Canada’s June 2023 inflation rate fell to 2.8 percent. Compared to 8.1 percent a year earlier, this is a significant improvement. This is inflation’s fastest decline in over forty years.

The finance minister was quick to claim credit, tweeting “Canada’s plan to bring down inflation is working”.

But hold your applause.

This drop in inflation isn’t the result of the government’s actions or policy choices. It’s largely due to a fall in global energy prices. This one factor alone accounts for a full 3.7 percentage point drop in Canada’s inflation over the past year. That’s 3.7 out of a total decline of 5.3 points. That means energy alone accounts for roughly 70 percent of the total improvement.

Whatever the cause, falling inflation is good news. But it doesn’t mean Canada’s affordability challenges are over. It just means things are not getting worse as fast.

Consider this: had inflation remained on target since February 2020, prices would be about 7 percent higher today—half the increase we have seen. To be precise, prices are now 6.3 percent higher than they would have been had inflation remained on target.

The recent return of inflation closer to its two percent target simply means prices are rising at a more normal pace, not that affordability has improved.

And if we successfully maintain inflation at 2 percent from this point forward, we effectively lock in this overall increase. Even this is optimistic since inflation remains above target and the Bank of Canada expects that to continue for a while longer.

Simply put, affordability will remain a major issue for years to come.

For perspective, if prices were magically frozen at today’s level, it would take a little over three years to return to our previous price level trajectory. That’s July 2026, well after the next federal election.

It is unclear how long it will take Canadians to regain their purchasing power. Wages usually rise faster than prices. Not by much, of course, especially given Canada’s disappointing recent productivity growth. In the decade before the pandemic, average hourly wages grew by roughly 2.5 percent per year. Inflation over that same period averaged 1.7 percent. If this same gap between earnings and inflation continues, it will take nearly eight years for real (inflation-adjusted) earnings to rise enough to offset the 6.3 percent rise in prices.

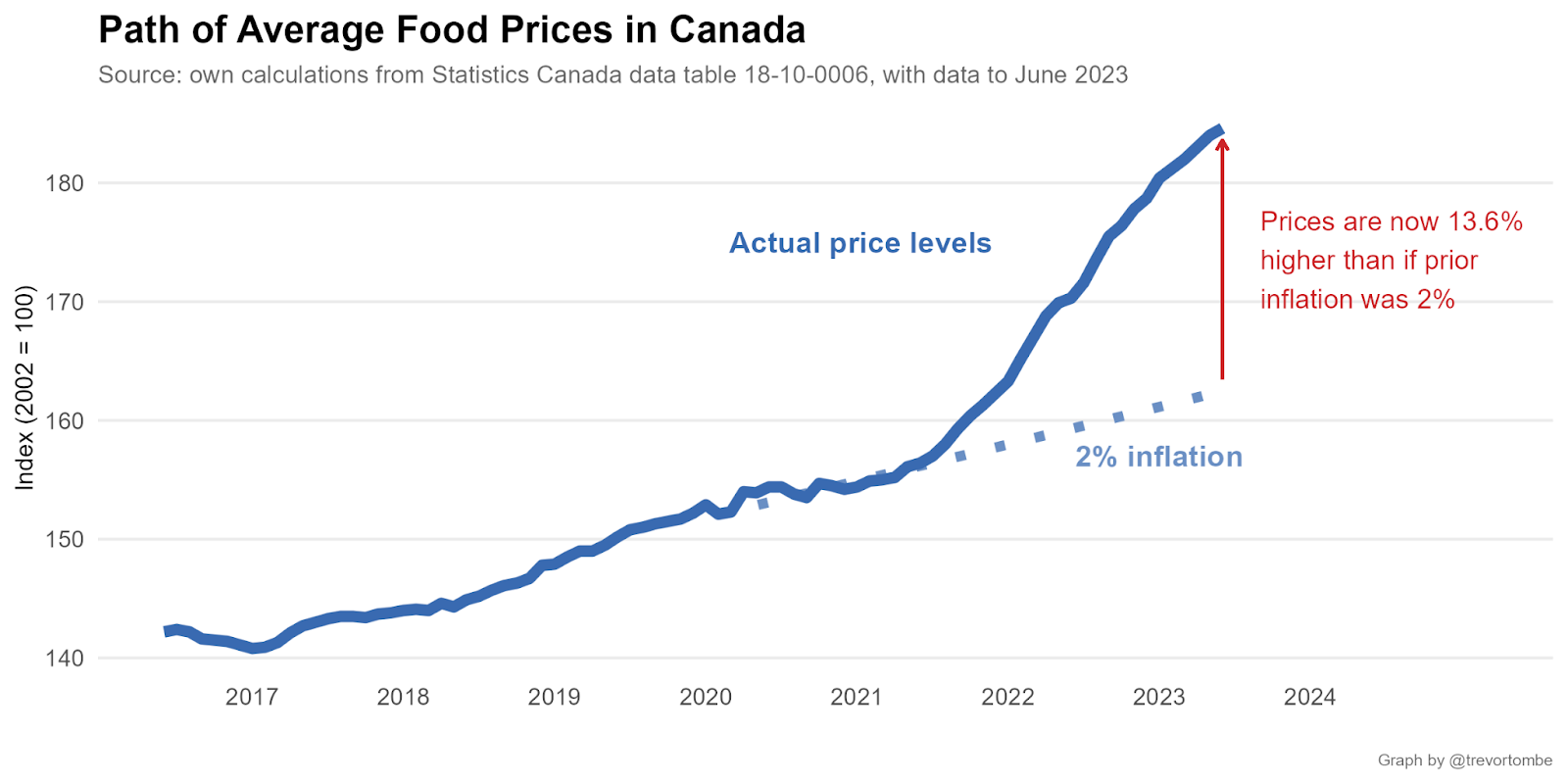

Perhaps more concerning for many—and potentially more relevant to understanding the psychological and political dynamics of affordability as an issue—is the fact that prices have ratcheted up even more for many of the most important items we buy. Food prices are nearly 14 percent higher than they would have been if annual increases were limited to 2 percent. And this gap continues to widen.

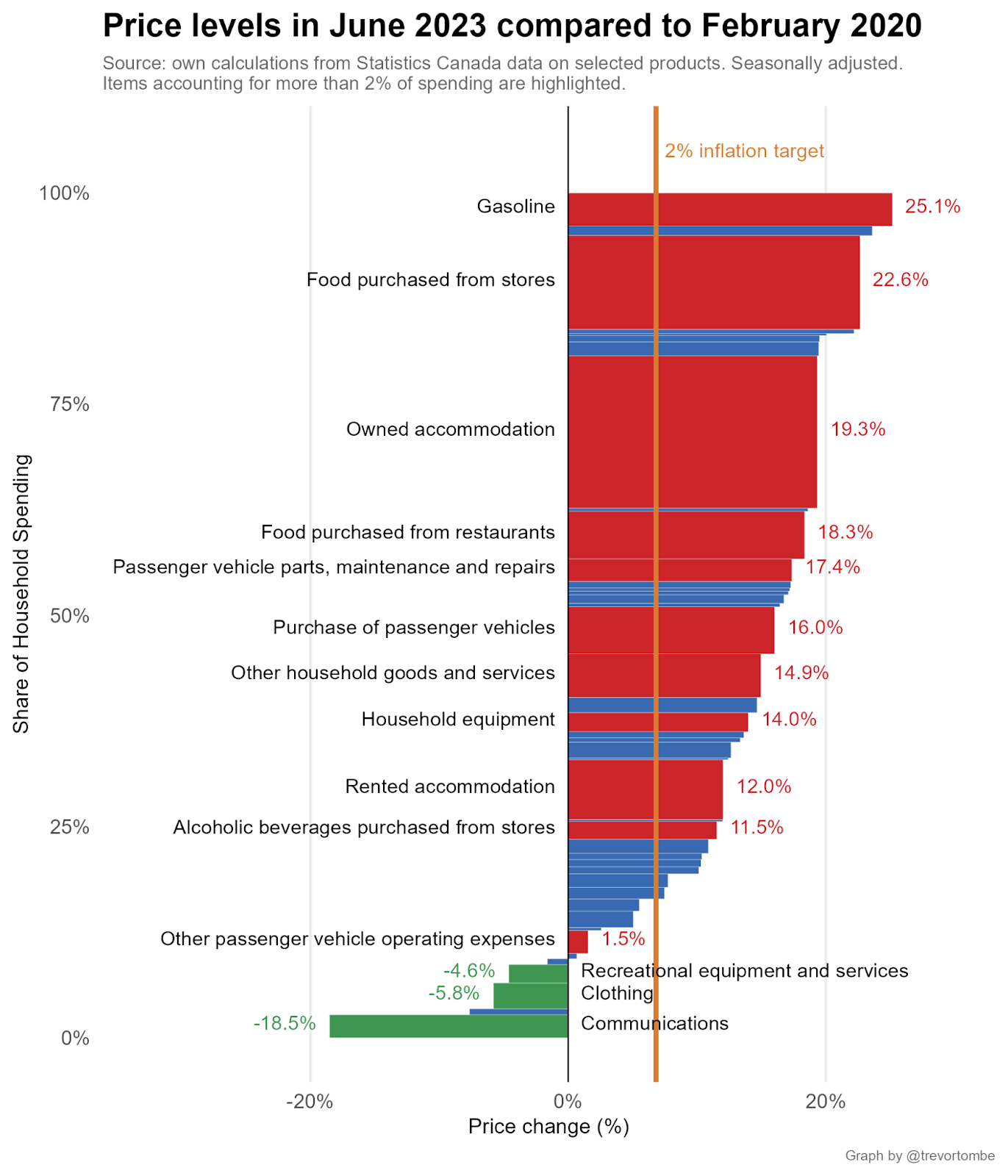

Transportation prices (up largely because of gasoline) are still 7.7 percent higher, despite recent declines. Shelter prices are 9.4 percent above what they would have been. Health and personal care items are 6.2 percent higher. And so on.

Not everything is more expensive. But almost everything is.

Using detailed data on products tracked by Statistics Canada that form the basis of the Bank of Canada’s core inflation measures, I estimate that nearly 85 percent of consumer spending is on goods whose price levels rose faster than the target rate of inflation. I illustrate each below, both in terms of price changes since February 2020 and each item’s share of average household consumer spending.

Internet and phone plans are cheaper. Recreational and clothing prices have dropped too. And childcare services are nearly 8 percent cheaper than before the pandemic.

But almost everything else is way up.

To be clear, the price of specific items will rise and fall as supply and demand conditions change. On average, though, price levels have permanently ratcheted up for the simple reason that the Bank of Canada targets inflation, not prices. It is legally mandated to target average annual price increases of two percent. For price levels to return to their prior trajectory anytime soon would require deflation, which the Bank will not permit.

I’m not suggesting this is a problem with the Bank of Canada’s mandate. Not at all. There are pros and cons to targeting inflation rather than price levels.For some excellent research and discussion, see material produced for a recent conference at the Max Bell School of Public Policy. Returning Canada back to its previous path—which would keep average inflation at 2 percent over the long run and provide more certainty to individuals and businesses—comes at the cost of a more volatile economy. It may also be confusing. Regardless, the current mandate is in place until December 31, 2026, and it would be extremely unwise for the government to change it before then.

To improve affordability, governments must look to other policies. At the risk of sounding like a broken record, there should be no more important priority than boosting Canada’s lagging productivity growth, building more, and avoiding unnecessarily costly policy mistakes.

Unfortunately, even a renewed focus on improving Canada’s economy will take time to bear fruit. In the meantime, while the recent decrease in inflation is welcome news, the reality is that Canada’s affordability challenges will persist for many years to come.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School…

Recommended for You

Canada has a long, hard road ahead if it wants to meet its lofty investment ambitions

Why Canada’s GDP per capita crisis is real: DeepDive

What rising oil prices mean for your bank account

Canadians should prepare for prolonged high inflation if war in Iran persists: Economist Trevor Tombe