Canada’s finance minister, Chrystia Freeland, will provide a fiscal update next Tuesday. It will not be pretty.

Federal finances are under increasing strain from slowing economic growth, expanded affordability measures, new social programs (such as dental care), massive subsidies for battery plants, and, perhaps most important of all, rapidly rising interest rates.

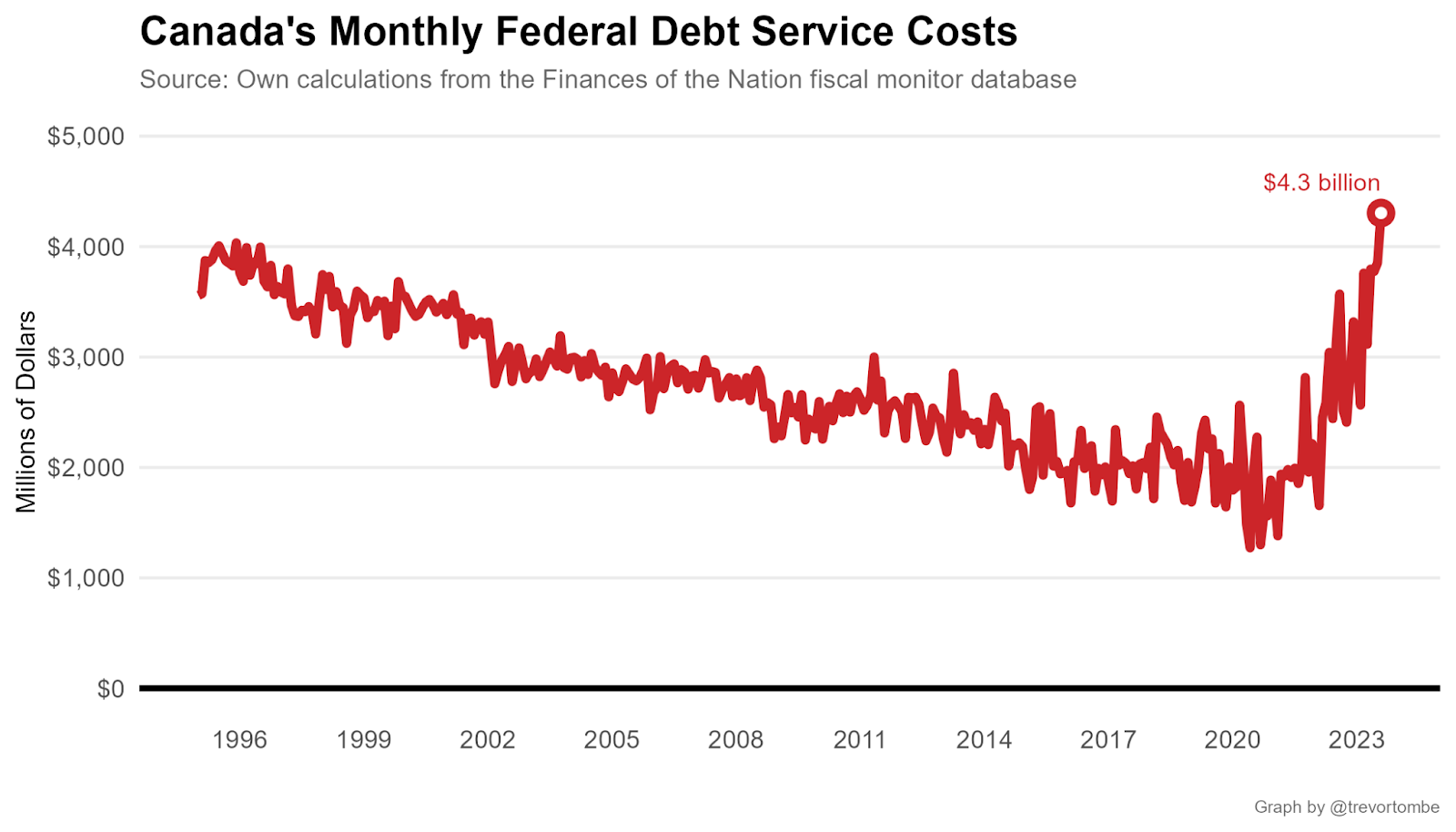

In fact, the monthly interest costs of the federal government are now at an all-time high. The latest available data for August shows federal interest costs exceeded $4.3 billion, surpassing the previous record of $4.03 billion set in December 1995. It’s more than double the pre-COVID amounts, as I illustrate below. And it’s the fastest acceleration in interest costs in recorded history.1While the fiscal monitor data does not extend further back than 1995, my own estimates of monthly costs inferred from the historical public accounts suggest very strongly that August 2023 is indeed an all-time record but I’m willing to be corrected.

At this rate, annual interest costs could exceed $50 billion—four years ahead of schedule.

All this means that when Minister Freeland updates the numbers next week, the federal deficit will almost surely grow. A lot.

In the PBO’s latest economic and fiscal outlook, they anticipated a $46.5 billion deficit this year—up from the budget’s $40 billion.

Other projections suggest we may see an even larger deficit. The latest projection by Finances of the Nation, which releases new figures every month, including a new set published last week, projects a deficit of just under $56 billion this year.

That may be overly pessimistic, of course. But if it is even close to accurate, then it would be a very large increase indeed. Excluding the COVID-19 years, which are obviously an exception, it would be an over $20 billion increase over last year. That’d be the largest increase since the financial crisis. And controlling for the health of the economy (using what’s called the “cyclically adjusted budget balance”), it would be the largest deficit, as a share of the economy, since 1995.

This doesn’t mean we’re headed over a fiscal cliff.

Relative to the size of government or the overall economy, the burden of these high interest costs remains lower than it was in the mid-1990s. Far lower. In 1995, interest costs were 35 percent of revenue and nearly 6 percent of our entire economy. Today, even if interest costs exceed $50 billion, that would be 11 percent of revenue and less than 2 percent of GPD. And central banks should start lowering their policy rates next year, perhaps by spring or earlier, as inflation pressures recede.

Canada is also not alone. Indeed, the situation abroad is even worse. Based on the latest data compiled by The Economist, the U.S. federal deficit is set to reach 5.7 percent of GDP this year, equivalent to roughly $165 billion in Canada. Borrowing in the Euro area is 3.4 percent. The U.K. is 3.9 percent. Indeed, of all the countries it tracks—developed and developing alike—only three expect a surplus: Australia, Denmark, and Norway.

However good the company we may be in, though, Canada has a challenge on its hands.

The federal government’s 2023 budget was based on a 10-year interest rate of approximately three percent. That may now have to increase by half a point, which could increase borrowing costs by several billion per year for the foreseeable future.

And if rates stay higher for longer, as many (including the Bank of Canada) now expect, the government’s debt levels may not be sustainable.

Consider a situation where federal borrowing costs average 3.5 percent, government revenue and economic growth slow to an average of 3 percent, and government spending grows at 3.5 percent. I estimate that federal debt GDP by 2028 would reach 47 percent—roughly where it was at its highest level following COVID-19. This is far higher than the government’s plan for 40 percent that year.

Federal debt that grows faster than the economy is not sustainable. If the fiscal update shows that, alarm bells should ring.

What can Canada do? As I’ve noted before, sticking with the government’s own previous plans would be a good start. Ratcheting up spending plans with every single budget is an important reason why we’re in this situation. Looking ahead, those seeking to replace the current prime minister—whether within the Liberal Party or Pierre Poilievre of the Conservatives—should start considering options.

The longer we delay, the larger and more difficult our fiscal challenges will become.