated with a 1.7 percentage point decline in GDP growth, alongside drops in business investment, productivity, employment, and the rate of new business formation.

Graphic credit: Janice Nelson.

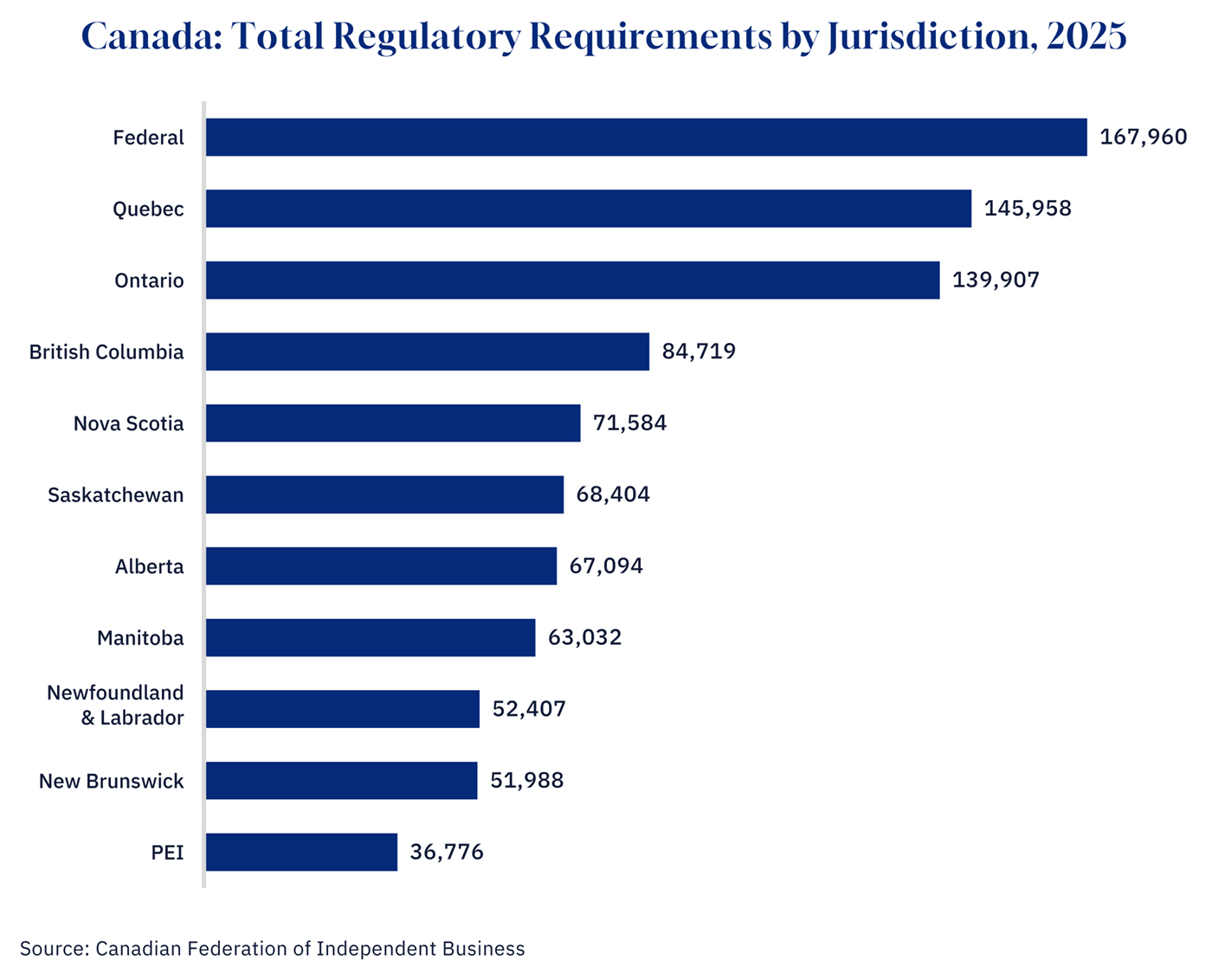

And that’s just federal. Ontario alone, according to a CFIB analysis, carries approximately 140,000 regulatory requirements, using a different methodology. Quebec is the province with the highest, at nearly 146,000.

Graphic credit: Janice Nelson.

The cumulative burden is significant. The CFIB’s latest estimate puts the total regulatory cost for small businesses across all government levels at $51.5 billion in 2024—a 13.5 percent jump from 2020. Of that total, $17.9 billion represents pure “red tape” attributable to unnecessary or duplicative compliance.

Businesses are burning through 768 million hours annually on regulatory paperwork, the equivalent of roughly 394,000 full-time jobs. For the average business owner, that means losing 32 working days a year to red tape alone. Small firms with fewer than five employees are hit hardest, paying over $10,200 per employee in annual compliance costs, a burden that large corporations with dedicated legal departments absorb far more easily. This disparity is precisely why large incumbents are often indifferent to a heavy regulatory environment.

Paying twice and the hidden tax of tax compliance

And then there’s the cost of simply figuring out what you owe. Canada’s tax system is complicated by any standard.

The Income Tax Act has grown almost beyond comprehension. What occupied less than 10 pages when Parliament first enacted it in 1917 now runs to nearly 3,200 in its current consolidated form, and that is without adjusting for font, page, and margin size. The regulatory footprint has expanded in step: the Department of Finance administers 2,054 tax-related regulatory requirements; the CRA administers a further 1,824.

The accumulating complexity diverts billions from productive activity while discouraging investment and risk-taking. Personal income tax compliance alone is estimated at $4.2 billion in 2022, a cost separate from the taxes themselves. These are not productive expenditures. They require time and energy to navigate the system rather than creating value within it. These costs hurt lower-income Canadians and small businesses disproportionately, as they often don’t have the resources or knowledge to navigate the system. Ottawa’s move toward auto-filing for simple returns is a welcome step, but it leaves the larger compliance burden entirely untouched.

View reader comments (10)

Add to this a CRA that has grown in size and assertiveness while becoming less reliable to deal with. Frequent changes to tax rules, inconsistent interpretations, and a growing volume of audit activity have created an environment where the rules of the game feel unclear, even to those trying to follow them. For business owners and investors, this changes behaviour, delaying decisions and pushing capital to jurisdictions where the rules are stable and the tax authority is not a source of operational risk.

An oligopolistic economy by design

Canada’s concentrated industries—telecom, banking, air travel, dairy, eggs, and poultry—share a common feature: their market structure is engineered through government regulatory policy. According to one estimate, over 20 percent of Canadian economic activity is shielded from competition as a matter of deliberate policy choice. The OECD has repeatedly noted that restrictions on services trade remain high in network sectors, hindering dynamism and innovation.

Foreign ownership restrictions written into the Telecommunications Act and Broadcasting Act have blocked the entry of foreign capital that might challenge Bell, Rogers, and Telus—a trio that controls 87 percent of wireless subscribers. The average Canadian telecom bill is nearly $70 per month as of 2023, compared to roughly $44 in Australia—a country of comparable geography and population density.

Banking’s Big Five, protected by the Bank Act’s ownership caps and the high capital requirements of entry, impose an estimated $8.5 billion in excess annual fees (roughly $250 per adult) compared to more competitive markets like the United Kingdom.

Air travel follows the same pattern. The Canada Transportation Act restricts domestic routes to Canadian-majority-owned carriers and prohibits foreign airlines from competing on flights between Canadian cities, a practice known as cabotage. Foreign ownership was capped at 25 percent until 2018; it now sits at 49 percent, but cabotage remains untouched. The Competition Bureau has called for reform, finding that the status quo results in fewer choices and higher prices for Canadians. Air Canada and WestJet dominate a market that policy built for them.

Supply management in dairy, eggs, and poultry enforces over-quota tariffs of 200 to 300 percent, costing Canadian households an estimated $500 per year in dairy prices. This burden falls hardest on low-income families. As one professor put it: “On one hand, [elected officials] talk about food affordability, and on the other hand, they have a government-sanctioned cartel in staple foods.” In early 2025, Canada imposed a 245 percent tariff on British cheese, a move that helped derail trade talks with the U.K. These are taxes governments impose on Canadians to protect a domestic industry at the expense of domestic consumers.

Regulations impacting everyday life

Canadians encounter the cost of bad regulation at the grocery store, on their utility bills, and most acutely when they buy a home.

Canada’s own import barriers impose a tax on everyday essentials. Agricultural imports face an average tariff of nearly 15 percent, dairy imports over 243 percent, and imported clothing 16.5 percent. Trevor Tombe has calculated that these self-imposed levies cost the average Canadian family around $230 annually, and for one in 10 families, more than $500.

Canada is now the food inflation capital of the G7. Grocery prices rose 6.2 percent last year—double the U.S. rate, triple that of France and Germany. This is despite the U.S. pursuing far more aggressive tariffs on imported goods. Sylvain Charlebois, a food policy expert, identifies one of the causes as a complex and costly regulatory environment: labelling requirements, administrative compliance burdens, interprovincial trade barriers, and layers of taxation embedded throughout the supply chain. Each factor, taken alone, might appear marginal. Collectively, they “systematically increase the cost of doing business in Canada—and those costs inevitably flow through to consumers.”

Canada’s bilingual labelling rules demonstrate how regulatory compliance costs accumulate invisibly. Under the Consumer Packaging and Labelling Act, virtually every consumer prepackaged product sold in Canada must display mandatory information—product name, net quantity, nutritional information, ingredients—in both English and French, with equal prominence. Quebec adds more layers of French priority. For a domestic small business expanding within Canada, or for a foreign producer entering Canada, this means Canada-specific packaging: separate print runs, translation costs, and label redesigns, requiring layout changes across entire product lines. If international producers don’t bother, that means fewer products on Canadian shelves, less competition, and higher prices.

Then there is housing, one of Canada’s most visible affordability challenges and one where government-imposed costs are enormous, setting aside the demand-side pressures from immigration entirely. In Ontario, government charges account for 31 percent of new home prices. Development charges—fees municipalities levy on new construction, ostensibly to pay for infrastructure—have become a vehicle for cost-shifting on a remarkable scale. In Toronto, development charges on a single-detached home rose 993 percent from $12,910 in 2010 to $141,139 in 2024. Development charges now add more than $195,000 to the average new home price in Toronto.

Prime Minister Mark Carney tours a housing development in Ottawa on Thursday, Nov. 6, 2025. Spencer Colby/The Canadian Press.

These costs do not appear on the purchase agreement but are buried in the price, invisible to the buyer. One study found that government fees, taxes, and charges on new GTA housing are three times higher than in San Francisco, Miami, Boston, New York City, Chicago, and Houston.

The hidden charges on new homes are only part of the story. Canada’s zoning regime actively prevents homes from being built at all. In Toronto, developers face an average 25-month wait for municipal planning approval, compared to 3.4 months in Edmonton and 4.2 months in Calgary. Much of the country’s urban residential land remains exclusively zoned for single-detached homes, making the “missing middle”—fourplexes, triplexes, townhomes—illegal across huge swaths of the cities where housing demand is greatest. When residents can trigger public hearings and appeal zoning amendments, adding months or years to approval timelines, the regulatory system is biased toward existing homeowners and inaction. Canada is in a housing crisis partly of its own regulatory making.

Single-use plastic regulation for checkout bags, cutlery, and straws illustrates how regulatory proliferation creates compliance challenges. Federal, provincial, and municipal governments have each enacted their own plastic bans and restrictions, often with overlapping scope and inconsistent rules.

A grocery chain operating across Alberta was permitted to provide plastic checkout bags in most of the province, but not in the municipalities of Fort McMurray, Devon, or Wetaskiwin. A business operating nationally must navigate the federal Single-use Plastics Prohibition Regulations, plus each province’s own regime, plus any local by-laws that go further still. British Columbia bans compostable plastic bags as of July 2024. Vancouver has a separate fee structure for paper bags. Montreal bans eight specific items.

Although the federal regulations were struck down by a Federal Court in 2023, the Federal Court of Appeal overturned that decision in early 2026, reinstating the federal regulatory framework. Despite this legal clarity, businesses must still navigate conflicting provincial and local rules.

There may be a legitimate case for reducing plastic waste. But the regulatory logic is questionable: lifecycle research finds that plastic alternatives such as paper bags typically generate higher greenhouse gas emissions than the products they replace, and research from comparable jurisdictions finds that roughly 30 percent of plastic reduction was offset by consumers switching to heavier unregulated alternatives.

Other everyday examples accumulate quickly. Provincial liquor boards mark up alcohol by 50 to 100 percent through monopoly retail before the product reaches a consumer. Interprovincial alcohol shipment restrictions long made it illegal to carry a case of wine across a provincial border, and while bilateral deals are now emerging, liberalization remains piecemeal. Vehicle safety inspection requirements vary by province and, in some jurisdictions, impose significant costs on car owners with no clear evidence of improved road safety outcomes. CRTC CanCon levies are embedded in every cable and streaming bill. In each case, the regulation has defenders and a rationale.

This is what a comprehensively regulated economy looks like. A surcharge here, a compliance requirement there, a fee that gets buried in the price of a home, grocery bill, or phone plan. Collectively, they amount to a system that extracts steadily from every Canadian household, yet the question of whether the cost is proportionate to the benefit rarely gets asked.

Projects blocked by development regulations

Regulatory uncertainty slows and sometimes kills investment entirely. The Impact Assessment Act—derided by critics as the “No More Pipelines Act”—was partly struck down by the Supreme Court of Canada in October 2023 as an unconstitutional intrusion into provincial jurisdiction. The uncertainty shelved projects for years while the constitutional question wound through the courts. Capital is mobile; investors who cannot get a clear answer simply go elsewhere.

The average lead time for mining projects has nearly tripled over the past three decades. Projects that became operational between 2020 and 2024 took an average of 17.8 years from discovery to production, compared to roughly six years for mines that opened in the 1990s. This compares to seven years in Australia. General construction permits took nearly 250 days in Canada (as of 2020)—approximately three times longer than in the U.S. and among the longest in the developed world. Every project that never gets built is a prosperity boost that never materializes.

The Carney government’s Major Projects Office promises to reduce federal timelines to two years for projects of “national interest” through a “one project, one process, one decision” model. Ontario has moved in the same direction. But federally, designation requires Cabinet referral through an opaque process without published criteria. Carney himself cautioned that referral “does not mean the project is approved.” Smaller projects, independent operators, and anything outside the political spotlight get no such guarantee. Selective acceleration is Cabinet discretion dressed up as reform.

The same logic applies to the government’s proposed regulatory sandbox provisions in Bill C-15, which would give ministers the power to exempt specific companies from non-criminal federal laws in the name of innovation and competitiveness. The idea has merit in principle; testing regulatory alternatives before committing to them is sensible. But selective exemptions for named parties, chosen by Cabinet without structural reform to the underlying rules, is a pattern Canada should be moving away from, not enshrining in legislation.

A patchwork of professional licensing

Less visible than grocery prices are Canada’s provincial professional licensing regimes. Each province maintains its own regulatory bodies. Ontario alone has roughly 40, covering more than 100 professions and trades. The result is several hundred self-regulatory organizations nationwide, each holding a state-conferred monopoly over who may practice and on what terms.

While often well-intentioned, the economic cost can be significant. Qualified professionals licensed in one province routinely face months of additional requirements before they can work in another. Internationally trained professionals can encounter duplicative testing, Canadian experience requirements (although this is changing), and re-qualification processes that sideline skills Canada urgently needs. Progress toward mutual recognition is underway but remains incomplete. The system fragments the labour market, leaving qualified people idle and employers underserved.

Financial regulation and fragmented capital markets

Capital markets show similar fragmentation. Canada has 13 separate provincial and territorial securities regulators, each with its own legislation, rules, and compliance requirements. Ontario—home to the TSX and the country’s largest capital market—does not fully participate in the CSA passport system, meaning firms seeking national reach must satisfy Ontario’s requirements separately from every other jurisdiction. The U.S. has one SEC. The U.K.has one FCA. Australia has one ASIC. Canada has 13.

The financial sector offers another variant of the same issues favouring incumbents. Banking is among Canada’s most heavily regulated industries. A single bank answers to OSFI for prudential oversight, the Department of Finance for legislative compliance, the Financial Consumer Agency of Canada for consumer protection, CDIC for deposit insurance, FINTRAC for anti-money laundering—and in some cases provincial overseers and securities regulators.

Foreign ownership restrictions limit competition, the Bank Act constrains new entrants, and OSFI’s prudential rules, while serving legitimate stability purposes, have the secondary effect of protecting incumbents. In January 2026, the Competition Bureau launched a market study into SME financing, examining how banking concentration raises borrowing costs for small businesses, a gap wider between large firms in Canada than in most OECD countries.

OSFI has signalled awareness of the entry problem. A targeted fast-track approvals framework launching in June 2026 will offer credit unions and fintech entrants a faster, more predictable path to federal licensing. It is a welcome step, but it applies only to two categories of new entrants and explicitly leaves everyone else on the existing process.

The pattern of belated, incremental reform extends to open banking: after many years, Canada is finally targeting a consumer-driven banking framework in 2026—years after the U.K. and Australia—with full payment functionality not expected until mid-2027.

The Bank of Nova Scotia, Scotiabank, signage is pictured in the financial district in Toronto, Friday, Sept. 8, 2023. Andrew Lahodynskyj/The Canadian Press.

Environmental regulation on top of environmental taxes

The environmental regulatory file is where the Trudeau-era’s regulatory accumulation was particularly pronounced. The government’s layering of command-and-control mandates on top of a market-based carbon price defeated the purpose of that instrument. Prof. Ross McKitrick has spent years making this argument: For a carbon price to be economically coherent, the other regulatory boulders in the road need to come out first.

Instead, the Trudeau government layered an increasing carbon tax on top of an expanding pile of sector-specific mandates: a proposed oil and gas emissions cap, Clean Fuel Regulation, coal phase-out for electricity generation, building energy efficiency standards, natural gas generation performance mandates, Clean Electricity Regulations imposing emissions standards on provincial grids, a regulatory environment that stalled or killed nearly every proposed LNG export facility, motor vehicle fuel economy standards, a fertilizer emissions reduction target, and EV sales mandates. The result was the worst of both worlds: a carbon tax that raised costs and a parallel regulatory regime that independently restricted supply, raised prices, and blocked development.

When Carney described the Trudeau government’s oil and gas emissions cap as providing “marginal value in reducing emissions,” he was implicitly acknowledging that Canada had accumulated so much regulation that the system was working against its own stated goals. He has since scrapped the consumer carbon tax, repealed the EV mandate, suspended the Clean Electricity Regulations, and replaced the hard emissions cap with a carbon capture approach. These are meaningful reversals, but many of the underlying command-and-control regulations that blocked energy investment remain in place.

What the international rankings say

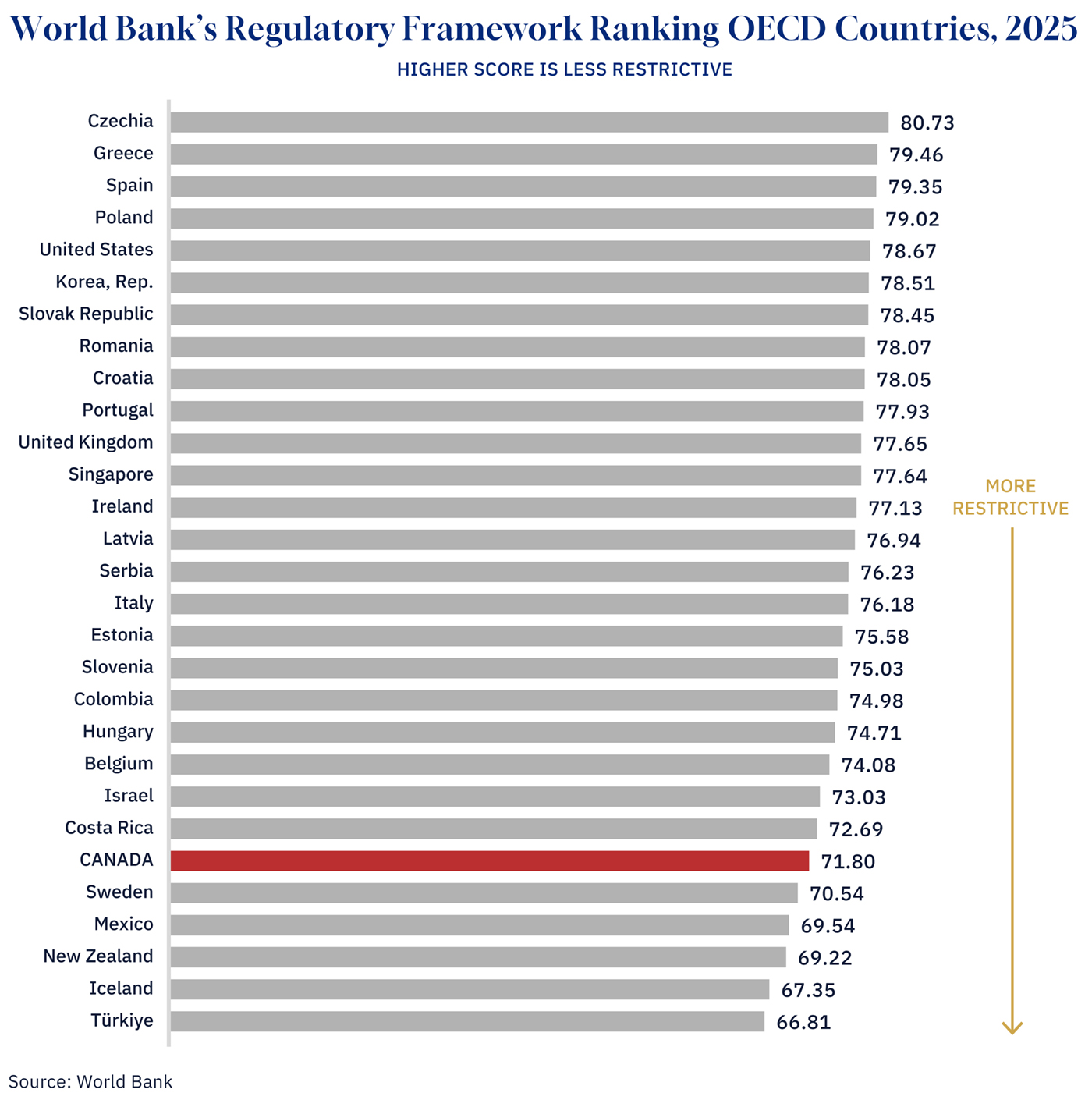

According to the World Bank’s latest Business Ready assessment of 101 countries, Canada’s regulatory performance reveals a troubling gap. On public services and operational efficiency—measuring what government delivers—Canada ranks 8th on both pillars. But on the regulatory framework pillar—measuring the rules businesses must navigate—Canada falls to 33rd, well behind G7 peers in the U.S. (5th) and the U.K. (12th).

The gap is starker among OECD members. On regulation, Canada scores 71.80, placing us 24th among 29 OECD countries, behind not just the U.S. and U.K. but Costa Rica, Israel, Belgium, Hungary, Colombia, and Slovenia. The U.S. sits at 78.67. Canada is closer to the bottom of the OECD than the top.

Graphic credit: Janice Nelson.

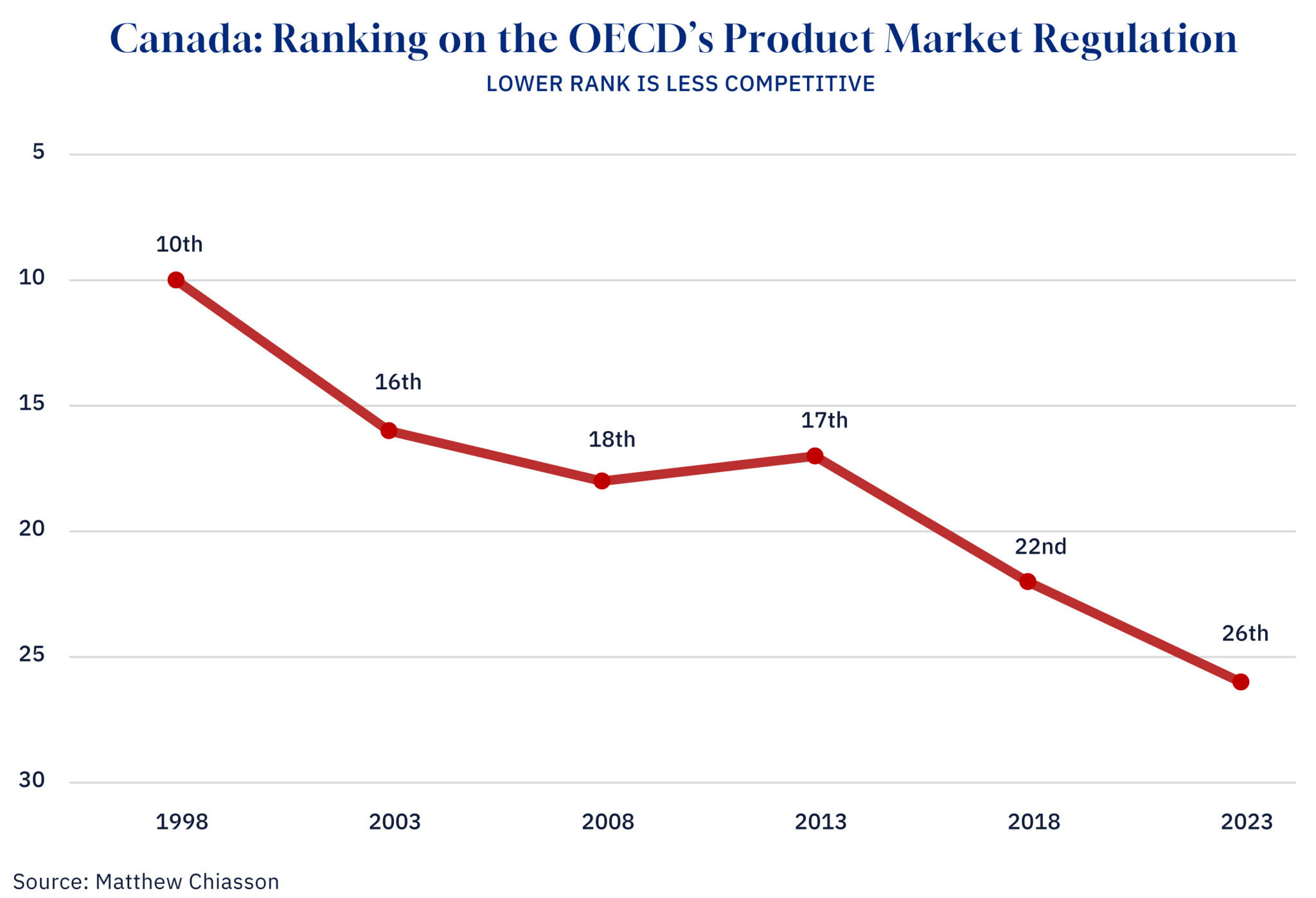

The OECD’s Product Market Regulation indicators measure how conducive a country’s regulatory framework is to investment and productivity-enhancing competition, covering a variety of barriers. Canada’s overall standing has deteriorated from 10th in 1998 to 26th in 2023. Matthew Chiasson points to specific areas where Canada lags: administrative burden (32nd), licensing (36th), foreign investment openness (40th), public procurement (39th), and governance of state-owned enterprises (40th).

Graphic credit: Janice Nelson.

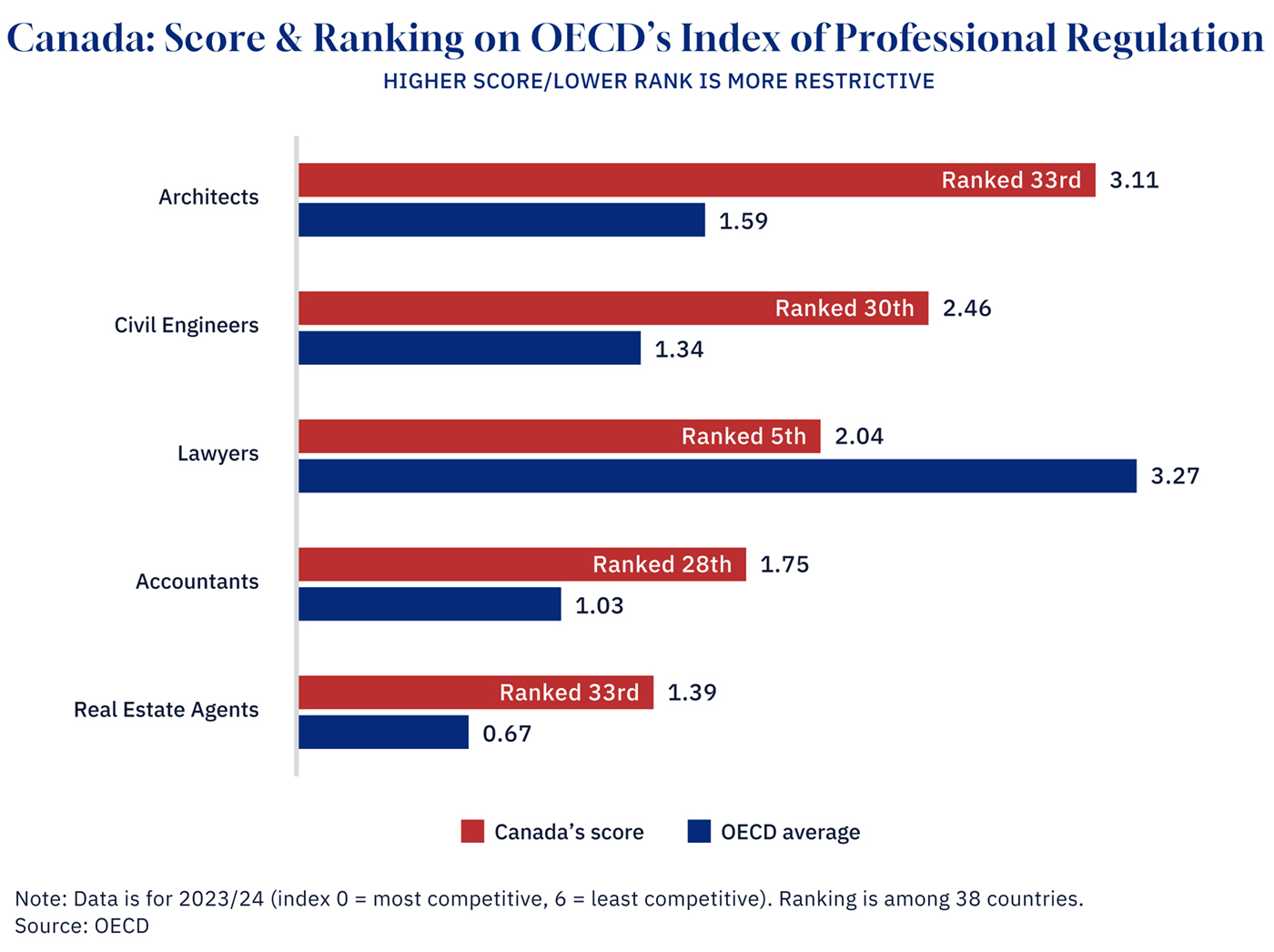

The OECD specifically measures the regulatory competitiveness of certain professions. On a scale from zero (most competitive) to six (least), Canada’s scores for architects, civil engineers, and real estate agents all sit well above OECD averages, ranking in the bottom quarter among 38 countries. These are professions that sit at the heart of Canada’s housing, infrastructure, and construction challenges.

Graphic credit: Janice Nelson.

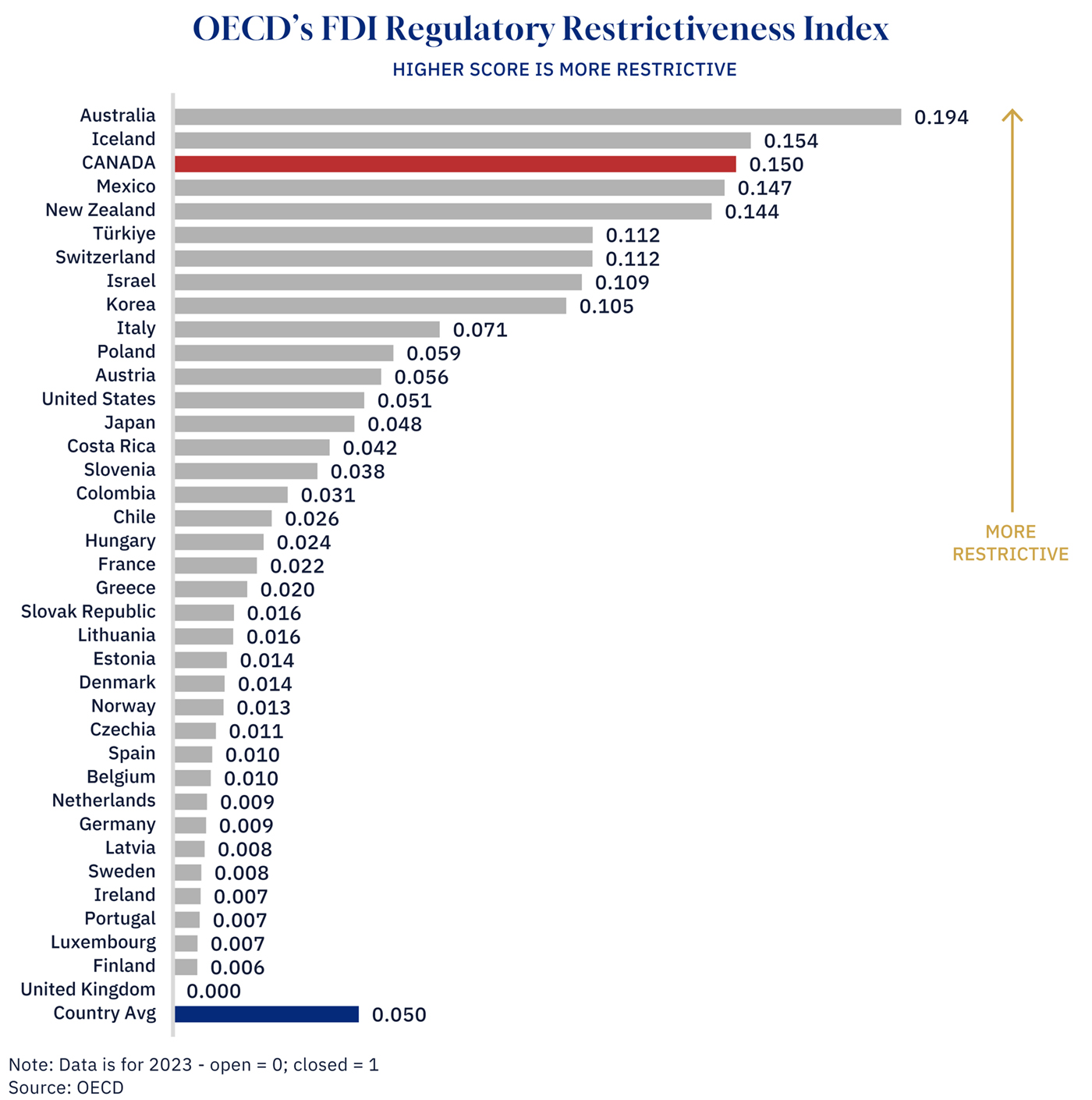

The OECD’s FDI Regulatory Restrictiveness Index measures the extent to which countries limit foreign ownership and control across sectors of their economy, from equity caps and screening mechanisms to operational restrictions on foreign-owned firms. Canada scores 0.150, the highest in the G7 by a wide margin and three times the OECD country average of 0.050. By this measure, Canada is the most hostile country in the G7 to foreign investment. The OECD recently flagged that Canada is moving toward greater restrictions, noting that the Investment Canada Act now signals foreign acquisitions in critical minerals will be approved only in exceptional circumstances, with national security concerns explicitly weighted against incoming capital.

Graphic credit: Janice Nelson.

The full weight of the state

Canada’s regulatory story can’t be told with red tape alone. Philip Cross mapped the full government footprint in a 2014 study. Combining direct public spending (currently 45 percent of GDP), tax expenditures, and the economic value of regulated industries, governments control or heavily direct upward of two-thirds of the Canadian economy. This signals a heavily managed economy with a market sector in the narrow spaces government leaves open.

Crown corporations illustrate the point starkly. Government business enterprises generated $210 billion in revenues in 2024, equivalent to 7 percent of GDP, spanning electricity generation and distribution, alcohol retail across every province, postal delivery, broadcasting, auto insurance, and venture capital finance. There are 47 federal Crown corporations; Ontario alone maintains over 170 provincial agencies. Unlike private competitors, these entities operate with government guarantees, captive markets, and subsidized capital—conditions that crowd out private investment and eliminate the competitive discipline that drives efficiency.

Red tape, Crown corporations, compliance burdens, and government-built moats are expressions of the same underlying disposition toward managed rather than competitive economic life. Together, they explain why Canada’s economic sclerosis runs so deep. That’s why the Bank of Canada has repeatedly extolled the benefits of competition.

Reform is possible

The reform playbook already exists. British Columbia cut over 40 percent of its regulatory requirements starting in 2001 without compromising health, safety, or environmental outcomes—and saw measurable improvements in business investment and economic dynamism. Alberta has sustained regulatory reform through its Red Tape Reduction Act, earning top marks from the CFIB for two consecutive years. Internationally, the OECD’s latest economic outlook dedicated an entire chapter to the regulatory reset imperative, citing New Zealand, the Netherlands, and the U.K. as models of proportionality-based reform that improved both business conditions and regulatory quality.

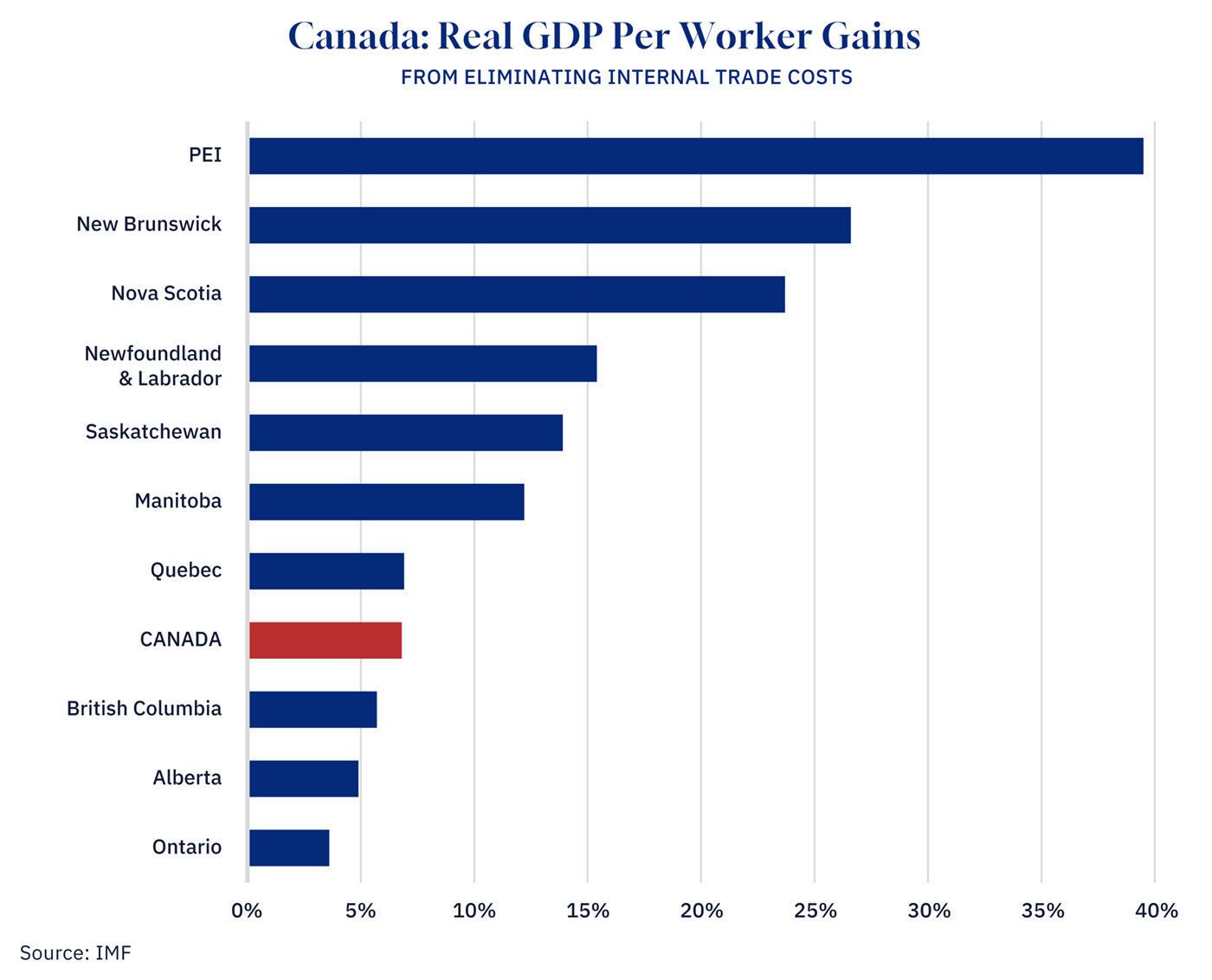

The potential economic gains are large and well-documented. A Competition Bureau-commissioned study analyzing 15 OECD countries over 25 years estimates that aligning Canada’s regulations in energy, transport, retail distribution, and professional services with international best practices could boost GDP by 6.5 to 10 percent over the long run. Meanwhile, the IMF estimates that eliminating internal trade barriers—currently equivalent to a 9.5 percent national tariff—could raise real GDP by roughly 7 percent, or $210 billion in today’s dollars.

Graphic credit: Janice Nelson.

What needs to change

First, a genuine one-for-two rule: for every new regulation introduced, two must be removed, with public reporting against measured targets. The existing one-for-one rule is a floor. Jurisdictions that have improved their regulatory standing have done so through explicit stock reduction, not just flow management.

Second, mandatory sunset reviews on a five-year cycle, with the burden of proof on regulators to demonstrate that existing rules still serve their original purpose at proportionate cost.

Third, universal rather than selective project approval timelines. Every project meeting published criteria should receive binding federal timelines, not just the ones Cabinet has chosen to accelerate. The Major Projects Office is a step, but its discretionary structure means the most politically favoured projects get the fastest approvals.

Fourth, full mutual recognition of goods and professionals across provinces on a fixed timeline. Ontario and select provinces have advanced mutual recognition on goods and services in December 2025, but the system remains fragmented. Canada could look to the Australian model of the 1990s, where subnational governments aligned on competitiveness as a shared priority and channelled federal leadership into binding mutual recognition legislation rather than perpetual intergovernmental process. Canada could also institutionalize an interprovincial barrier reduction commission with a permanent mandate to identify, track, and eliminate remaining barriers. A commission enshrines political will after Trump’s tariff threats subside.

Fifth, a serious review of the most heavily regulated sectors asking whether the original regulatory justifications still hold in 2026. Most of those rationales were formed in the mid-20th century. Technological change has fundamentally altered the economics of natural monopoly, information asymmetry, and cultural protection that once justified these structures.

Push through the open window

Every regulation that imposes costs on the broader economy typically creates concentrated benefits for a specific group. Those groups are organized, funded, and present at the table. The entrepreneurs who never started and the investors who went elsewhere are often less visible.

That asymmetry is why the apparatus keeps growing despite successive promises to cut it back. But the political calculus has shifted. External pressure—tariff threats, capital flight, weak economic performance, and the imperative to drive growth without adding to the debt—has turned red tape into an economic imperative. The Carney government’s reversals and rhetoric, and mutual recognition agreements spreading across provinces, signal that the window is open.

This reform doesn’t cost money. The political cost is real, but so is the constituency for change.

Canada’s excessive regulatory burden, or “red tape state,” is hindering economic growth by hurting productivity, deterring investment, inflating prices, and protecting incumbents. There is a vast accumulation of unnecessary, duplicative, and disproportionate rules across various sectors, including telecom, banking, and housing. Both the current government and opposition acknowledge the problem, with the government reversing some Trudeau-era regulations. Reforms such as a one-for-two rule for regulations, mandatory sunset reviews, universal project approval timelines, and full mutual recognition of goods and professionals across provinces are necessary.

The article highlights 'red tape' as a problem. What specific economic consequences does this 'red tape' have on Canada?

The article mentions potential solutions like a 'one-for-two' rule. What other specific regulatory reforms are proposed, and how might they impact Canadian businesses and consumers?

The article points to concentrated industries like telecom and banking. How do government regulations contribute to this concentration, and what are the potential effects on Canadian consumers?

Comments (10)

Are the costs of the thousands of public service workers employed to administer this regulatory overkill factored into this depressing analysis?