Next week the Bank of Canada will announce its third rate decision of the year. After signaling a pause in further tightening, it is unlikely to move off its current 4.5 percent policy rate.

But inflation is currently at 5.2 percent, far above the Bank’s target range of 1 to 3.

So why would our central bank pause further increases while inflation remains so high?

Two reasons: first, inflation pressures have likely already ended, despite the high headline rate most coverage focuses on; and second, it takes time for interest rate hikes to have their full effect—and today, thanks to the large number of variable rate mortgages out there, it might take longer than usual.

On the first point, the data is crystal clear.

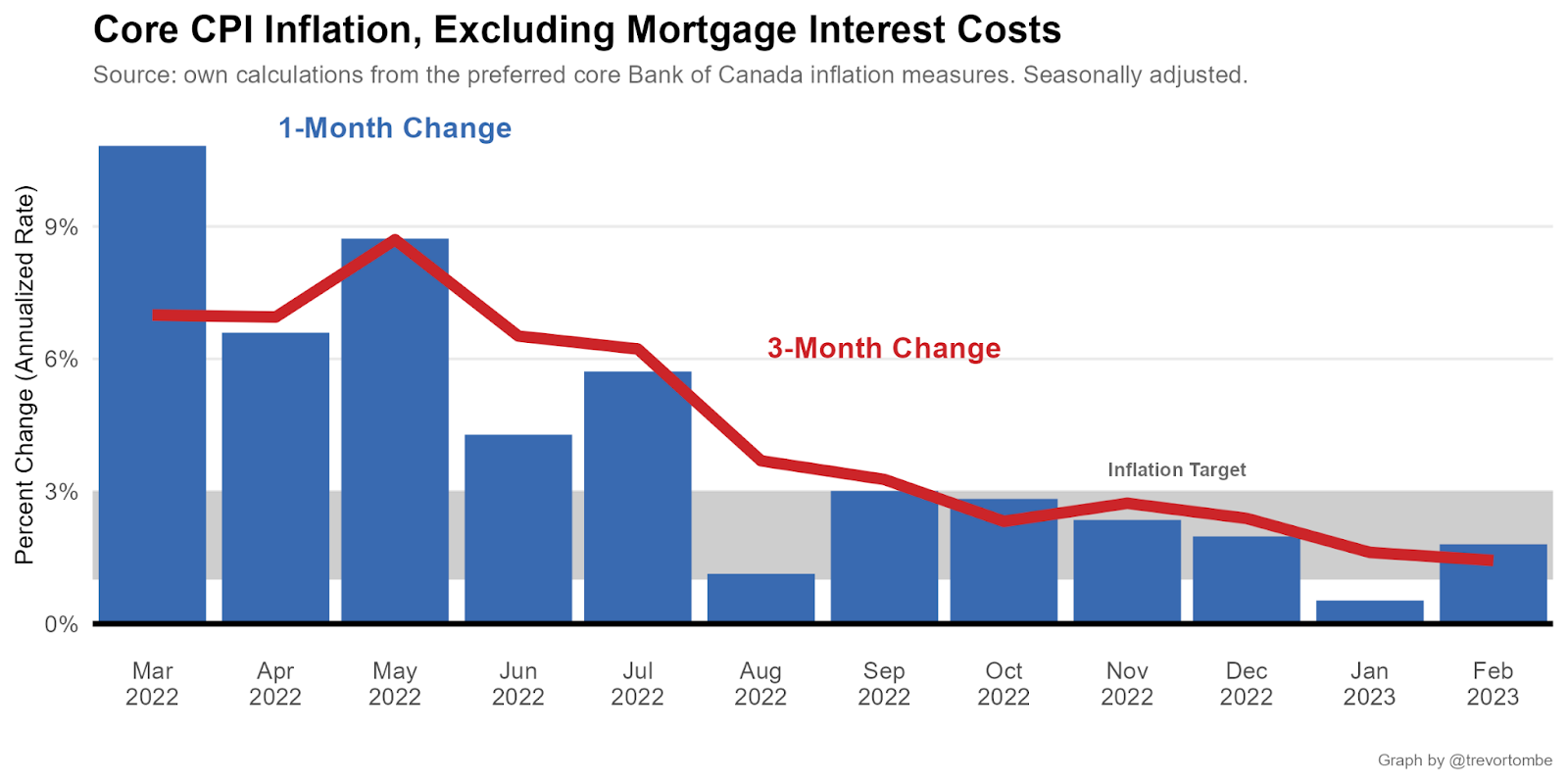

Excluding volatile components like food and energy, and excluding the policy-driven increase in mortgage interest costs, inflation is consistently within or below the target range for most of the past seven months.

Excluding these items doesn’t mean they don’t matter, to be clear. Increases in the price of any item can strain household budgets. But excluding volatile components provides a better indication of where inflation may be headed. Excluding mortgage interest costs also narrows our focus to prices determined by supply and demand rather than policy.

But even including food and energy, prices have increased at an average annualized rate of less than 0.3 percent over the past three months and only 2.5 percent over the past six months.

The reason reported inflation remains so high isn’t because prices are rapidly rising. Instead, it’s because the calculation reflects all of the monthly price changes for the past year.

So despite the sharp recent decline in the pace of price increases, we have to wait until the large increases in the first half of 2022 fall out of the calculation. If recent trends continue, though, we could see close to normal rates of inflation by this summer—so there may be no more need for the Bank to tighten further.

The second point—that rising rates take time to fully affect the economy—is even more important. Especially today.

Higher interest rates affect our spending in several ways. Borrowing is more expensive, so we spend less on items that we typically use debt to purchase (such as vehicles, renovations, new homes, and so on). Higher rates also make many of us poorer (look at home prices recently), which leads to lower spending.

Recent estimates suggest that each one percentage point increase in the Bank’s policy rate tends to decrease consumption spending by 1.7 percent—but this effect can take well in excess of two years to fully materialize.

Today, another channel may complicate this picture and lead to even longer lags than usual.

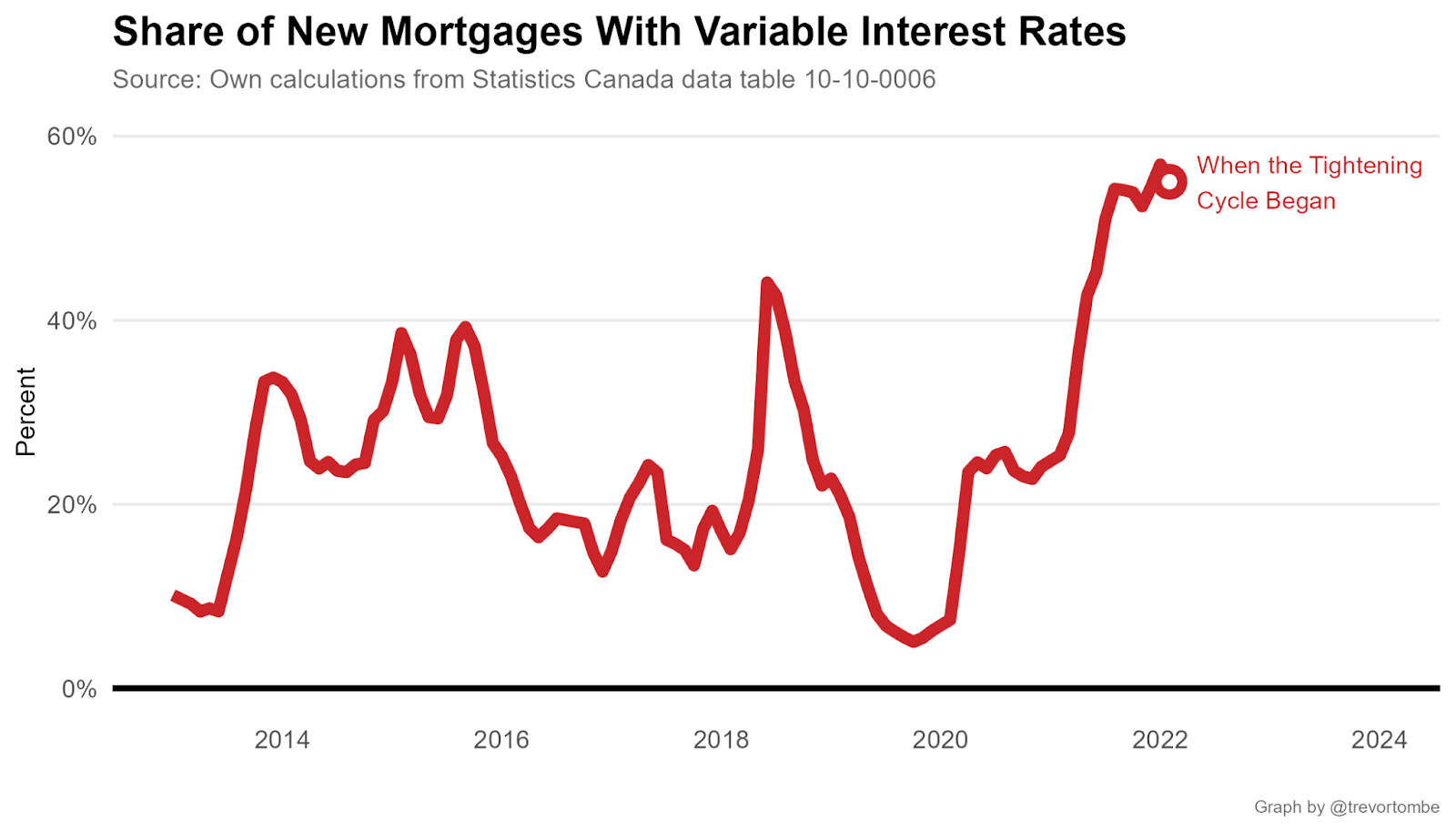

When rates rise, people pay more to service their debt and so have less to spend on other things. Those with variable rate mortgages are particularly exposed, but not right away.

Many households with variable rate mortgages—which account for roughly one-third of all mortgages, and most of which have fixed payments—now have monthly payments that are less than what they owe in interest. Depending on the Bank, somewhere between one-fifth and one-third of all outstanding residential mortgages are in this situation.

The result: instead of the total amount owing going down as payments are made, their mortgages are actually growing each month. This “negative amortization”, as it is called, will continue until rates decline. And when these mortgages come up for renewal, monthly payments may have to rise significantly to make up for it.

In effect, variable rate mortgages shift some of the burden of recent rate increases well into the future. And there were a lot of such mortgages issued right before the tightening cycle began. In fact, a majority of new mortgages had variable rates.

Much depends on the path of future rates, of course, but consider someone on a variable rate fixed payment mortgage that started at one percent on a five-year initial term. If they renew at three percent at the end of their term, monthly payments could rise by roughly one-third or more. On a $400,000 original mortgage, I estimate that could mean an extra $500 to $600 per month more than what they paid during the first five years.

It will take several more years for recent rate increases to fully affect these borrowers.

Of course, one option to avoid a sharp increase in payments may include extending the mortgage amortization at the time of renewal.Be sure to talk with a professional advisor or mortgage broker; I’m not providing any advice here, just illustrating some general issues. But even this comes with significant, though somewhat hidden, additional interest costs over the life of the now-longer mortgage.

Either way, thanks to the larger number of variable rate mortgages out there, pressure on many households to lower spending may continue even long after rates fall back to normal levels.

The Bank of Canada’s job is never easy; it is especially difficult today.

A pause in any further rate increases is entirely warranted, and we may even see cuts in the not-too-distant future. But since rate hikes over the past year may have unusually long-lasting consequences for Canada’s economy, our central bank’s job of managing recent disruptions is far from over.

Trevor Tombe is a professor of economics at the University of Calgary, the Director of Fiscal and Economic Policy at The School…

Recommended for You

‘The race is tightening up’: Darrell Bricker on what the polls are showing heading into the final weekend of the election campaign

Derrick Hunter: Canada can no longer afford to indulge in net-zero nonsense

Peter Tertzakian: Want to get pipelines built? Let Canadians own a piece of the action

Travis Toews: Canada needs a leader who takes economic growth seriously—and that requires being all in on energy investment