Dramatic headlines about household debt are everywhere: “Canada’s household debt is now highest in the G7,” read one headline. “Households now owe more than Canada’s entire GDP,” read another.

It’s not just the media. The Bank of Canada is increasingly signaling that it is “more concerned than it was last year about the ability of households to service their debt.” And the CMHC’s deputy chief economist recently warned that Canada’s high debt levels make its economy more vulnerable to any global economic crisis.

This all sounds pretty dire.

But do Canadians really have a debt problem?

A deeper look at the data suggests things may not be as gloomy as these headlines suggest. At least, not for most households. Instead, we should focus much more than we do on the very real challenges facing young Canadians and avoid lumping all households together.

Of course, it’s certainly true that household debt is higher than in many other countries. In Canada, households owe an amount equivalent to 107 percent of the economy—behind only Australia among advanced industrial economies, according to the IMF. Just for comparison, consider the U.S., with a household debt representing 78 percent of their GDP. Or the U.K., with their figure sitting at 86 percent. And Germany? A modest 57 percent.

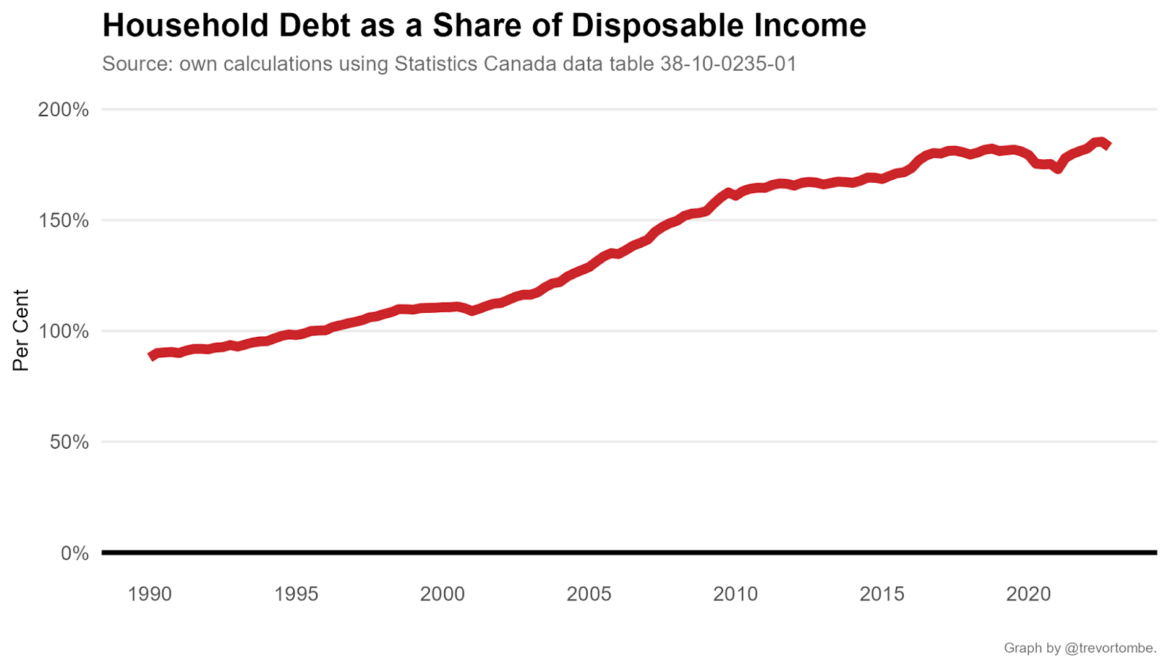

This is not a new development. Canadian household debt has been rising considerably in recent decades. Today, household debt exceeds 182 percent of income—roughly double what it was in the early 1990s.

But these particular statistics tell a misleading story if viewed in isolation.

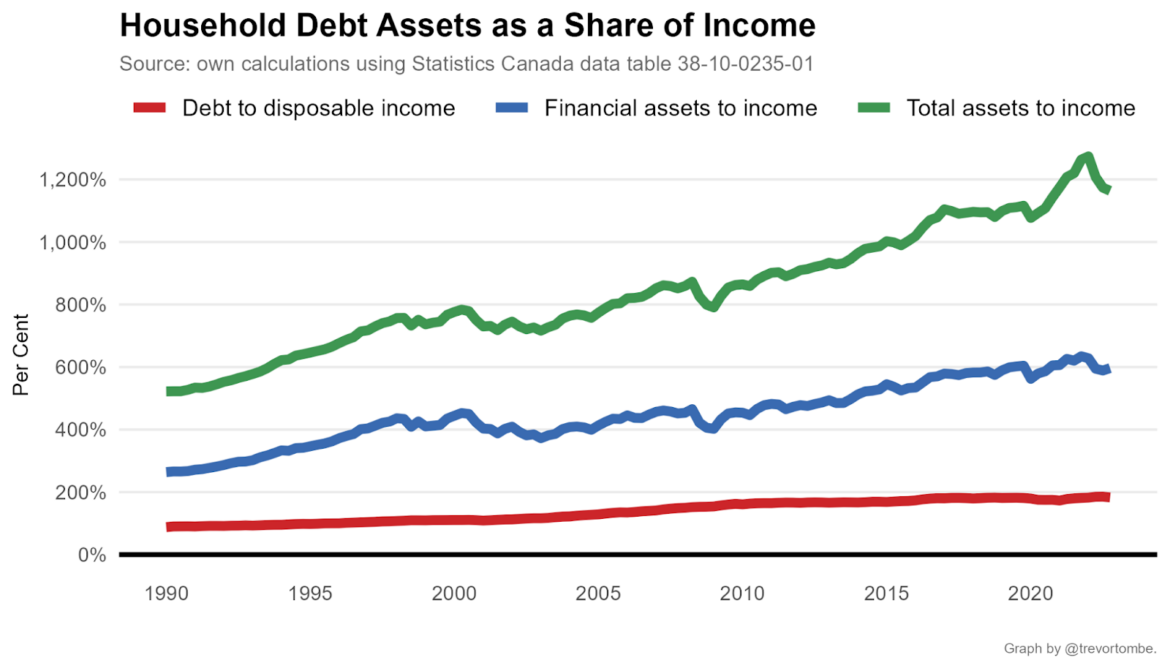

Households have not only been increasing their debt but have also dramatically increased their assets. So while Canadians owe a lot, they also own a lot!

This might even be a better way to think about household debt. Comparing it to GDP or to incomes is to compare stocks (debt) with flows (income or GDP). Better to compare like with like, i.e. debt (a stock) with assets (also a stock). After all, in the event of a crisis leading to job losses and declining incomes, those affected can lean on savings to meet their obligations.

In short, we mustn’t forget the other side of household balance sheets.

And I’m not just talking about the ever-increasing value of real estate that Canadians own. Selling a home is challenging, both financially and sometimes emotionally too. Even if we look at just financial assets, which excludes real estate, you can see Canadian households on the whole are doing well. Financial assets are 600 percent of income—more than triple the total debt—and over 330 percent of GDP.

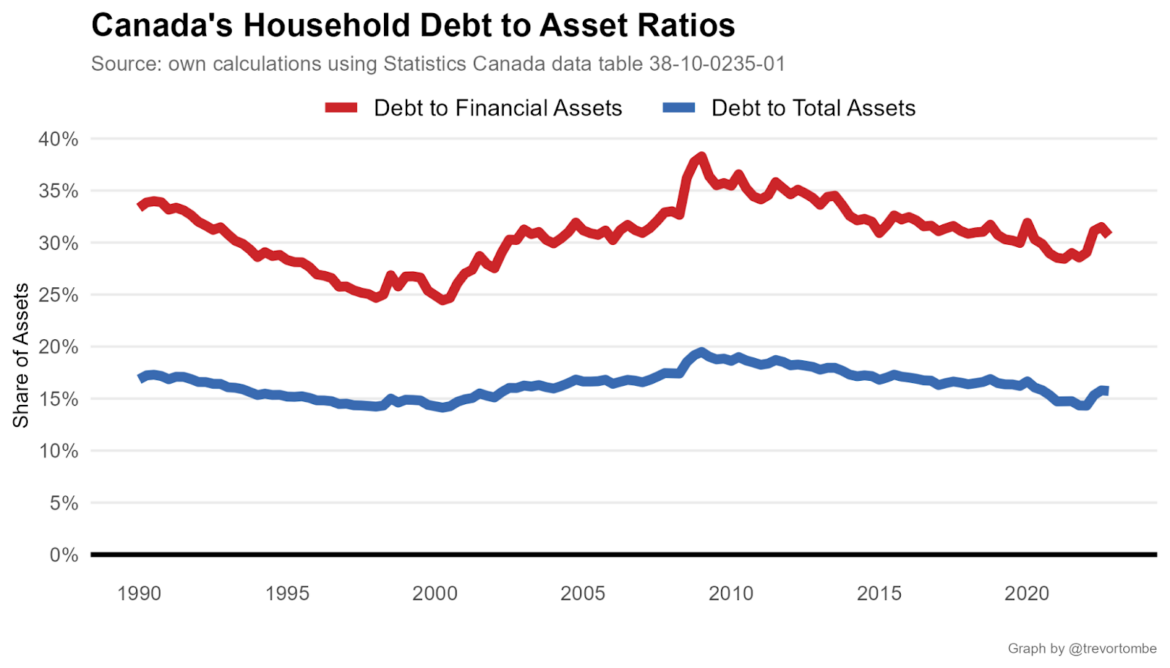

So by comparing total debt as a share of assets, we get a very different story. Instead of an intimidating upward climb, the chart below presents a steadier landscape. Debt as a share of assets remained within a range of about 15 to 20 percent for most of the past thirty years. Today, it’s actually on the relatively low end of things historically. Relative to financial assets only, household debt is barely over 30 percent—also in line with historical norms.

Let me be clear, though: this is not to suggest that all Canadians are having an easy time with debt during a time of rapidly rising interest rates. The cost of servicing debt has risen from just under 6 percent of income at the end of 2021 to nearly 8 percent at the end of 2022. That’s a sharp change and an interest burden not seen since 2009. Mortgage interest payments also reached 4.5 percent of household income at the end of 2022, the highest since early 2000.

But these rising burdens are not evenly felt. The situation facing young families and new home buyers is particularly acute.

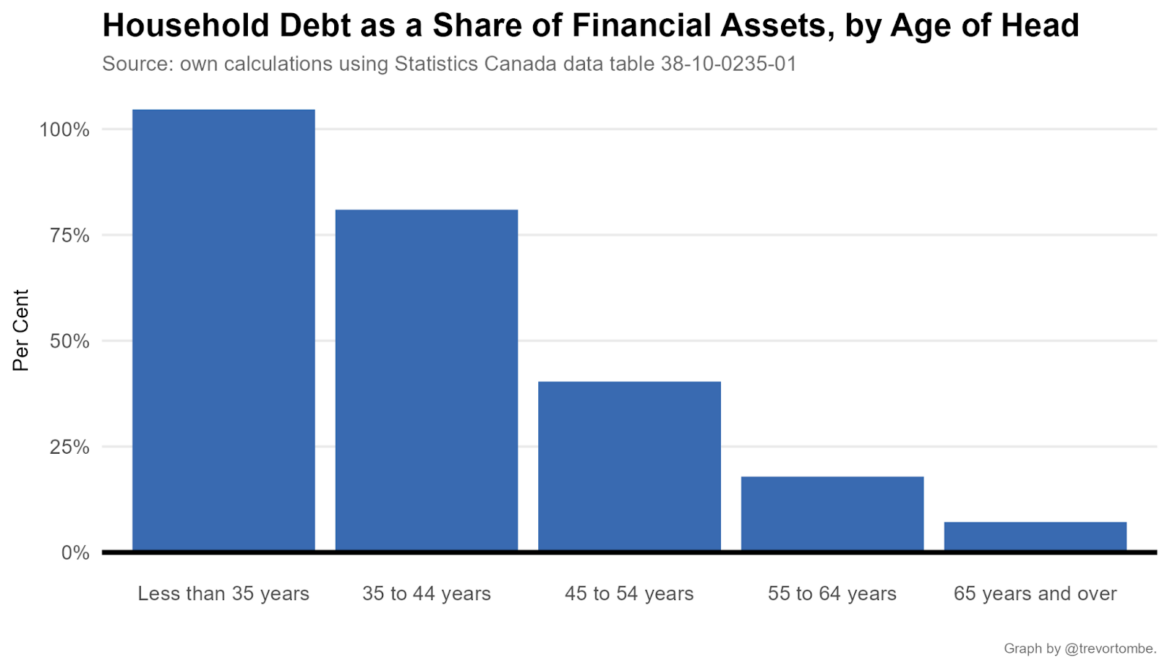

Consider younger families that have not yet built up a substantial cushion of liquid savings and must take out considerable debt to access unaffordable housing in many cities. By the end of 2022, households led by those under 35 found their debt burdens outweighing their financial assets. In households headed by someone aged 35 to 44, debt amounted to 80 percent of their financial assets on average. Debt burdens decline sharply for older households.

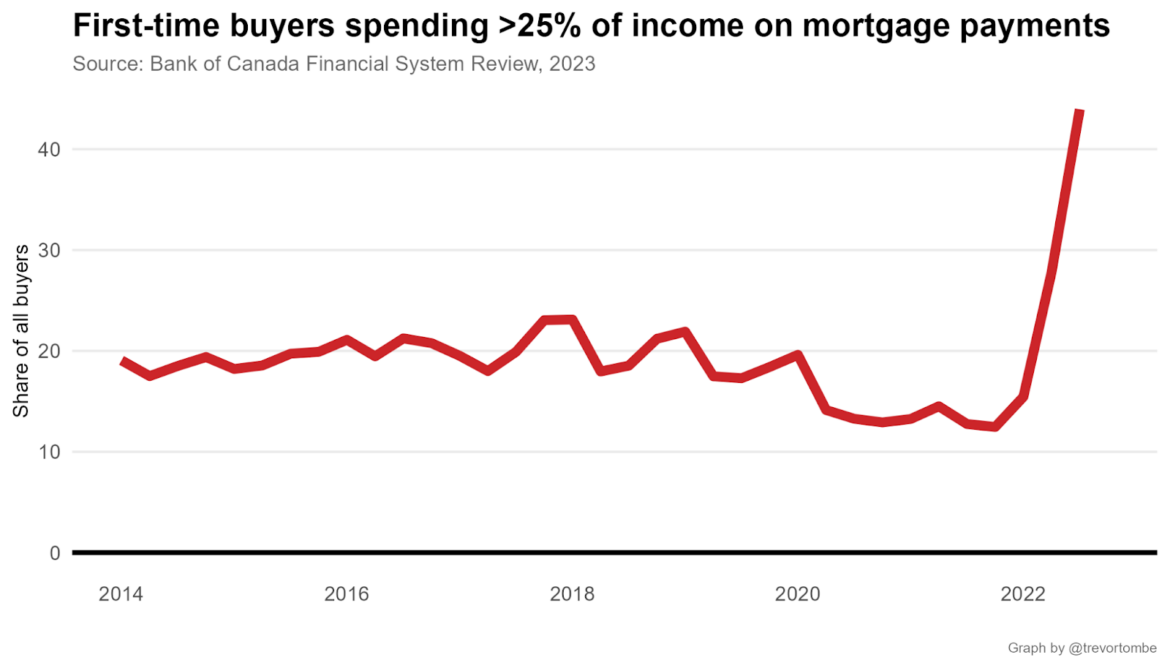

Young households are also typically new home buyers. The proportion of new homeowners who are devoting more than a quarter of their monthly income to mortgage payments is now substantially higher than it has been in the recent past. Today, nearly half of these buyers find themselves in this situation—more than double the normal share in most previous years. And while I don’t have data, these buyers are almost surely dominated by young Canadians.

This is where the risks are. Recessions normally lead to large increases in the share of households that can’t make a mortgage payment on time—a fact of the data that is strongly related to changes in the unemployment rate over the past half-century. That’s a real and serious risk, but not one faced by the majority of households. Indeed, it may not even be a concern for the average household.

But it most certainly is a risk for most young households. Little wonder that young Canadians are generally pessimistic.

Addressing this appropriately means a targeted response, with concrete policy ideas. “If there is a battle for the hearts and votes of young Canadians,” as Stuart Thomson noted in these pages recently, “it likely won’t be won with soaring rhetoric and patriotic appeals.”

In short, we should take the typical coverage surrounding Canadian household debt levels with several large grains of salt. Digging deeper into the data makes clear that Canada’s debt situation may not be as ominous as it first appears. At least, not when considering the overall picture.

Headlines that paint all households with the same broad brush divert attention from the genuine challenges confronting young Canadians. That’s where our focus should be.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School…

Recommended for You

The Notebook by Theo Argitis: Mark Carney’s first major tests

The Weekly Wrap: Trudeau left Canada in terrible fiscal shape—and now Carney’s on clean-up duty

‘Another round of trying to pull capital from Canada’: The Roundtable on Trump’s latest tariff salvo

Canada is losing ground on investment. Here’s where