Labour disruptions are on the rise.

Recent strikes have closed Metro stores and B.C. ports. Universities, Ontario construction sites, Vancouver hotels, and Canada’s largest cemetery have seen the same. Work stoppages at Air Canada and WestJet, which would have had massive spillover effects throughout the economy, were only narrowly avoided. Even Federal public servants went on strike to demand higher pay and flexible work arrangements.

These are not isolated incidents.

Last year, over 2.1 million work days were lost to labour disputes—almost double the amount in 2019 before the pandemic hit and the highest since 2009. This year, we’re on track for even more. From January to June, we’ve already experienced over 1.6 million lost work days. That’s more disruption in the first half of any year since 2002.

And there’s more to come. The United Auto Workers, along with their Canadian counterparts in Unifor, for example, have voted overwhelmingly in favour of a strike if a deal isn’t reached soon.

This may not be too surprising. Inflation rose last year to highs not seen since the 1980s and did so faster than at any point since the 1950s. Rising prices mean wages and salaries can buy less than before, so the real value of pay is down.

And while inflation has eased considerably, affordability challenges remain. In recent analysis for The Hub, I showed that price levels are over six percent higher than they would have been had inflation remained on target.

Workers are naturally going to push hard to recover this lost purchasing power. With tight labour markets, they often have the power to demand just that.

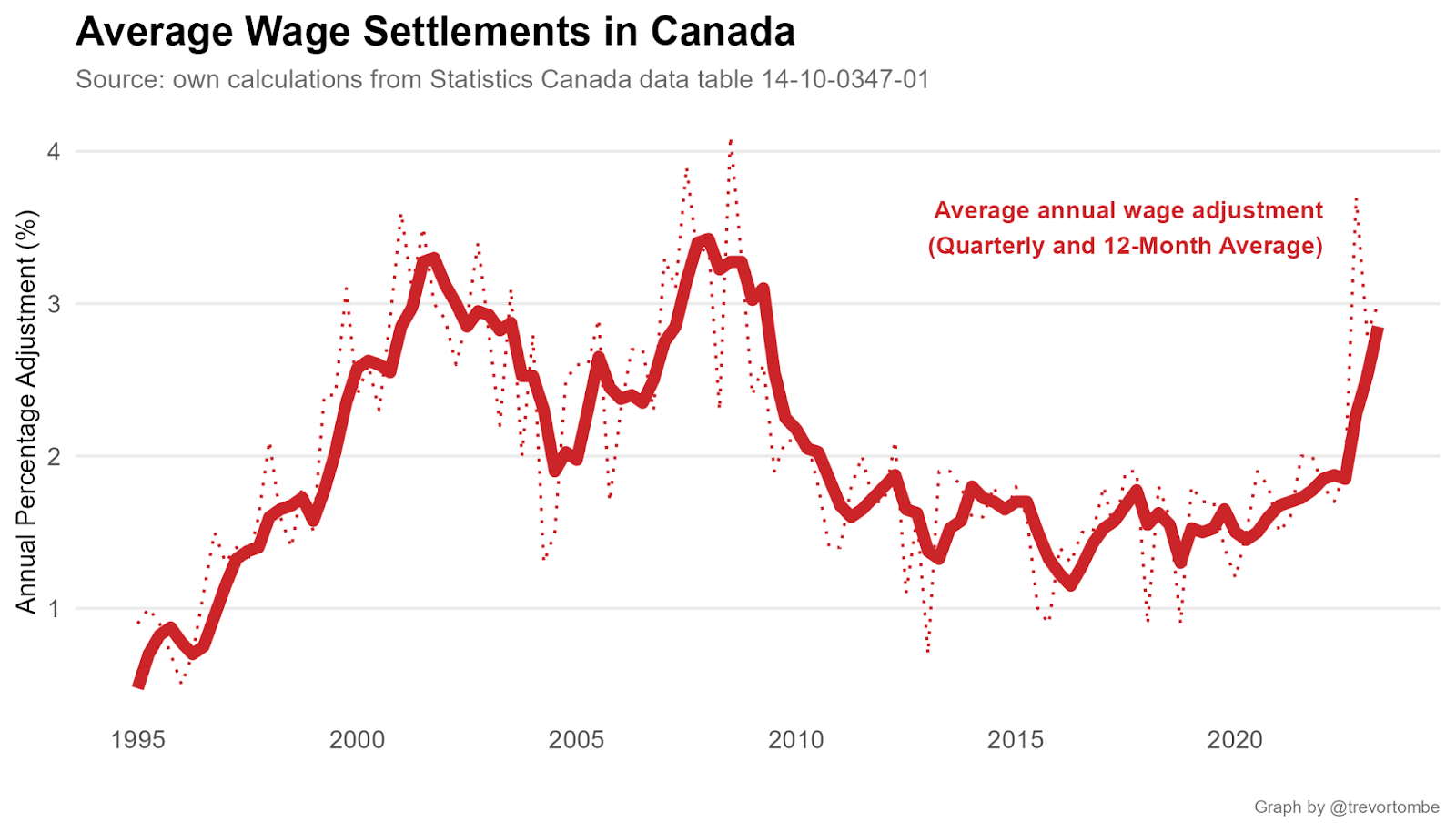

Indeed, we’re already seeing wage settlements agreed to in recent collective agreements rise sharply. Of the 26 major settlements reached in the first half of this year, the average annual wage increase was nearly three percent per year. That’s double the roughly 1.5 percent annual increases normally agreed to in the years prior to the pandemic, but still below inflation.

We should expect this trend to continue. Business leaders surveyed by the Bank of Canada expect wage increases over the coming year to average roughly 4.5 percent.

But as more contracts come due while broader economic conditions weaken, it may become increasingly difficult for many employers to meet rising wage demands. This could lead to more strikes, work stoppages, and disruptions throughout the economy.

We’ve seen this before.

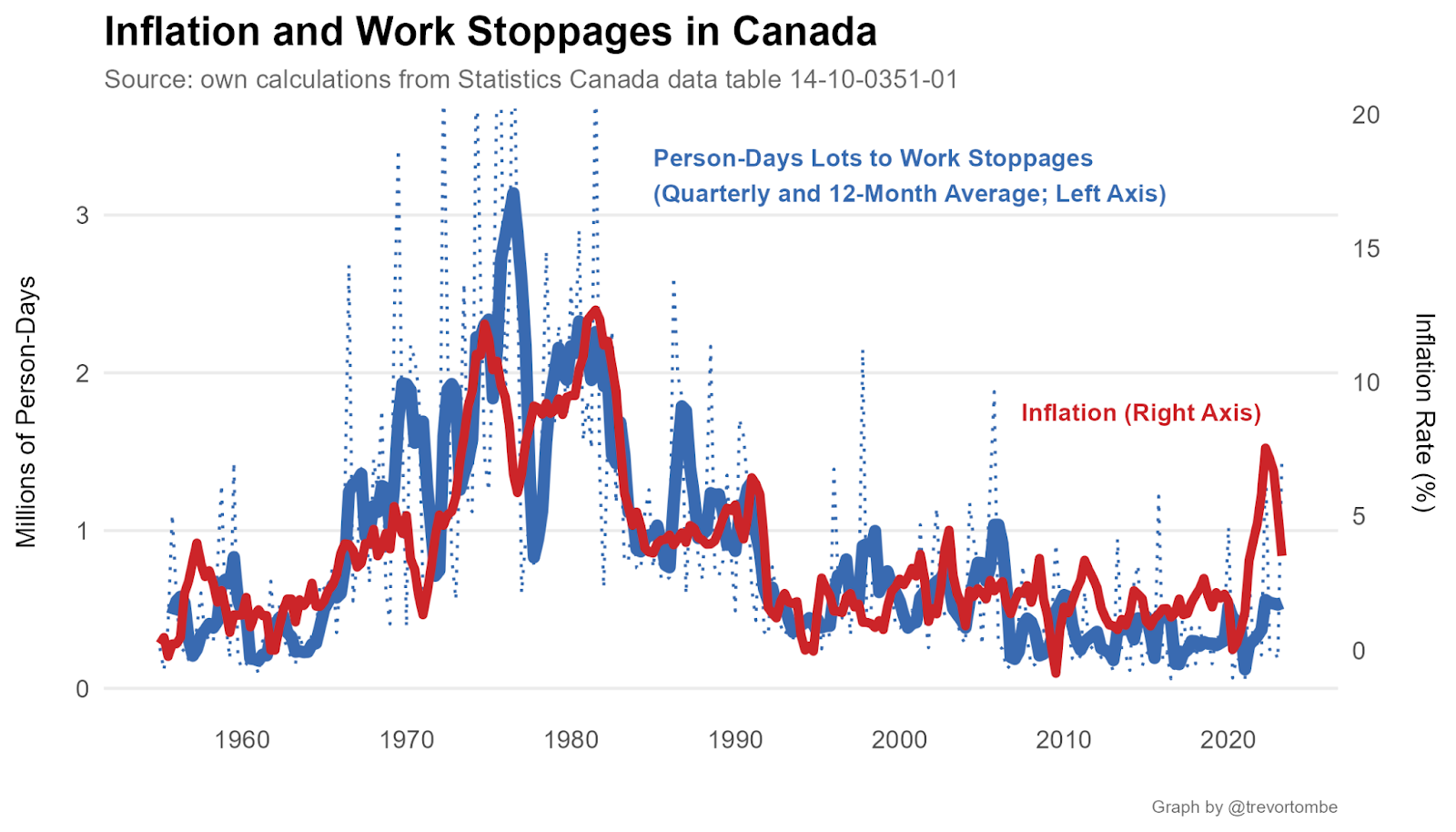

Historically, the frequency and scale of work stoppages tracked very closely with overall inflation.

Starting in the late 1960s, inflation gradually rose. By the 1970s, it exceeded ten percent at some points and remained uncomfortably and persistently high until the early 1990s. Strikes and other labour disputes dramatically increased. From less than half a million days per quarter lost to work stoppages in the early 1960s, disruptions rose sharply to over four million days per quarter by 1974.

Such disruptions took a significant economic toll. In 1976, there were nearly 12 million days of work lost. That’s possibly around 80 to 90 million hours where workers earned no wages and firms produced no output—equivalent to nearly as much as two to three percent of all hours worked in the entire economy.

Today’s situation is less bleak, with disruptions accounting for approximately 0.5 percent of total work hours. But even a modest increase could be a drag on Canada’s already weak economic growth.

There’s some reason for optimism, though. The rise in strike action in the 1970s and early 1980s was due to more than just rising inflation. It was also due to uncertainty around what future inflation would be. Some, such as former Bank of Canada governor David Dodge, have argued that many wage demands at the time were made as insurance against unexpected increases in inflation over the life of the employment contract. Uncertainty itself was therefore a driver of rising wage demands and resulting strike actions.

Today, things are different. The Bank of Canada—along with central banks around the world—is aggressively moving to get inflation back to a clearly defined target of two percent. Some may not believe that they will succeed, of course, but overall inflation expectations today are far better anchored than they were a half-century ago.

Over the next five years, Canadian consumers expect inflation to average roughly three percent per year. And businesses expect almost as much. With less uncertainty around future inflation, it may be easier to negotiate and agree to more gradual adjustments to worker pay and conditions.

If the Bank of Canada can successfully and sustainably return to normal rates of inflation soon, then its credibility may improve and bargaining may become easier.

But if it cannot, then turbulent times for both employers and workers alike may be ahead.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School…

Recommended for You

The Notebook by Theo Argitis: Mark Carney’s first major tests

The Weekly Wrap: Trudeau left Canada in terrible fiscal shape—and now Carney’s on clean-up duty

‘Another round of trying to pull capital from Canada’: The Roundtable on Trump’s latest tariff salvo

Canada is losing ground on investment. Here’s where