Investment is vital to a nation’s economy. From buildings and equipment to research and development, all are necessary to enhance the productivity of workers, and none would exist without investment.

The idea is simple: more capital means we produce more for each hour we put in. Imagine a construction site without excavators, cranes, or other tools. More capital also means higher wages, better living standards, and more.

But deciding to invest is not a matter of mechanical arithmetic. Entrepreneurs and businesses must consider future conditions, regulations, taxes, and more when deciding where and how much to invest. Often, they must look many years or decades ahead.

Our prosperity depends on investment, but high uncertainty can cripple it.

Sometimes rising uncertainty is unavoidable, and delaying investment, hiring, or even our own purchases is a rational response. But other times, governments and politicians needlessly add fuel to the fire. This is unfortunately the case in Canada today and is—at least in part—likely behind some of our disappointing economic performance.

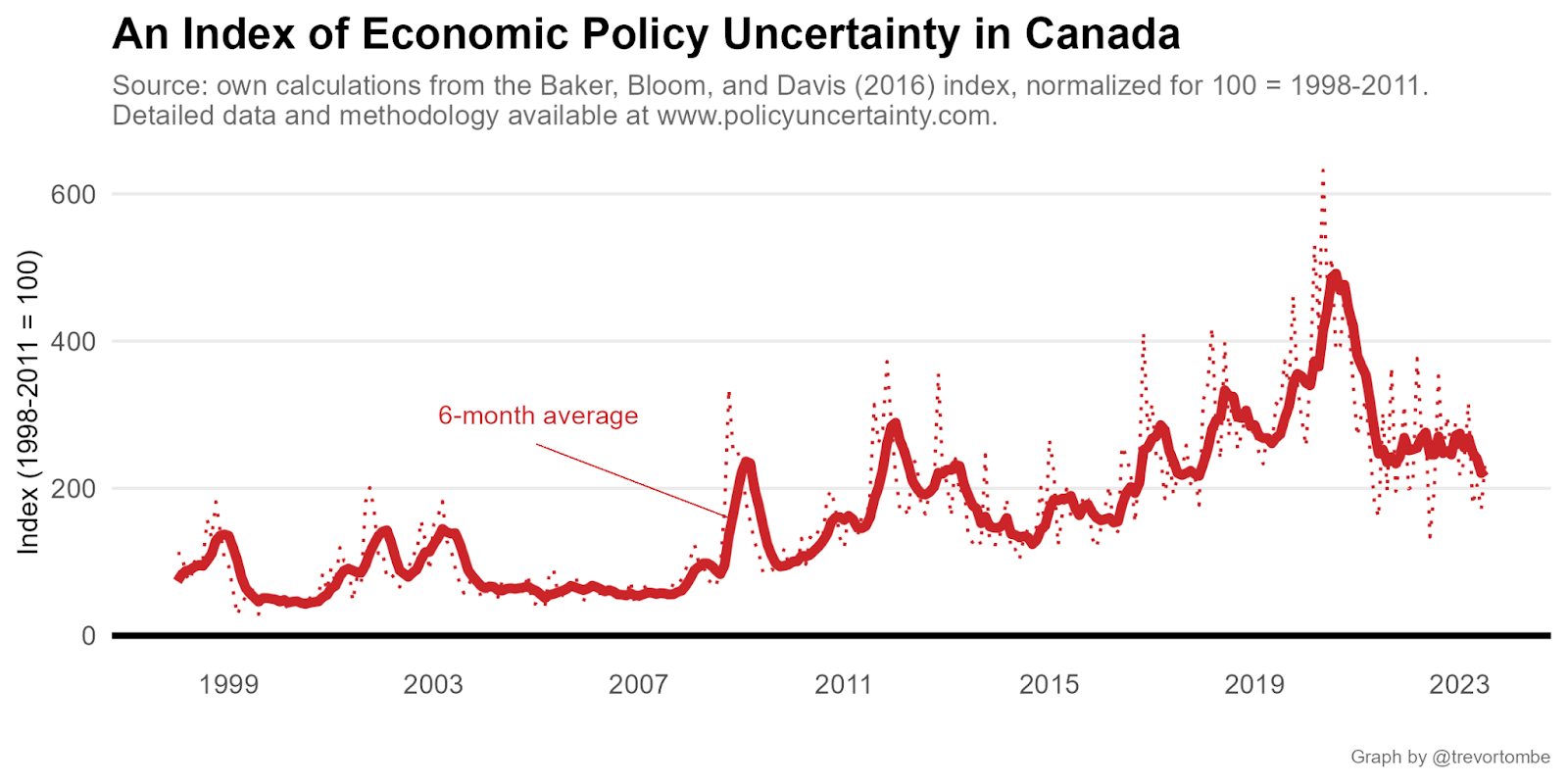

To estimate economic policy uncertainty, research from several leading economists, including Scott Baker, Nick Bloom, and Steven David, has resulted in robust measures across numerous countries based on a detailed examination of news articles.1You can read all the details here: https://www.policyuncertainty.com/methodology.html

According to this measure, economic policy uncertainty in Canada is high.

Although below our pandemic peak, today’s levels are far above historical norms.

Such a rise in policy uncertainty comes with real economic costs. These same researchers found that rising uncertainty in the United States after the financial crisis may have cut investment, industrial production, and employment substantially.

For Canada, the increase between 2014–15 and 2022–23 was even larger than that. Based on their results for the U.S., this might mean (and I must emphasize that this is just an illustrative back-of-the-envelope exercise) that Canadian investment may be 8 percent lower, industrial production over 1 percent lower, and employment roughly 0.5 percent lower due to this higher uncertainty.

This might seem like a small change, but it translates into about 100,000 fewer jobs and meaningfully lower real incomes. This is anything but trivial.

It’s true that uncertainty is higher in many countries. Globally, it is way up. But in Canada, it has risen more than in both the United States and the United Kingdom—two common comparators, and countries where Brexit (in the case of the U.K.) and remarkably high political dysfunction (in the case of the U.S.) might have led one to expect the opposite.

We have seen too many instances of unnecessary government-driven policy uncertainty in Canada. Consider Alberta’s abrupt interference in regulatory processes to halt investment in renewable energy. Billions in private unsubsidized dollars were poised to flow into wind and solar, only for this bomb to drop that not only pauses investment today but creates confusion and dents confidence in the future. It is not just electricity. Investors outside politically-favoured sectors may rightly worry about sudden and unexpected policy changes affecting their projects.

The federal government, too, has been muddying the waters. Recent examples include a poorly developed idea to tax sharing Canadian news, an ad-hoc approach to massive industrial subsidies, and ever-changing climate policies tilting towards regulatory actions that target certain sectors for extra burdens while others get special breaks.

It is not just government decisions. Politicians—both in government and in opposition—can affect things. Those seeking to form governments should be cautious about completely abandoning a previous government’s decisions. If they do, consider compensating those who invested under previous rules.2Recent discussion around federal “contracts for differences” is an interesting example of how to do that. We also currently do this in many of our free trade agreements with other countries’ investors, with compensation paid if adverse policy decisions are made.

Deliberate political polarization can also increase uncertainty. If each party focuses on manufacturing rage instead of thoughtful policy (a common theme across federal parties), then election outcomes become wild cards, capable of triggering more significant and less predictable shifts. Policy becomes more of a communications exercise than a tool to improve the country or a province and thus may become far more uncertain.

Recent work confirms this. Economists Scott Baker, Aniket Baksy, Nicholas Bloom, Steven Davis, and Jonathan Rodden find that uncertainty is higher around elections. But around close and polarized ones, uncertainty rises by more than double the normal amount.

None of this means policy should remain stagnant, of course. Transparent processes can lead to improvements that ease burdens and barriers rather than add to them. Rising uncertainty may also be a cost worth paying to achieve some other objective (as pro-Brexit arguments might go). If that cost is recognized up front, then fair enough.

But in the end, confidence in the rules laid down by governments is essential for all long-term decisions. The global economy is volatile enough. Politicians in Canada shouldn’t make matters worse.