Canada’s inflation fight continues.

“[The Bank] remains concerned that progress towards the 2 percent target could stall, jeopardizing the return to price stability,” it said after its July 12 meeting.

“While the Bank expects consumer spending to slow in response to the cumulative increase in interest rates, recent retail trade and other data suggest more persistent excess demand in the economy,” it continued.

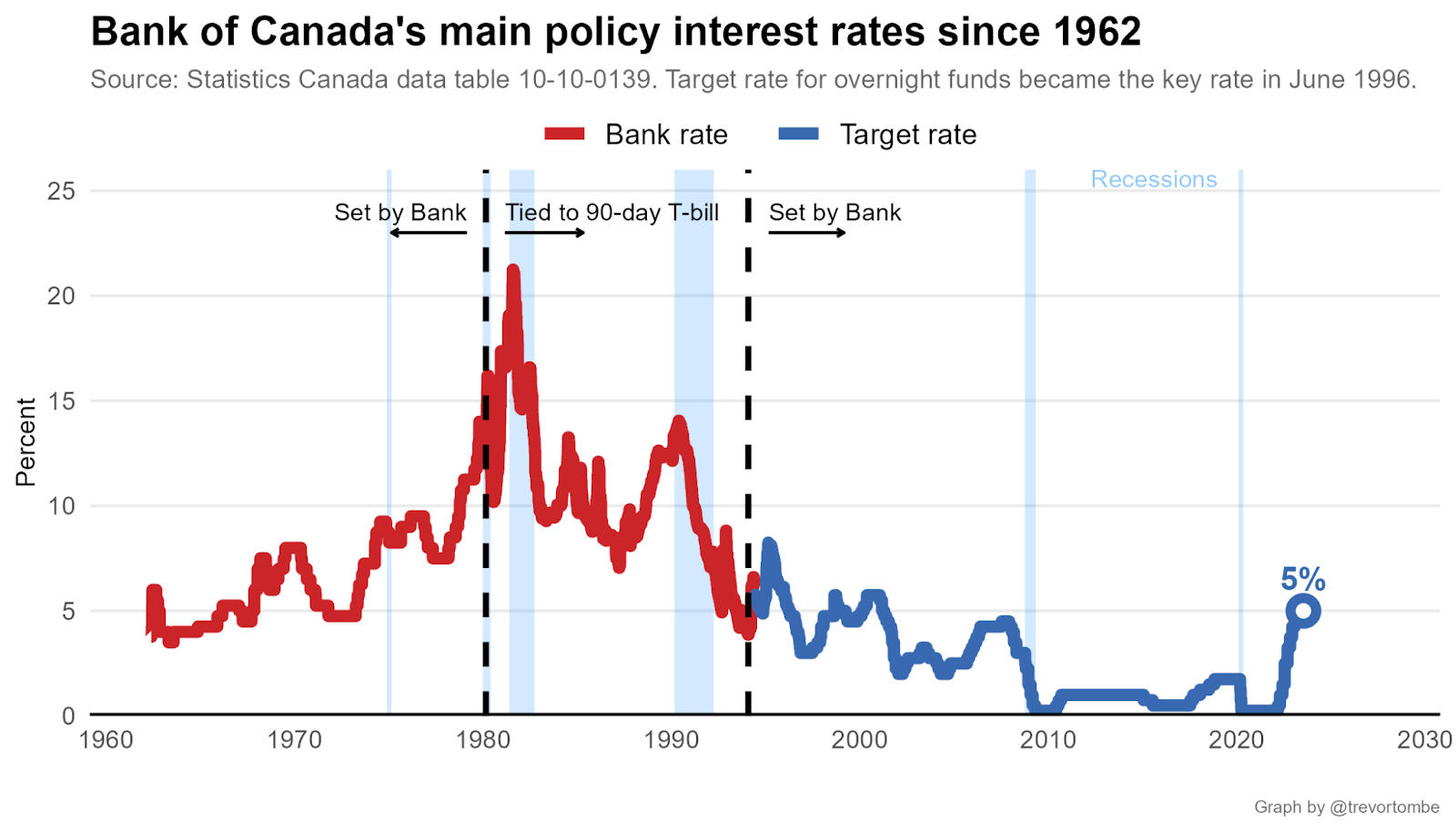

Given these concerns, Canada’s central bank raised its primary policy interest rate to 5 percent this week, which is the tenth increase since early last year, when the rate was barely above zero. We’re now at levels not seen since 2001, and the speed of the increase exceeds any in over four decades.

This raises borrowing costs for consumers, businesses, and governments. “We know this tightening cycle has not been easy for many Canadians,” said Deputy Governor Paul Beaudry recently, “but the alternative, not controlling inflation, would be far worse.”

The idea is simple: when interest rates go up, consumers and businesses demand less of many goods and services. This should take some of the pressure off prices. Even if the main items driving high inflation are not overly sensitive to interest rates, lower demand for other things could bring their prices down to compensate.

Knowing when to stop increasing rates is the tricky part.

Raising rates to 5 percent might have been the right move. Or it might have been a mistake. Depending on who you ask and what data they have in mind, the Bank may have gone too far or not far enough.

It is not clear which view is right. Even the Bank notes that “a considerable amount of uncertainty surrounds [its] forecast.”

Either way, the Bank of Canada opted for the least risky option. I’ll explain.

The Good News

First, the good news.

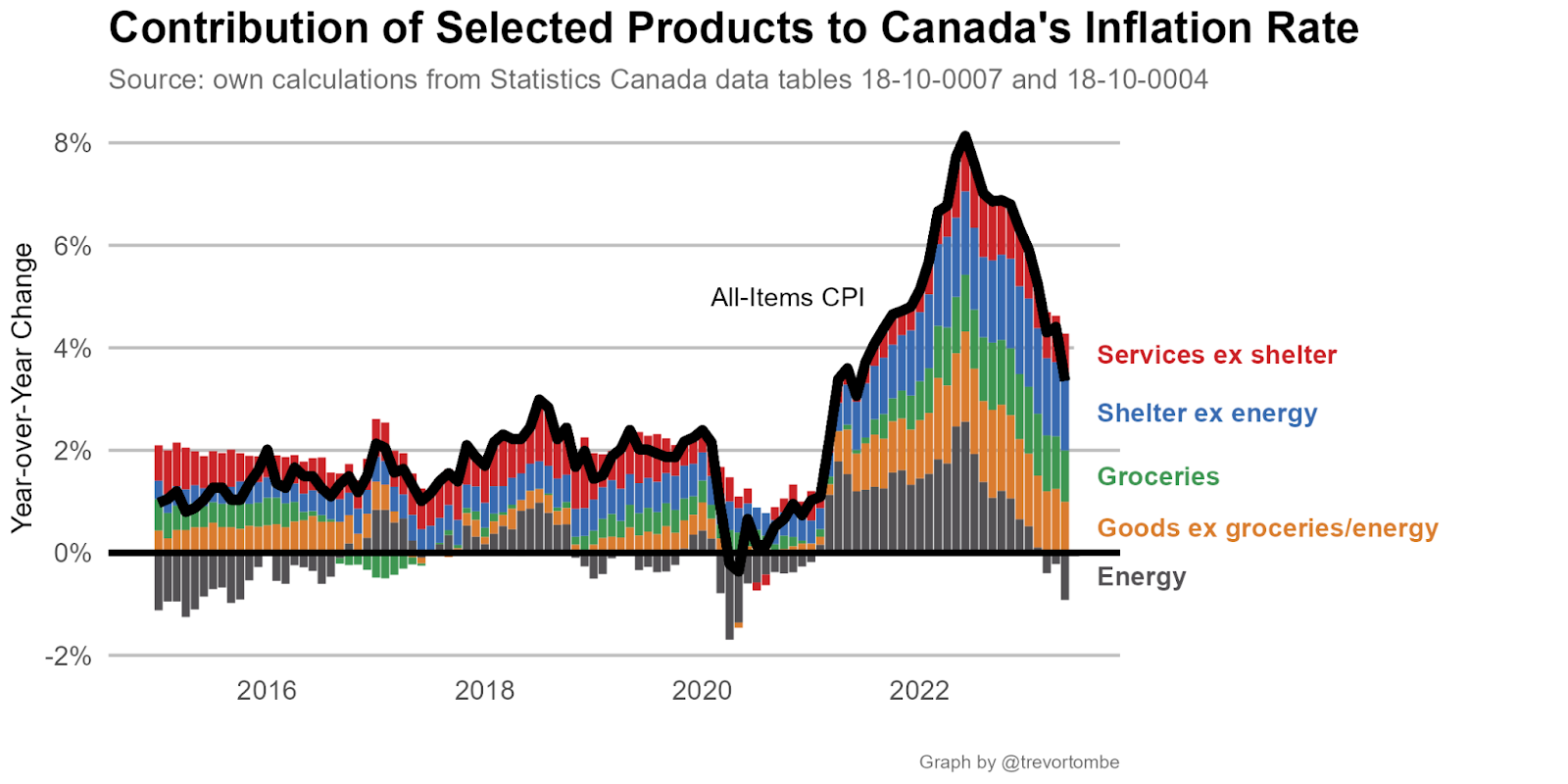

Consumer prices are 3.4 percent higher than they were a year ago, according to the most recent data for May 2023. This inflation rate is far lower than its peak of 8.1 percent last June. And most products tracked by Statistics Canada have seen a decrease in their pace of price change.

The big driver of this improvement is energy. It was the main reason why prices went up, and now it is the main reason why prices are going down. At least for this critical component, inflation pressures were indeed transitory.

There are also signs of improvement elsewhere.

Groceries are now the biggest current contributor to Canada’s high inflation. Increases for those items have thankfully begun to slow, and this should continue as production costs have also been easing. Goods inflation is also improving, especially as consumer demand for many consumer durables, such as furniture, major appliances, and certain vehicles, may be falling.

As for shelter costs, while still high, they may not be a big source of concern for the central bank. The biggest factor here is rising mortgage interest rates, which are up because of Bank rate increases rather than market conditions. In May, mortgage costs for homeowners contributed nearly a full percentage point. And among homeowners without a mortgage, I estimate their average personal inflation rate to be 2.6 percent, a full 0.8 points lower than for the average Canadian. This matters since if the Bank’s policy rates don’t rise further, neither will mortgage costs. We control which way they’re headed.

This is all good news. Most major items are trending in the right direction. Canada’s headline rate of inflation in June will almost certainly come in below 3 percent, and reaching our 2 percent goal may not be too far off.

This is one perspective. And one that suggests we’ve raised rates too high. But another way of looking at the data suggests a much more difficult road ahead.

The Bad News

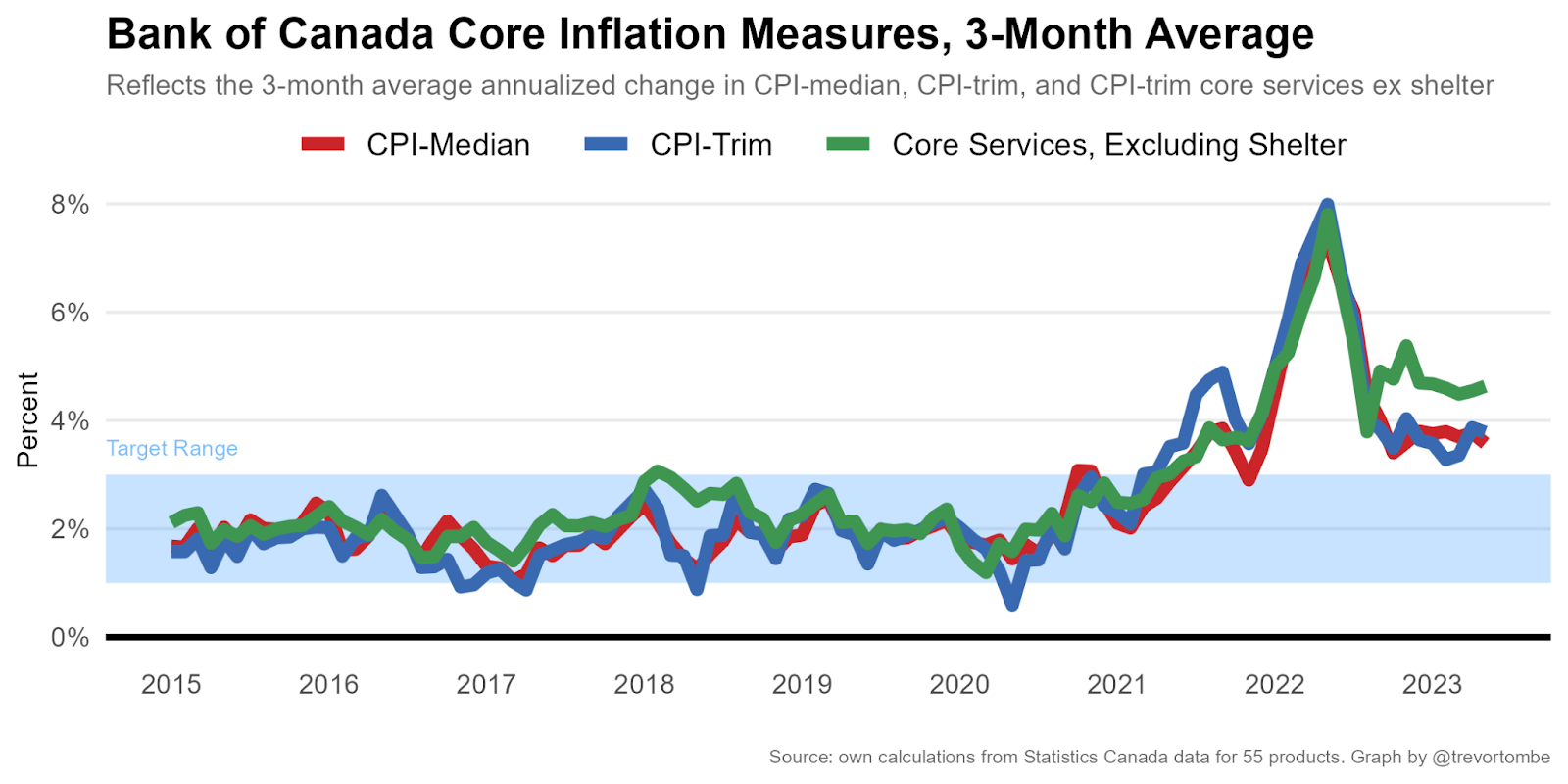

The Bank doesn’t just look at the overall rate of inflation when making its decisions.

Instead, it has a number of ways to measure “core” inflation that leave out volatile factors. This does not mean that things like food and energy are not important. Of course they are. But this approach to measuring inflation tends to provide a better indicator of where overall inflation is headed. It’s therefore a better guide to monetary policy decisions today.

Unfortunately, these measures are still too high and have stopped improving.

“The stubbornness of core inflation in Canada suggests that inflation may be more persistent than originally thought,” the Bank noted in its quarterly analysis of Canada’s economy.

Service (excluding shelter) inflation is particularly worrisome. Restaurant prices rose nearly 7 percent last year. Travel services rose nearly 12 percent. Consumers having significant post-pandemic pent-up demand for such services may complicate the Bank of Canada’s job. These are normally items that are sensitive to interest rate changes, but today consumers are buying more, not less, of these services.

These data suggest the path back to 2 percent inflation may be more difficult than the drop we’ve seen so far, and further rate increases may be necessary.

Choosing the Least Risky Option

So which story is the right one?

The truth is, no one really knows. Both the good and bad news stories offer important perspectives. And Canada’s central bank has a difficult job. Its decisions have a slow and uncertain impact on the economy.

But if raising rates yesterday was a mistake, it’s an easier one to correct. The alternative error, not raising rates when they should have, is worse. The longer inflation stays above our 2 percent goal, the more entrenched expectations become and the harder it is to fight.

This may be what the Bank of Canada has in mind, especially since, with the benefit of hindsight, we were probably too slow to raise rates two years ago. It does not want to make the same mistake twice.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School…

Recommended for You

‘Self-defeating’: The Roundtable on Trump’s costly tariffs and lessons learned, one year since ‘Liberation Day’

Canadians are leaving the country at record levels. Can anyone solve this pressing problem?

Was the Air Canada CEO turfed for his lack of French—or for something more concerning?

Government-run grocery stores would need to be ‘heavily subsidized,’ could be sued over food recalls: Food economist