Despite lower prices, Canadian homes are more expensive than ever.

Canada’s housing market is in the middle of a sharp contraction, the scale of which we haven’t seen in decades—potentially ever.

In new data released last week, the Canadian Real Estate Association (the premier source of data on this) found the volume of sales has collapsed to roughly half of its peak during the pandemic.

And our home price bubble may be bursting. But unfortunately for Canadians hoping to buy, even these sharp declines will do little to improve affordability and come with risks for Canada’s economy.

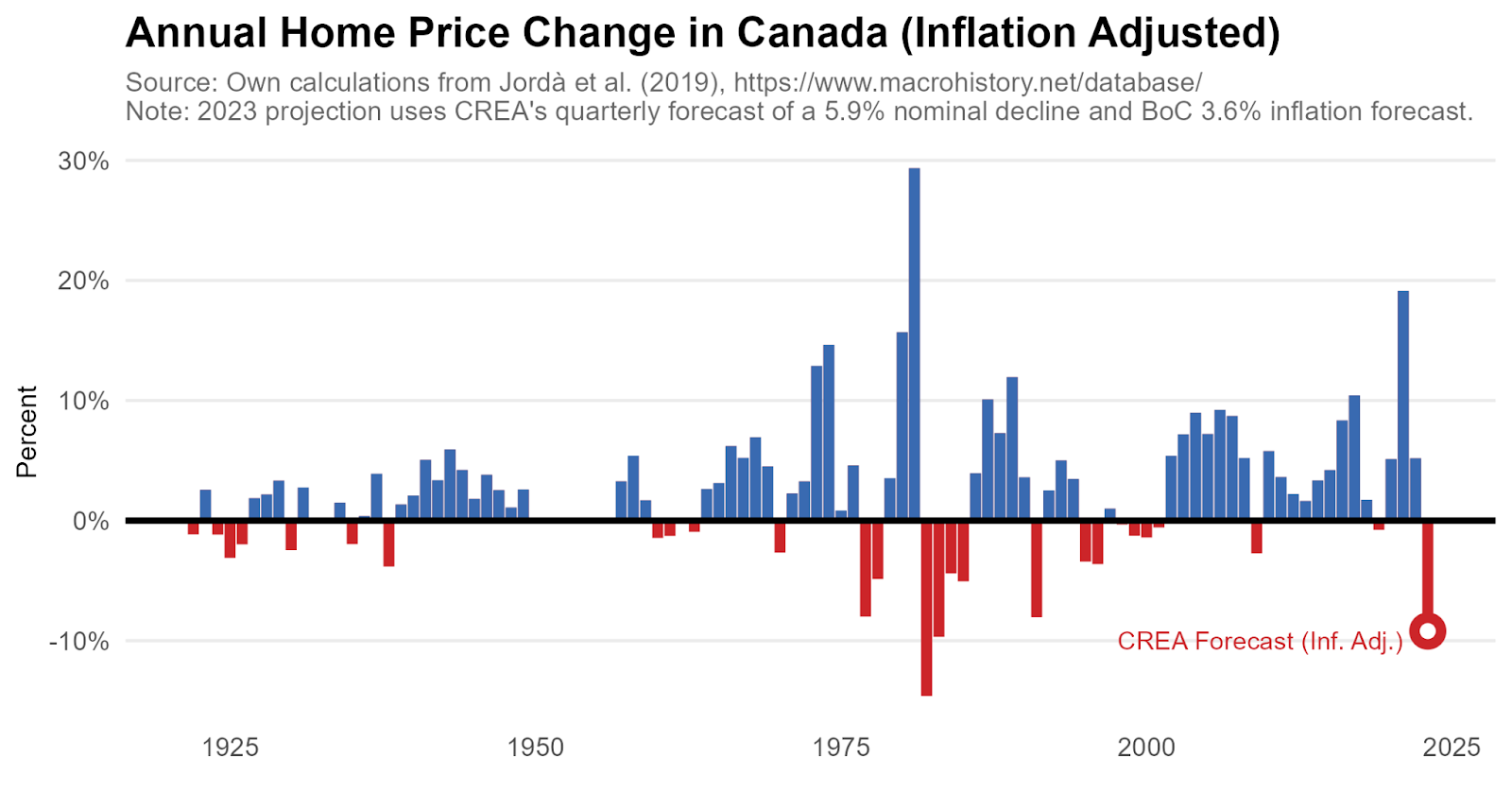

Year-over-year, prices are down nearly 13 percent. And compared to February 2022 (the peak), prices are down over 15 percent. This might be the sharpest decline for Canada on record. For comparison, the pace of home price declines in the United States during the financial crisis peaked in February 2009 at over 12.8 percent.

And some suspect we are only halfway through.

To appreciate the truly historical scale of this development, it is best to look at the annual averages—where we have roughly a century of good data.

CREA’s expectation is for 2023 prices to fall 5.9 percent, on average, compared to 2022. RBC, meanwhile, recently forecast an 8.5 percent reduction. And TD projects a 10.7 percent decline. Even using the lower forecast from CREA, 2023 may be the second-largest reduction in the real value of Canadian homes in history, adjusting for inflation.

Of course, Canada’s housing market—especially in Toronto and Vancouver—grew rapidly during the pandemic to eye-watering levels, to put it mildly. A correction is welcome and healthy.

For prospective home buyers, however, the situation is not improving. Despite prices falling over 15 percent, the monthly mortgage payment required to buy one is actually higher than before. The cause, of course, is rising interest rates

If you put 10 percent down and secured an average rate of nearly 6 percent, you’d face monthly payments of nearly $4,100 to purchase an average home.This is just an average of posted five-year rates. Shop around to different lenders to find better deals. That’s more than the roughly $3,800 per month you’d need to do the same early last year. If you put 20 percent down, monthly payments today would still be over $3,600.

These high payments are far above the roughly $2,300 per month required before the pandemic hit. At today’s rates, home prices would have to fall by more than a further one-third to get back to that level. That would be a roughly 45 percent decline from peak to trough—which would bring prices back to where they were 10 years ago and would represent double the total price decline in the United States observed nationally between 2006 and 2012.

These numbers are just to illustrate the point, and individual circumstances, rates, real estate markets, and so on, will vary. But one thing is clear: with average (pre-tax!) monthly earnings of around $4,800, we remain firmly in historically unaffordable territory.

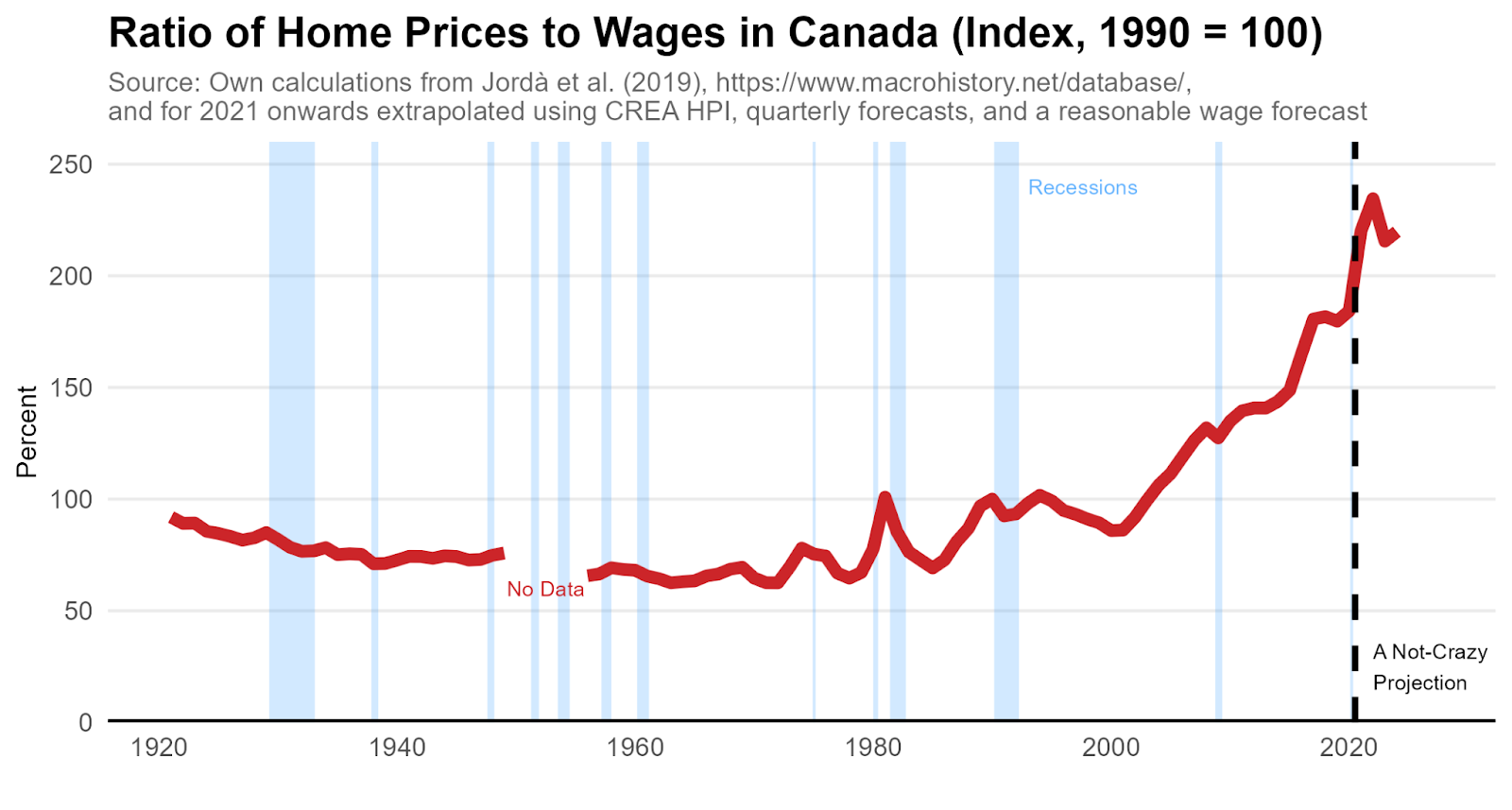

Using data for most of the past century, I find home prices relative to wages in 2022 were triple what they were for most of the period prior to 2000. In 2023, despite the forecasted drop, they may remain roughly 20 percent above the already-high 2019 levels.

Of course, interest rates were significantly higher in previous years, making even lower-priced homes challenging to afford. But I estimate 2023 is on track to see the second-highest ratio of mortgage payments to wages in Canadian history—second only to 1981.This is based on the mortgage payment required to purchase a home of average value at the average posted five-year rate.

To complicate matters further, the rapid pace of decline creates its own set of risks for Canada’s economy.

Consider the situation of any borrower who purchased a home in early 2022 anywhere in the Greater Toronto area. Today, their home could be worth 15 to 20 percent less. If they contributed less than that as a downpayment, they are already underwater: their mortgage is now larger than the value of their home.

Multiply this across many buyers in many cities and combine it with the potential for slowing economic growth, or even outright recession as some fear, and the potential for challenges in Canada’s financial system is obvious. Major banks are already increasing their loan loss provisions in anticipation.

To be absolutely clear, Canada’s financial system is much stronger than the United States’ was going into the financial crisis. The quality of our mortgages is higher since it’s harder to get one and borrowers face various minimum qualifying requirements. And our banks are individually in stronger positions. But there are still risks.

Indeed, our main bank regulator (the superintendent of financial institutions, Peter Routledge) recently noted “systemic vulnerabilities have persisted at elevated levels and, in some cases, have risen materially in recent quarters.” And they have acted. Effective February 1, for example, one of the key financial buffers the Big Six banks are required to hold—known as the Domestic Stability Buffer—was increased for the first time in nearly two years.

I don’t have a solution to offer. Supply-side efforts to increase housing supplies across the country are certainly necessary. But given the historically unprecedented situation we’re in—rapid reductions in home prices combined with worsening affordability—more public policy creativity than our governments tend to deliver is surely required.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School…

Recommended for You

Pierre Poilievre is doing his best to repair Canada–U.S. relations: The Weekly Wrap

Pierre Poilievre tells Joe Rogan he wants to take Canada in a different direction than Carney: As America’s resource partner and ally

‘They are scrambling in real time’: The Roundtable on the spiralling Iran War and Trump’s erratic leadership

Canada has a long, hard road ahead if it wants to meet its lofty investment ambitions